Clay County's New FEMA Flood Maps Take Effect Spring 2027 — What Orange Park, Fleming Island, and Middleburg Homeowners Must Do Now

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 26, 2026

Key Takeaways

- FEMA is replacing Clay County's 2014 Flood Insurance Rate Maps with updated maps effective spring 2027 — homeowners have roughly 10 months to act [1][2].

- Properties near the St. Johns River, Doctors Lake, Black Creek, and Doctors Inlet face the highest likelihood of flood zone reclassification [1].

- If your home moves INTO Zone AE and you carry a federally-backed mortgage, federal law requires your lender to mandate flood insurance — typically within 45 days of the effective date [3].

- Purchasing NFIP coverage before the maps go effective can lock in lower grandfathered rates — but Risk Rating 2.0 has narrowed that benefit for many properties [4].

- The NFIP's 30-day waiting period means you cannot wait until the last minute. Private flood policies can sometimes bind in 10–15 days, but that is not a strategy to rely on [4].

- An independent broker shops the federal NFIP and private flood carriers simultaneously to find the most cost-effective option for your new designation.

FEMA's new Clay County flood maps take effect spring 2027, replacing maps last revised around 2014 — and a meaningful share of Orange Park, Fleming Island, Middleburg, and Green Cove Springs homes will move into a high-risk flood zone for the first time. Homeowners in those communities have roughly ten months to verify their proposed designation, lock in NFIP coverage before the 30-day waiting period becomes a deadline-killer, and compare private flood insurance that often costs 20–40% less than equivalent NFIP coverage.

FEMA is updating Clay County's Flood Insurance Rate Maps — the official government documents that define which homes sit in high-risk flood zones and which don't. The new maps use more precise LiDAR (laser-survey) elevation data and updated hydraulic modeling of the county's waterways. The anticipated effective date is spring 2027.

What's Actually Changing on These Maps

Flood Insurance Rate Maps — FIRMs in FEMA's shorthand — divide every community into flood zones based on the statistical likelihood of flooding in any given year. The key dividing line is the Special Flood Hazard Area (SFHA), which includes Zone AE (the most common high-risk designation), Zone A, and AE Floodway. A property inside the SFHA has at least a 1% annual chance of flooding — what the industry calls the "100-year flood" threshold. Cross that line and mandatory purchase requirements attach to federally-backed mortgages; stay outside it and they do not.

Clay County's current maps are roughly a decade old. In the time since, significant development has reshaped drainage patterns — particularly around the Fleming Island and Oakleaf Plantation corridors — and FEMA's modeling technology has advanced considerably. Newer LiDAR data captures ground elevation far more precisely than older photogrammetric methods. The result: some properties that appeared safely above the flood line may now sit inside it, and some that were technically in the flood zone may no longer be.

FEMA released preliminary maps in mid-2025 and held a public open house on September 12, 2025, where residents could review proposed changes alongside FEMA and Clay County Planning and Zoning staff [2]. A 90-day appeal and comment period followed, during which property owners could submit scientific or technical data — such as an elevation certificate from a licensed surveyor — to challenge an incorrect designation. That window has now closed. The maps are being finalized, with a spring 2027 effective date.

