Do You Need Flood Insurance for a New Home in St. Johns County? The 2026 Nocatee, SilverLeaf & RiverTown Buyer's Guide

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 16, 2026

Key Takeaways

- A standard homeowners policy in Florida does not cover flood damage — not from a hurricane, not from a summer downpour, not ever. Flood is always a separate policy, and that is just as true for a brand-new home in Nocatee or SilverLeaf as it is for a 40-year-old house.

- If your new St. Johns County home sits in a Special Flood Hazard Area (flood zones labeled A, AE, or VE on the FEMA map) and you have a federally backed mortgage, flood insurance is federally required — your lender will not close without it.

- St. Johns County is a Community Rating System (CRS) Class 5 community, earning a 25% discount on National Flood Insurance Program (NFIP) premiums in the high-risk Special Flood Hazard Area and a 10% discount in the lower-risk X zones — applied automatically and printed on your policy.

- New construction is usually built at or above the Base Flood Elevation, which under FEMA's Risk Rating 2.0 pricing can mean a far lower flood premium than an older, lower home a few streets away. Your Elevation Certificate is the document that proves it.

- About 1 in 4 NFIP flood claims come from properties outside the high-risk zones. A Zone X home has no federal mandate, but "not required" is not "not at risk" — and a flood policy there is often only a few hundred dollars a year.

- If you hold a Citizens wind policy, a separate state rule is phasing in mandatory flood coverage for all policyholders by January 1, 2027 — another reason St. Johns buyers should price flood now, not later.

Buying a new home in St. Johns County — whether it's in Nocatee, SilverLeaf, RiverTown, or one of the dozens of newer communities filling in along County Road 210 — almost always raises the same question at the closing table: do I actually need flood insurance, and why is the lender asking for it? The short answer is that your homeowners policy will never pay for flood damage, so if your home is in a high-risk flood zone with a federally backed mortgage, flood coverage is required by law. Even when it is not required, St. Johns County's strong flood rating and the way new homes are elevated mean coverage is often far cheaper than buyers expect. Here is how it works for Northeast Florida's fastest-growing county in 2026. For a broader look at coverage across the area, see our Ponte Vedra and St. Johns County insurance page.

Why This Matters More in St. Johns County Than Almost Anywhere in Florida

St. Johns County is the fastest-growing county in Florida, with an estimated population of roughly 359,000 and an annual growth rate above 4% [1]. That growth is being built, quite literally, by a handful of enormous master-planned communities. In 2025, three St. Johns developments ranked among the top-selling communities in the entire country: SilverLeaf sold more than 1,000 homes, RiverTown sold roughly 500, and Nocatee — even as it nears build-out — sold more than 400 [2].

What that means in practice is that thousands of families a year are signing contracts on homes that did not exist 18 months ago, in neighborhoods carved out of former timberland and wetlands near the St. Johns River, Durbin Creek, and the Tolomato/Guana basin. Drainage, retention ponds, and fill dirt are engineered into these communities — but flood risk does not disappear because a subdivision is new. It gets redrawn. And the single most expensive mistake a new-construction buyer can make is assuming the shiny new house and the homeowners policy that comes with it have flood covered. They do not.

Your Homeowners Policy Does Not Cover Flood — Full Stop

This is the part that surprises people every hurricane season. A Florida homeowners (HO-3) policy covers wind, fire, and a long list of other perils, but rising water from outside the home is specifically excluded. Storm surge, a creek that overtops its banks, water that sheets across a saturated subdivision during an August thunderstorm — none of that is a homeowners claim. It is a flood claim, and you can only file it if you bought a separate flood policy.

Flood coverage comes from one of two places: the National Flood Insurance Program (NFIP), the federal program administered through FEMA, or a growing number of private flood carriers that now compete with — and frequently beat — the NFIP in Florida. Both pay for the same kind of loss; they simply price and underwrite it differently. That is exactly the kind of comparison an independent broker exists to run.

