The Citizens Flood Deadline: What Northeast Florida Coastal Homeowners Must Do Before January 1, 2027

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 2, 2026

Key Takeaways

- Florida law requires nearly every Citizens Property Insurance personal-residential policy that includes windstorm coverage to also carry a separate flood policy — and the final deadline for everyone is January 1, 2027 [1][2].

- The mandate is phasing in by home value: dwellings valued at $400,000 or more have been required to carry flood since January 1, 2026; all remaining policies — regardless of value — must comply by January 1, 2027 [1][3].

- It applies even if your home is not in a FEMA high-risk flood zone. Coastal Citizens policyholders in Jacksonville Beach, Ponte Vedra, St. Augustine Beach, and Amelia Island are squarely in scope [2][3].

- Your flood limit must at least equal your Citizens dwelling (Coverage A) limit or the $250,000 NFIP maximum for a home, whichever is lower [1].

- Miss the requirement at renewal and Citizens will non-renew your entire policy — stripping your wind coverage in the middle of hurricane season [1][2].

- St. Johns County's CRS Class 5 rating earns a 25% NFIP discount and Nassau County's Class 7 earns 15% — and private flood policies often beat NFIP pricing by 10–30% for newer, well-elevated homes [4][5][6].

If you insure your home through Citizens Property Insurance and your policy includes windstorm coverage, Florida law now requires you to also carry a separate flood insurance policy — and for the many Northeast Florida coastal homeowners with dwellings valued under $400,000, that requirement lands at your first renewal on or after January 1, 2027. The rule applies whether or not your home sits in a FEMA-designated flood zone, and failing to show proof of a qualifying flood policy is grounds for Citizens to non-renew your home insurance entirely — which means losing your hurricane wind coverage at the worst possible time.

This is one of the most misunderstood changes in the Florida market right now, and it hits the First Coast harder than almost anywhere else. Citizens — the state-created "insurer of last resort" — is heavily concentrated in coastal ZIP codes precisely because private carriers have retreated from the beaches. So as the 2026 hurricane season opens, a large share of homeowners in Duval, St. Johns, and Nassau counties are about to discover a flood-insurance bill they never planned for. Here is exactly what the rule says, who it affects, and how to satisfy it without overpaying.

What the Citizens Flood Requirement Actually Says

Citizens Property Insurance Corporation is the not-for-profit, state-backed insurer the Florida Legislature created for homeowners who can't find coverage in the private market. As part of the 2022 reforms (passed in a December 2022 special session and codified under section 627.351(6), Florida Statutes), the Legislature attached a condition to Citizens eligibility: if your policy includes windstorm coverage, you must also obtain and maintain flood insurance [1][2].

"Maintain" is the operative word — this isn't a one-time box to check at purchase. Flood coverage becomes a permanent condition of eligibility, and if it lapses, Citizens can non-renew your property policy [1].

The required limit is specific. Your flood dwelling coverage must at least equal the Coverage A limit on your Citizens policy — Coverage A is the part that insures the physical structure of your home — or the maximum building coverage available through the National Flood Insurance Program (NFIP), which is $250,000 for a home, whichever is lower [1]. So a $320,000 dwelling limit requires at least $250,000 in flood coverage; a $210,000 dwelling limit requires at least $210,000.

A few policy types are exempt: condominium unit-owner (HO-6) policies, tenant (renter) contents policies, and any policy that excludes windstorm or hail coverage [3]. For most single-family homeowners on the coast, though, the exemptions won't apply.