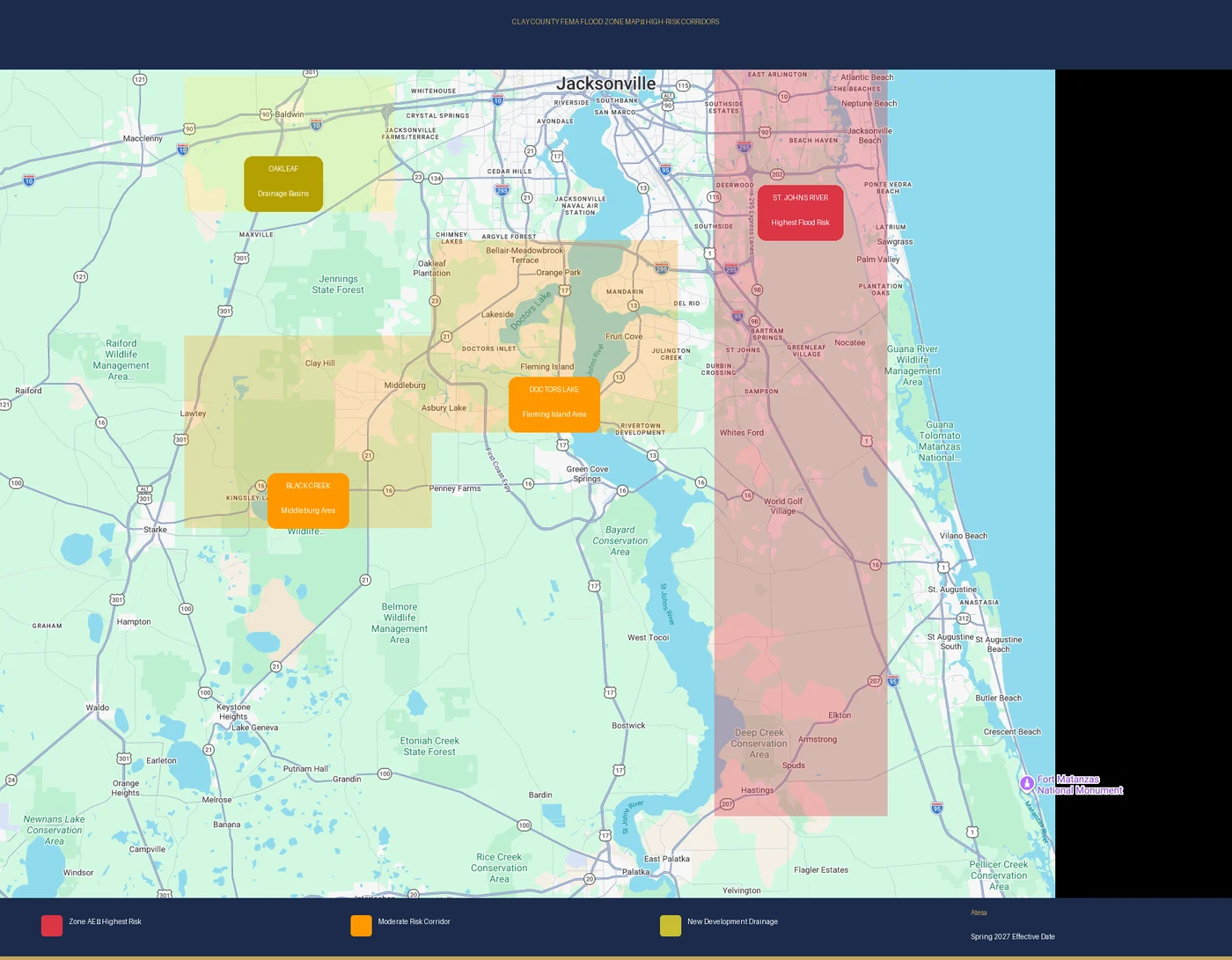

Which Clay County Communities Face the Most Reclassification Risk

FEMA does not publish a street-by-street list of which addresses are changing. You must check your individual property. That said, Clay County's geography points to several high-exposure corridors:

- St. Johns River shoreline (Orange Park, Green Cove Springs): Low-lying properties within a half mile of the river's edge, where backwater flooding during major storms can extend well inland.

- Doctors Lake and Doctors Inlet (Fleming Island area): This tidal inlet connects Doctors Lake to the St. Johns River. Storm surge pushing up the St. Johns from the Atlantic can propagate into Doctors Lake, raising flood elevations beyond what freshwater-only modeling predicted.

- North and South Forks of Black Creek (Middleburg, southeastern Clay County): Black Creek is Clay County's second major drainage system, prone to extended inland flooding after sustained rainfall events and historically underestimated in older flood models.