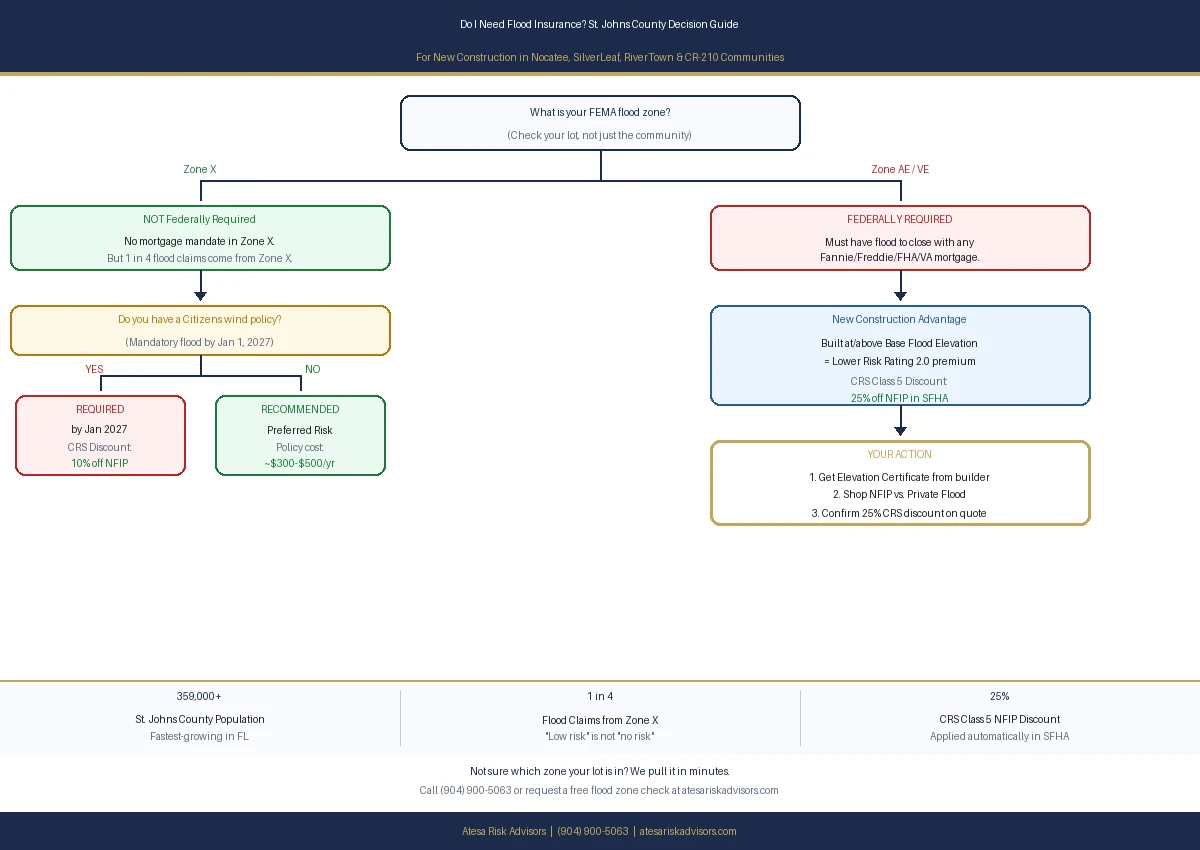

Is Flood Insurance Required on My New St. Johns County Home?

Whether coverage is required comes down to two things: your flood zone and your mortgage.

Flood zones are set by FEMA's Flood Insurance Rate Maps (FIRMs). The labels you will see on a St. Johns County property are:

- Zone X — the lower-risk area outside the Special Flood Hazard Area. Most of the higher, interior portions of communities like SilverLeaf and Nocatee fall here. No federal flood insurance requirement.

- Zones A and AE — the Special Flood Hazard Area (SFHA), the high-risk zones with a 1%-or-greater annual chance of flooding. AE zones carry a published Base Flood Elevation (BFE) on the map.

- Zone VE — high-risk coastal areas exposed to wave action. Rare for inland St. Johns construction but relevant near the Intracoastal and the beaches.

The mortgage rule: if your home is in an SFHA (A, AE, or VE) and you have a loan backed by Fannie Mae, Freddie Mac, the FHA, or the VA — which is nearly every conventional mortgage — federal law requires you to carry flood insurance for the life of the loan [3]. Your lender will require proof before closing and will escrow it if you do not provide your own. If you are in Zone X, there is no federal mandate, but the lender may still recommend coverage — and they are right to.