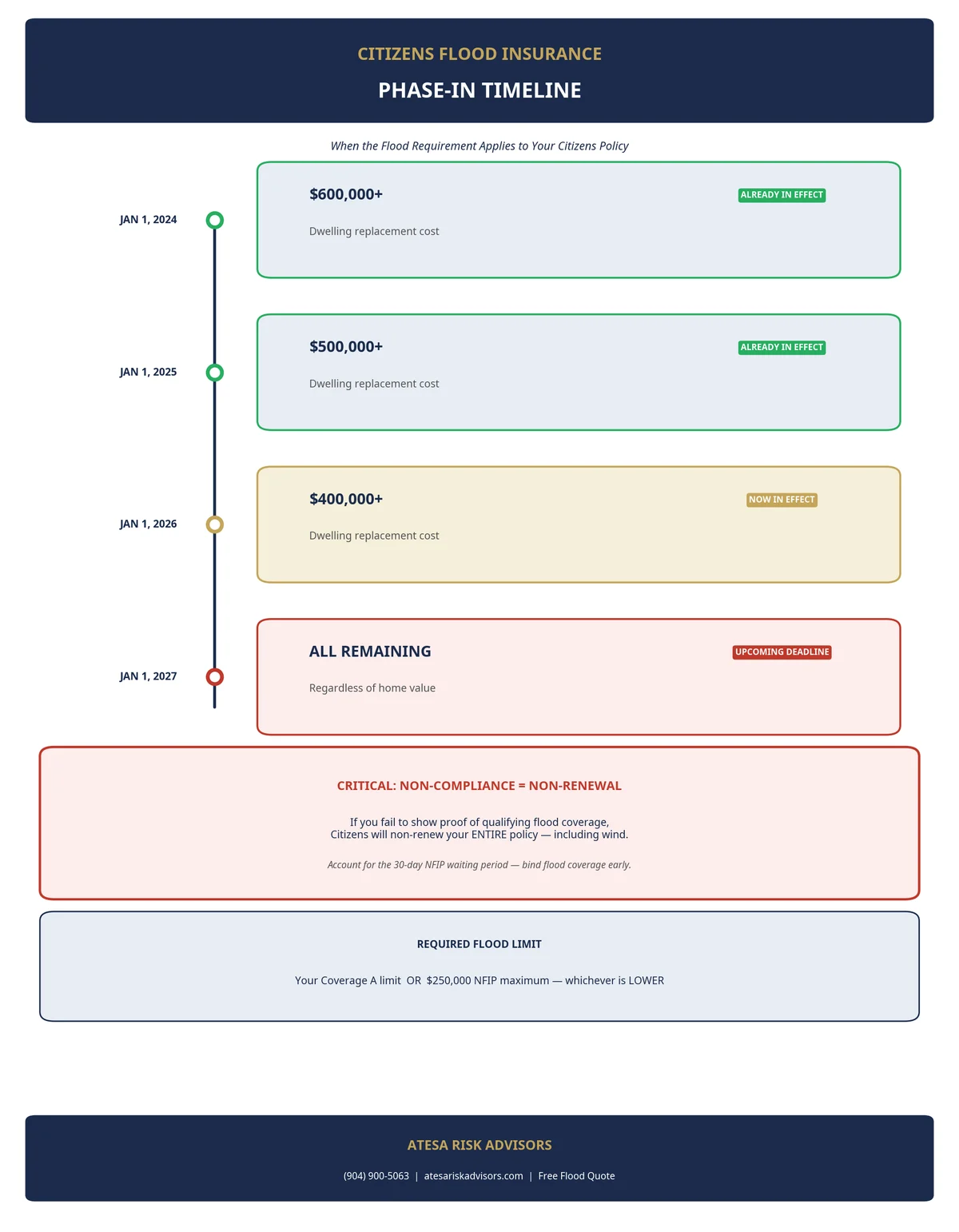

The Phase-In Schedule: Where 2026 and 2027 Fit

The Legislature didn't drop this on everyone at once. It phases in by the dwelling replacement cost — the estimated cost to rebuild your home — starting with the most expensive properties [1][3]:

- January 1, 2024 — homes with a dwelling replacement cost of $600,000 or more

- January 1, 2025 — homes valued at $500,000 or more

- January 1, 2026 — homes valued at $400,000 or more

- January 1, 2027 — all remaining Citizens personal-residential policies with wind coverage, regardless of value

That last line is why this is suddenly urgent for ordinary First Coast homeowners. As of January 1, 2026, the $400,000 tier swept in a large block of Ponte Vedra, Nocatee, and beaches-area homes — and the January 1, 2027 deadline captures everyone else, from the $250,000 inland home in Orange Park to the modest beach cottage in Atlantic Beach [1][3].