- Newer development drainage basins (Oakleaf Plantation, southwest Clay County): Engineered stormwater systems in these subdivisions affect flood boundaries in ways not fully reflected in the 2014 maps.

To check your specific address: visit Clay County's interactive flood map at claycountygov.com/community/flood-zone-changes, or use the FEMA Flood Map Service Center and search by address. Both tools display your proposed new designation from the preliminary maps.

What Happens If Your Home Moves INTO a High-Risk Zone

Being reclassified from a low-risk zone (typically Zone X) into Zone AE triggers real legal and financial consequences:

- Mandatory purchase requirement. If you carry a federally-backed mortgage — FHA, VA, or any conventional loan sold to Fannie Mae or Freddie Mac — federal law requires your lender to notify you of the reclassification. If you do not act, your lender will force-place a flood policy on your behalf. Force-placed policies routinely cost two to four times what you would pay shopping the open market, and they typically provide only structural coverage with no contents protection [3].

- Your homeowners policy still does not cover flooding. Water that enters your home because a river overflows, storm surge pushes inland, or heavy rain overwhelms a storm drain is a flood event — and your standard HO-3 homeowners policy excludes it entirely. Only a standalone flood policy — NFIP or private — covers this peril.

- Higher premium — unless you act strategically. Zone AE flood insurance is priced under FEMA's Risk Rating 2.0 methodology, which accounts for your home's elevation above the Base Flood Elevation (BFE). Without an elevation certificate documenting that your finished floor sits significantly above the BFE, FEMA's algorithm defaults to assumptions that often overstate your risk and inflate your premium [4].

What If Your Home Is Moving OUT of the Flood Zone?

Reclassification from Zone AE to Zone X is the good-news scenario: the mandatory purchase requirement disappears after the maps go effective, and your NFIP premium — if you keep coverage — often changes little, because the NFIP now prices each property individually under Risk Rating 2.0 rather than by zone. However, flood experts consistently recommend maintaining some flood coverage even in Zone X. More than 20% of NFIP claims nationwide come from properties outside the high-risk SFHA. Clay County's low-lying geography along a tidal river system means flooding can occur in any zone.

If you are moving out of the SFHA, the smart move is not to cancel coverage — it is to ask your broker to requote you at the lower-risk premium you now qualify for. The savings can be substantial, and you retain protection against the flood events that maps cannot perfectly predict.

The Grandfathering Window — Why Timing Matters

The NFIP's grandfathering rule allows homeowners who purchase a flood policy and maintain continuous, uninterrupted coverage before the new maps become effective to be rated based on their prior, more favorable flood zone designation rather than the new one. For a home moving from Zone X into Zone AE, this can translate into meaningful annual premium savings.

A critical caveat: FEMA's Risk Rating 2.0, implemented in October 2021, fundamentally changed how NFIP premiums are calculated. Rather than relying primarily on flood zone designation, the methodology now uses property-specific variables: distance to water, first-floor height, and replacement cost value. For many properties under Risk Rating 2.0, the zone-based grandfathering benefit has narrowed or disappeared entirely [4]. The only way to know whether grandfathering saves you money is to have a licensed agent model your property under both scenarios before the maps go effective.

One thing is certain: the NFIP's 30-day waiting period is not flexible. If the maps go effective April 1, 2027, you need an NFIP policy bound by March 2 to ensure coverage is active on day one. Private flood insurance often carries a 10–15 day waiting period, but that is not a plan. The time to evaluate your options is now, not next winter.

NFIP vs. Private Flood Insurance in Clay County

Florida homeowners have two primary routes to flood coverage:

NFIP (National Flood Insurance Program): Federally backed and available to virtually every homeowner regardless of risk level. Coverage caps at $250,000 for the structure and $100,000 for personal property. Premiums are set by FEMA's Risk Rating 2.0 algorithm — no agent can negotiate a better rate within the NFIP. Contents claims settle on an actual cash value basis, meaning depreciation reduces your payout.