A note that catches buyers off guard: roughly 1 in 4 NFIP flood claims nationwide come from properties outside the high-risk zones [3]. "Zone X" means lower risk, not no risk. The good news is that a Zone X flood policy is one of the cheapest insurance products you will ever buy — frequently a few hundred dollars a year.

The St. Johns County Discount Most Buyers Never Hear About

Here is a genuine local advantage. St. Johns County participates in FEMA's Community Rating System (CRS) — a voluntary program that rewards communities for going beyond the minimum floodplain-management standards. The county has earned a Class 5 rating, one of the better ratings in Florida [4].

That rating translates directly into money off your premium:

- 25% discount on NFIP flood policies for properties inside the Special Flood Hazard Area (effective for policies in the SFHA on or after October 1, 2020).

- 10% discount on standard-rated NFIP policies in the X zones.

The discount is applied automatically and shows up right on your NFIP policy declarations page [4]. You do not apply for it — but you should confirm it is there, because a misclassified property occasionally misses it. This is one of the first things we check when we review a St. Johns County flood quote.

Why New Construction Is Often Cheaper to Insure — and the One Document That Proves It

Under FEMA's Risk Rating 2.0 pricing methodology, the biggest single factor in a flood premium is how high the lowest floor of your home sits relative to the expected flood level. New homes in St. Johns County are built to current floodplain code — which, in an SFHA, means the lowest floor must be at or above the Base Flood Elevation, often with additional "freeboard" on top.

A home built two or three feet above the BFE is statistically much less likely to take on water than an older home built at grade in the 1980s — and Risk Rating 2.0 prices it accordingly. The document that captures all of this is the Elevation Certificate, a FEMA form completed by a licensed surveyor that records your lowest floor elevation, the BFE, and the building's flood characteristics.

For new construction in an AE or VE zone, your builder or a surveyor should provide an Elevation Certificate at or shortly after completion [5]. Hold onto it. While Risk Rating 2.0 no longer strictly requires one for every NFIP quote, a favorable Elevation Certificate can be the difference between a guess and a precisely rated — usually lower — premium, and private flood carriers frequently ask for it. If your builder has not handed you one, ask.

I've stood on the builder's side of the table, and I've watched two nearly identical St. Johns County homes a few streets apart pay very different flood premiums — the only difference being that one owner had the Elevation Certificate in hand and the other didn't. On new construction, that one piece of paper is worth real money. Get it before you close.

— Ricardo Alonso, Founder, Atesa Risk Advisors

The Citizens Wedge: A Separate Flood Mandate Arriving January 1, 2027

If your wind or homeowners coverage is through Citizens Property Insurance — common for newer coastal-adjacent homes that private carriers are cautious about — there is a second flood rule in play. State law is phasing in a requirement that Citizens policyholders carry flood insurance regardless of their flood zone, with the final group of policyholders required to comply by January 1, 2027 [6]. Higher-value homes are already subject to it.

For a St. Johns County buyer, that means even a Zone X home insured through Citizens may soon need flood coverage to keep its wind policy in force. Pricing flood now — while you can shop it calmly rather than scrambling against a deadline — is simply smart sequencing. We cover the full Citizens timeline in a dedicated guide linked below.

How to Buy Smart: A Quick Checklist for St. Johns County Buyers

- Find your zone before you waive contingencies. The county's Floodplain Management office issues FIRM determination letters, and your broker can pull the zone in minutes.

- Get the Elevation Certificate from your builder if you are in an AE or VE zone — it is leverage on price.

- Confirm the CRS discount is showing on any NFIP quote — 25% in the SFHA, 10% in X zones.

- Shop NFIP against private flood. In St. Johns County's newer, well-elevated homes, private carriers are often competitive or cheaper.

- Do not skip Zone X coverage just because it is optional. A Zone X flood policy is cheap insurance against the 1-in-4 claim that comes from "low-risk" ground.

Frequently Asked Questions

Do I need flood insurance for a new home in Nocatee or SilverLeaf?