Because Citizens enforces the requirement at renewal, you don't have until New Year's Day 2027 to act. If your policy renews in February 2027, you'll need proof of flood coverage before that renewal processes — and given the NFIP's waiting period (below), the practical deadline is weeks earlier than the calendar date.

"But I'm Not in a Flood Zone" — Why That Doesn't Matter Here

This is the single biggest point of confusion, so it's worth stating plainly: the Citizens flood requirement applies even to homes outside the Special Flood Hazard Area (SFHA) [3].

The SFHA is FEMA's term for a high-risk flood zone (Zone AE, Zone A, and similar) where a federally backed mortgage lender must require flood insurance. Many Northeast Florida homeowners assume that because they're in a low-to-moderate-risk "Zone X" and their lender never required flood, they don't need it. Under the old rules, that was their choice. Under the Citizens rule, it's no longer optional.

That matters here because a meaningful share of Florida flood claims come from properties outside the mapped high-risk zones — flash flooding, storm surge that overtops the maps, and drainage backups don't respect FEMA's lines. The state's logic: if it's going to backstop your wind risk through Citizens, it doesn't want to be left holding an uninsured flood loss on the same home.

What This Means County by County

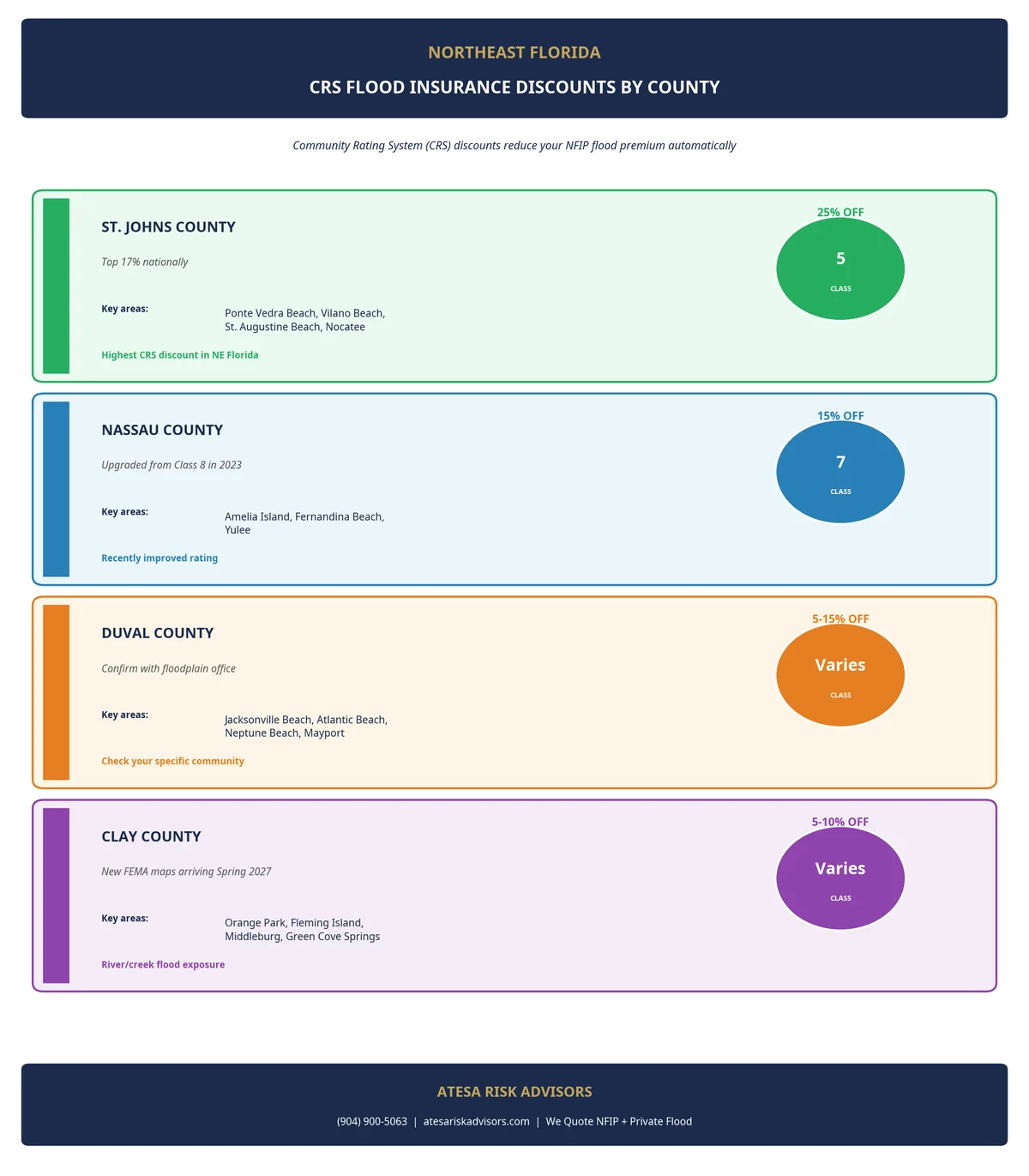

Northeast Florida's exposure to this rule is uneven, and your CRS discount softens the blow differently depending on where you live. The Community Rating System (CRS) is a FEMA program that rewards communities for floodplain management with NFIP premium discounts for every policyholder in that community:

- St. Johns County — CRS Class 5, which earns a 25% discount on NFIP flood premiums, placing the county in the top 17% of CRS communities nationally [4]. With heavy Citizens concentration in Ponte Vedra Beach, Vilano Beach, and St. Augustine Beach, St. Johns has both the most affected homeowners and the strongest discount cushion.

- Nassau County — CRS Class 7, a 15% discount, upgraded from Class 8 in 2023 [5]. Amelia Island and Fernandina Beach Citizens policyholders benefit here.

- Duval County — Jacksonville and the beaches (Atlantic Beach, Neptune Beach, Jacksonville Beach, Mayport) participate in CRS as well; confirm your community's current class and discount with the city/county floodplain office before you quote.

- Clay County — Largely inland (Orange Park, Fleming Island, Middleburg), but with significant exposure along the St. Johns River, Doctors Lake, and Black Creek — and with new FEMA flood maps arriving in spring 2027 that may reclassify properties just as the Citizens deadline hits.