Private Flood Insurance: Written by private carriers and frequently available at premiums 20–40% below the NFIP equivalent. Private policies often offer higher structure limits (critical for homes valued above the $250,000 NFIP cap), replacement-cost value on contents, and additional living expense coverage if your home is uninhabitable after a flood [6]. The tradeoff: private carriers can non-renew in high-risk zones after a bad storm season, and some mortgage servicers require documentation confirming that a private policy meets NFIP "substantial equivalency" standards.

As an independent broker shopping 40+ A-rated carriers, Atesa quotes both NFIP through write-your-own partners and private flood markets simultaneously, delivering a side-by-side comparison so you choose based on coverage, cost, and carrier stability — not whichever option the first call center happened to pitch.

Your 5-Step Action Plan Before Spring 2027

| Step | Action | Why it matters |

|---|---|---|

| 1 | Check your proposed flood zone today. Use Clay County's interactive map or FEMA's MSC. Document your current and proposed designations. | Determines whether you need to act before the effective date. |

| 2 | Order an elevation certificate if you are near a zone boundary. A licensed land surveyor measures your home's finished floor elevation against the Base Flood Elevation. | If your floor sits well above the BFE, the EC can dramatically reduce your premium — often paying for itself ($500–$900) in the first year. |

| 3 | Get a flood insurance quote — both NFIP and private — now. | Knowing your rate before the effective date lets you budget and compare without deadline pressure. |

| 4 | If you rent in Clay County, get contents-only flood coverage. Your landlord's policy protects the structure; your belongings are your responsibility. | Renter flood policies typically start around $100–$200 per year. |

| 5 | Do not let your mortgage servicer force-place coverage. | Force-placed flood insurance is the most expensive and least protective option — two to four times the open-market price with no contents coverage. |