It depends on your specific lot's flood zone. Much of the higher interior ground in these communities is mapped Zone X, where flood insurance is not federally required. But lots nearer ponds, creeks, and preserves can fall into AE zones, where a federally backed mortgage makes coverage mandatory. Always confirm the zone for your exact address rather than assuming the whole community is the same.

How much does flood insurance cost in St. Johns County?

It varies widely by zone and elevation. The NFIP prices each property individually under Risk Rating 2.0: a Zone X policy can run a few hundred dollars a year, while an SFHA home pays more based on its specific risk profile. St. Johns County's CRS Class 5 status knocks 10–25% off NFIP premiums, and a well-elevated new home with a good Elevation Certificate typically prices toward the lower end. The only way to know your number is to run the actual address.

What is an Elevation Certificate and do I need one?

It is a FEMA form, completed by a licensed surveyor, that documents how high your home's lowest floor sits relative to the Base Flood Elevation. For new construction in an AE or VE zone, your builder or surveyor should provide one. It can lower your premium under Risk Rating 2.0 and is frequently requested by private flood carriers, so it is worth obtaining and keeping.

I'm in Zone X — should I really bother?

Yes, in most cases. Roughly a quarter of all NFIP flood claims come from outside the high-risk zones, and Zone X coverage is inexpensive. For a few hundred dollars a year, a flood policy protects you from the storm that does not read the flood map.

Should I use NFIP or private flood insurance in St. Johns County?

Both cover the same kind of loss, but they price and underwrite it differently. NFIP is federally backed, widely available, and the source of the county's automatic CRS discount. Private flood carriers have expanded aggressively across Florida and often beat the NFIP on price for newer, well-elevated St. Johns County homes — sometimes with higher limits and faster issuance. Because new construction here typically sits at or above Base Flood Elevation, it is exactly the profile private carriers compete hardest for, so it is worth quoting both before you commit.

Does the Citizens 2027 flood mandate apply to a new St. Johns County home?

If your wind or homeowners coverage is through Citizens Property Insurance, yes. A state rule is phasing in mandatory flood insurance for all Citizens policyholders regardless of flood zone, with the final group required to comply by January 1, 2027. That means even a Zone X home insured through Citizens may need a flood policy to keep its wind coverage in force — so pricing flood now, while you can shop it calmly, beats scrambling against the deadline.

How Atesa Risk Advisors Can Help

At Atesa Risk Advisors, we shop both the NFIP and the private flood market for St. Johns County buyers, and we start by pulling your exact lot's flood zone — not the community's general designation — so you know whether coverage is required before you waive a contingency. We confirm the county's CRS Class 5 discount is applied to your quote, review your builder's Elevation Certificate for rating leverage, and line flood up alongside your homeowners and wind coverage so nothing slips through the cracks at the closing table.

As an independent, RamseyTrusted brokerage, we work for you rather than a single carrier — which matters most on new construction, where the right elevation documentation and the right market can mean hundreds of dollars a year in difference on a policy you will hold for as long as you own the home.

Closing on a new home in Nocatee, SilverLeaf, RiverTown, or anywhere in St. Johns County? Get your free flood-zone check and quote at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] World Population Review — St. Johns County, Florida Population 2026

[3] FEMA / FloodSmart — Flood Insurance Requirements and Risk Outside High-Risk Zones

[4] St. Johns County — Floodplain Facts (Community Rating System Class 5 discount)

[5] FEMA — National Flood Insurance Program Elevation Certificate and Instructions

[6] News4Jax — Flood insurance will be mandatory for most Citizens policyholders by 2027

Related Reading

- The Citizens Flood Deadline: What Northeast Florida Coastal Homeowners Must Do Before January 1, 2027

- Clay County's New FEMA Flood Maps Take Effect Spring 2027 — What Orange Park, Fleming Island, and Middleburg Homeowners Must Do Now

- How Much Does Flood Insurance Cost in Florida? (2026 Guide)

- How Much Is Homeowners Insurance in Florida? The Surprising 2026 Reality

- What Is an Independent Insurance Agent? Why It Matters for Your Wallet

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a Master of Liberal Arts in Finance from Harvard University and a background in construction, he helps homeowners and new-construction buyers across St. Johns County and Northeast Florida navigate flood zones, elevation, and coastal property risk.