NFIP vs. Private Flood: How to Comply Without Overpaying

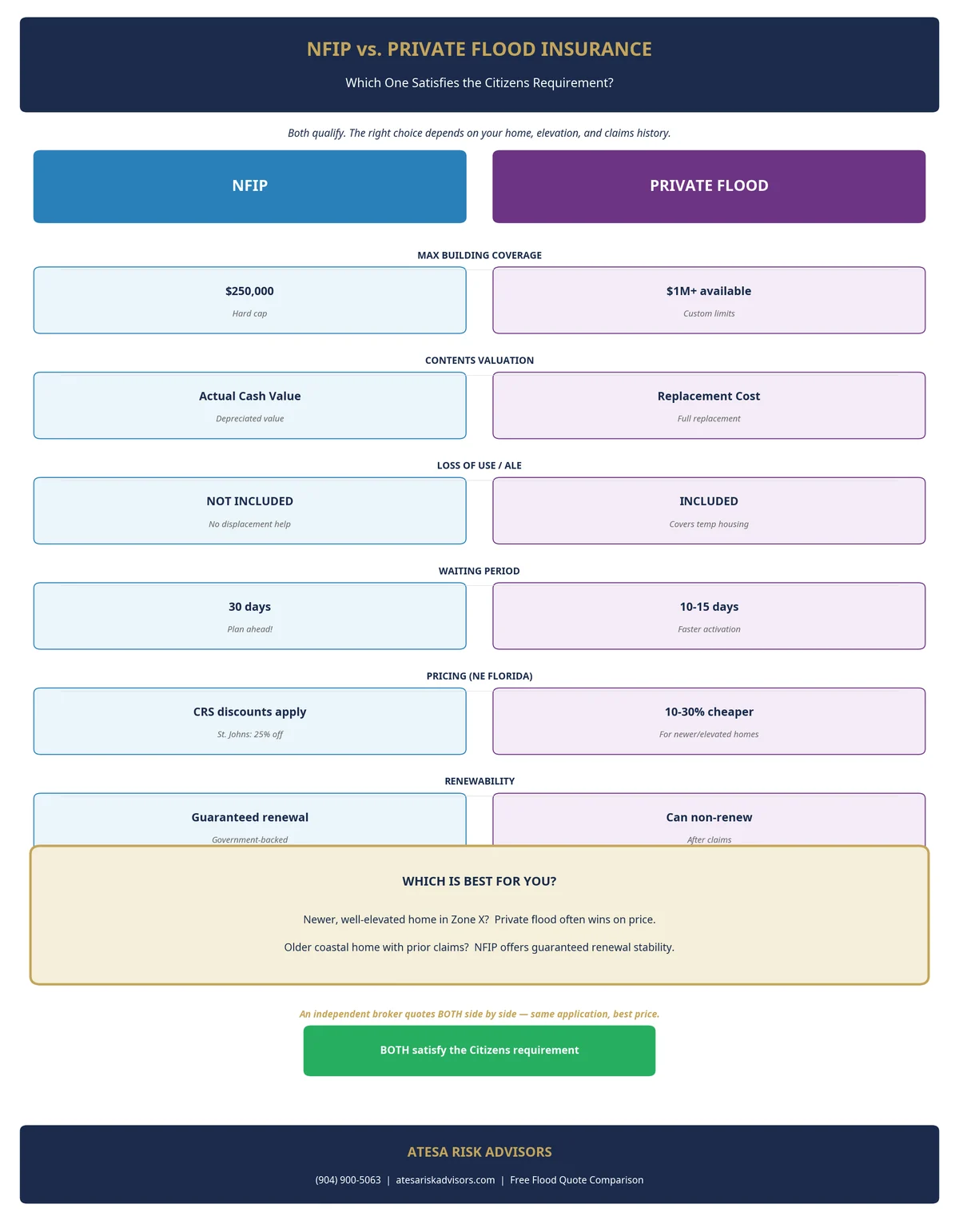

You can satisfy the Citizens requirement with either an NFIP policy or a qualifying private flood policy. They are not the same product, and the cheaper option depends entirely on your home:

- NFIP is the federal program. Building coverage caps at $250,000 for a home, contents are paid on an actual cash value (ACV) basis (depreciated value, not replacement cost), and there's no coverage for additional living expenses if you're displaced. NFIP's standard 30-day waiting period is the big scheduling trap — buy too late and the policy won't be in force in time for your renewal [6][7].

- Private flood carriers can offer much higher limits (well into the millions), replacement-cost contents, and loss-of-use coverage NFIP doesn't provide. For newer, well-elevated homes in moderate-risk zones, private flood frequently runs 10–30% cheaper than NFIP, and waiting periods are often shorter (around 10–15 days) [6].

For high-risk, repeatedly flooded, or older coastal homes, NFIP is sometimes the safer long-term bet, since private carriers can non-renew after a claim. For the typical sub-$400,000 First Coast home now swept into the 2027 deadline, private flood is very often the lower-cost path to compliance — but the only way to know is to quote both side by side, which is exactly what an independent broker does.

Your Action Plan Before Renewal

- Find your renewal date and your Coverage A limit. They're on the declarations ("dec") page of your Citizens policy. Your required flood limit is the lower of your Coverage A or $250,000.

- Check whether you've already been notified. If your dwelling is valued at $400,000+, you were required to comply as of your first 2026 renewal — confirm your flood policy is active and not just "pending."