Florida-Specific Considerations

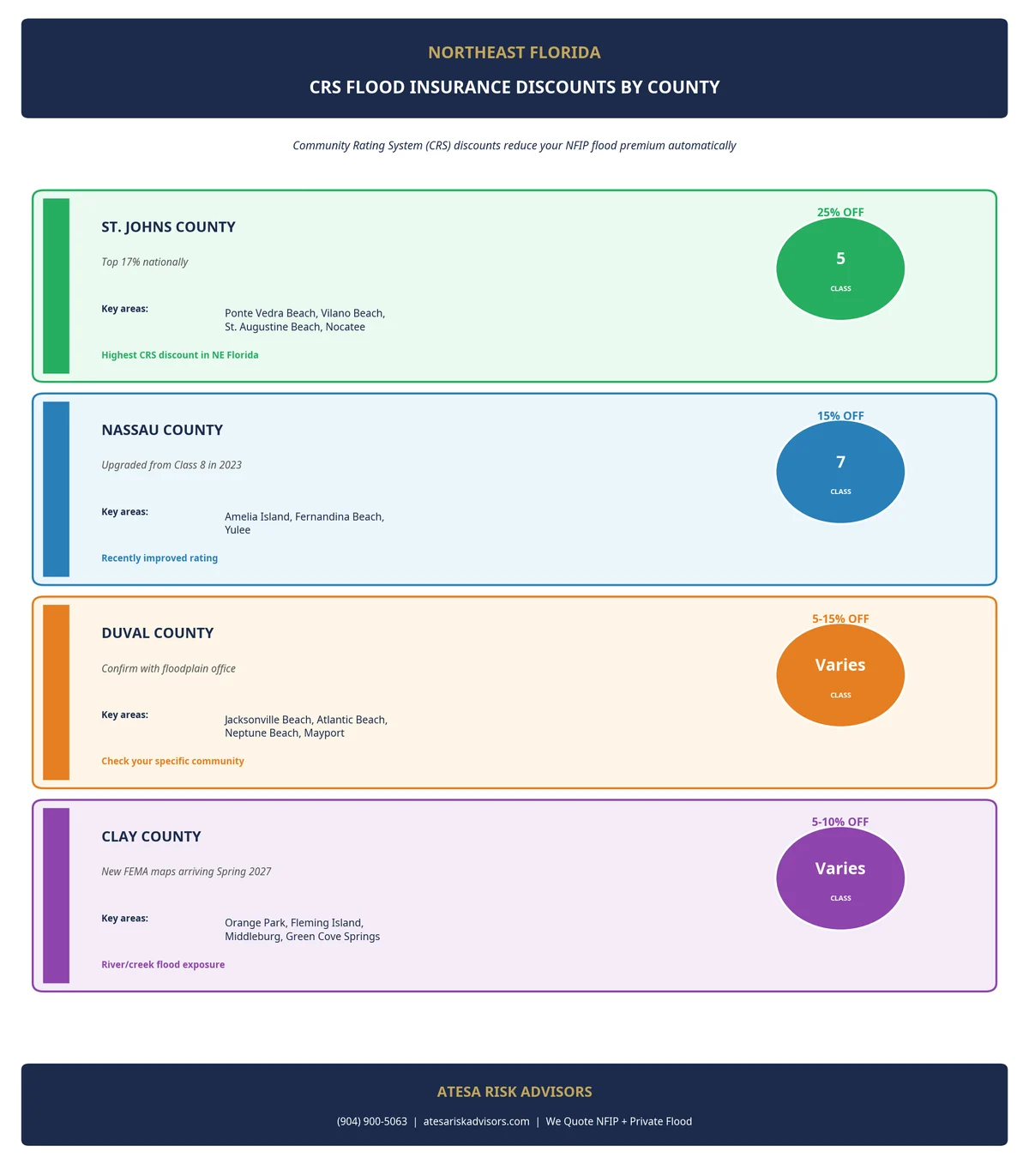

Florida Statute § 627.715 lays out the requirements for private flood insurance policies that mortgage lenders must accept in place of NFIP. Coverage must meet "substantial equivalency" standards — providing at least the same protection as NFIP at the same coverage limit. Many private flood carriers in Florida (Neptune, Wright, TypTap, Lloyd's syndicates) now offer policies that exceed NFIP terms while costing 20–40% less [6].

After Hurricane Idalia (2023) and the 2024 storm season, Florida's private flood market tightened. Several carriers added moratoria on new policies in coastal ZIP codes during active hurricane forecasts. The window between flood map updates and storm season is the right time to bind — outside hurricane warnings and before the new maps trigger a wave of demand.

FAQ for Clay County Homeowners

Q: Do I have to buy flood insurance if my Clay County home is reclassified to Zone AE?

A: If you carry a federally-backed mortgage (FHA, VA, or conventional loans sold to Fannie Mae or Freddie Mac), yes. Federal law requires your lender to mandate flood insurance once your property is designated Zone AE. If you own your home free and clear, no law requires flood insurance — but your structure and contents have zero flood protection under a standard homeowners policy.

Q: How do I find out if my specific property is affected by the FEMA map update?

A: Visit Clay County's interactive flood map at claycountygov.com/community/flood-zone-changes or the FEMA Flood Map Service Center at msc.fema.gov. Enter your street address to see both your current and proposed new flood zone designations. For questions, contact Clay County Planning and Zoning at (904) 278-4705.

Q: What is an elevation certificate, and do I need one?

A: An elevation certificate is a document from a licensed land surveyor measuring your home's lowest finished floor elevation relative to the Base Flood Elevation on FEMA's maps. If your floor is above the BFE, the EC typically reduces your NFIP premium significantly. A new survey costs $500–$900 but premium savings often exceed that in the first year. Homes built after 1975 in a flood zone may already have an EC on file with Clay County — worth confirming before ordering a new one.

Q: Can I get private flood insurance instead of the NFIP in Clay County?

A: Yes. Florida law (FS 627.715) permits mortgage lenders to accept private flood insurance meeting "substantial equivalency" standards in place of NFIP. Private policies often carry lower premiums, higher coverage limits, replacement-cost contents coverage, and shorter waiting periods. Confirm with your mortgage servicer before binding, as lenders vary in how they handle private flood documentation.

Q: What exactly is the NFIP 30-day waiting period?

A: NFIP flood policies have a mandatory 30-day waiting period from the date of application before coverage activates. You cannot purchase a policy days before a map effective date and expect coverage on day one. There are narrow exceptions for loan closings. Plan to bind well in advance of storm seasons and map effective dates.

Q: If I do not have a mortgage, do I still need flood insurance?

A: No law requires it for mortgage-free homeowners, but the financial risk is entirely yours. A single flood event can cause $50,000 to $200,000 or more in structural damage that no homeowners policy will pay for. In Clay County — with its St. Johns River shoreline, tidal inlets, and inland creek systems — uninsured flood exposure is a significant financial risk.

Q: Will my homeowners insurance cover water damage from heavy rain or storm surge?

A: No. Standard homeowners insurance (HO-3) explicitly excludes all flood-related water damage regardless of source — overflowing rivers, storm surge, surface water from heavy rain, or overflow from any body of water. Only a standalone flood policy — NFIP or private — covers this peril. This exclusion applies to every homeowners carrier writing in Florida.

Q: How long before the map effective date should I bind a policy?

A: For NFIP, bind at least 30 days before the effective date so coverage is in force on day one — and ideally 60+ days to allow time for an elevation certificate if needed. For private flood, 15–30 days before is typically safe, but private carriers can impose binding restrictions during active hurricane forecasts.

Related Reading

- Clay County Homeowners Insurance in 2026: The Inland Advantage, New-Construction Credits, and How to Shop It — Why inland Clay homes are priced differently, how wind-mitigation credits stack on new builds, and how the 2027 flood-map update fits your coverage.

- How Much Does Flood Insurance Cost in Florida? (2026 Guide) — NFIP vs. private flood pricing, sample quotes by county, and how Risk Rating 2.0 changes the math.

- What Your Florida Homeowners Policy Actually Covers — and What It Doesn't — Why the flood exclusion exists in every HO-3 policy and what gaps to fill.

- Hurricane Season 2026: What Every Florida Homeowner Needs to Know — Prep checklist, coverage review timing, and Florida-specific carrier behavior in the lead-up to June 1.

How Atesa Risk Advisors Can Help

Atesa Risk Advisors is a Jacksonville-based, Florida-licensed (2-20 General Lines) independent brokerage serving homeowners across Duval, Clay, St. Johns, and Nassau Counties. We are a RamseyTrusted provider and shop 40+ A-rated carriers — including both NFIP write-your-own partners and private flood markets — to find coverage that reflects your property's actual risk profile, not a worst-case map assumption.

Flood insurance is among the most misunderstood products in the Florida market. The difference between buying blind and working with a broker who models your elevation, compares NFIP versus private, and explains the grandfathering implications can easily be $300–$600 per year. For Clay County homeowners facing the spring 2027 zone change, that difference is real money on the table right now. You can also learn how we serve the area on our Orange Park insurance page.

Want a free Clay County flood insurance review before the maps go effective? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Clay County, FL — Flood Zone Changes: What Homeowners and Businesses Need to Know

[2] Clay County, FL — Flood/FEMA Information, Planning and Zoning Division

[3] FEMA — National Flood Insurance Program Overview

[4] FEMA Flood Map Service Center

[5] FEMA — Letters of Final Determination 2026

[6] Federal Register — NFIP Assistance to Private Sector Insurers, FY 2027 Arrangement (May 19, 2026)

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. He serves homeowners across Northeast Florida with a focus on flood, wind, and high-value coastal property risk.