- Don't wait for the deadline. Back the NFIP 30-day waiting period out from your renewal date. If you renew in January 2027, you realistically need to bind flood coverage by late November 2026.

- Quote NFIP and private flood together. Apply your county's CRS discount to the NFIP number, then compare against private carriers on price and on coverage (contents valuation, loss of use, deductible).

- Consider whether you still need Citizens at all. With the private market re-entering Florida, some homeowners can now leave Citizens for a private carrier — often bundling wind and flood more efficiently. A broker can run that comparison at the same time.

Frequently Asked Questions

Q: I'm a Citizens policyholder but my home is worth less than $400,000. Do I really have to buy flood?

A: Yes — by your first renewal on or after January 1, 2027, every Citizens personal-residential policy with wind coverage must carry flood insurance, regardless of value [1][3]. The only common exceptions are condo unit-owner (HO-6) policies, renter contents policies, and policies that exclude wind/hail [3].

Q: My home isn't in a flood zone. Am I exempt?

A: No. The Citizens requirement applies even to homes outside FEMA's high-risk flood zone [3]. Being in "Zone X" lowers your premium — it does not remove the requirement.

Q: What happens if I don't buy it, and how much do I need?

A: Failing to provide proof of a qualifying flood policy makes you ineligible for Citizens, so Citizens will non-renew your property policy — leaving you without windstorm protection during hurricane season [1][2]. You need flood coverage at least equal to your Citizens dwelling (Coverage A) limit, or the $250,000 NFIP maximum for a home, whichever is lower [1].

Q: Is private flood insurance allowed, or does it have to be NFIP?

A: A qualifying private flood policy satisfies the requirement, and for many newer or well-elevated First Coast homes it costs less than NFIP while offering broader coverage [6]. The right choice depends on your specific property — comparing both is the only way to be sure.

Related Reading

- The Citizens Exit Guide: What to Do When a Private Carrier Takes Out Your Policy — How Citizens depopulation works and how to evaluate a takeout offer.

- How Much Does Flood Insurance Cost in Florida? (2026 Guide) — NFIP vs. private pricing, sample quotes by county, and how Risk Rating 2.0 changes the math.

- Clay County's New FEMA Flood Maps Take Effect Spring 2027 — Why Orange Park, Fleming Island, and Middleburg homeowners may change flood zones right as the Citizens deadline hits.

- What Your Florida Homeowners Policy Actually Covers — and What It Doesn't — Why every Florida home policy excludes flood, and what gaps to fill.

- Hurricane Season 2026: What Every Florida Homeowner Needs to Know — Prep checklist and coverage-review timing for the June-to-November season.

How Atesa Risk Advisors Can Help

Atesa Risk Advisors is a Jacksonville-based, Florida-licensed (2-20 General Lines) independent brokerage serving homeowners across Duval, St. Johns, Clay, and Nassau counties. We are a RamseyTrusted provider and shop 40+ A-rated carriers — including NFIP write-your-own partners and the leading private flood markets — so we can quote your flood requirement both ways and tell you which one actually costs less for your home.

For Citizens policyholders facing the January 1, 2027 deadline, working with a broker who applies your CRS discount, compares NFIP against private flood, and checks whether you can leave Citizens for a private carrier altogether can easily save $300–$600 a year — and removes the risk of a surprise non-renewal during hurricane season.

Want a free Northeast Florida flood and Citizens-compliance review before your next renewal? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Citizens Property Insurance Corporation — Flood Insurance Requirements

[2] Citizens Property Insurance Corporation — New Flood Requirements Begin January 1

[3] News4JAX — Flood insurance will be mandatory for most Citizens policyholders by 2027

[4] St. Johns County — Floodplain Facts (CRS Class 5 / 25% discount)

[5] Nassau County, FL — Community Rating System (CRS)

[7] FEMA — National Flood Insurance Program Overview

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a construction background and a Master of Liberal Arts in Finance from Harvard University, he helps homeowners across Northeast Florida navigate flood, wind, and high-value coastal property risk.