Amelia Island Flood Insurance in 2026: The Nassau County CRS Discount That Can Cut Your Premium 15–25%

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 30, 2026

Key Takeaways

- Flood is never covered by a Florida homeowners policy. On a barrier island like Amelia, a separate flood policy is effectively unavoidable — and your mortgage lender almost certainly requires it if any part of your home sits in a mapped flood zone.

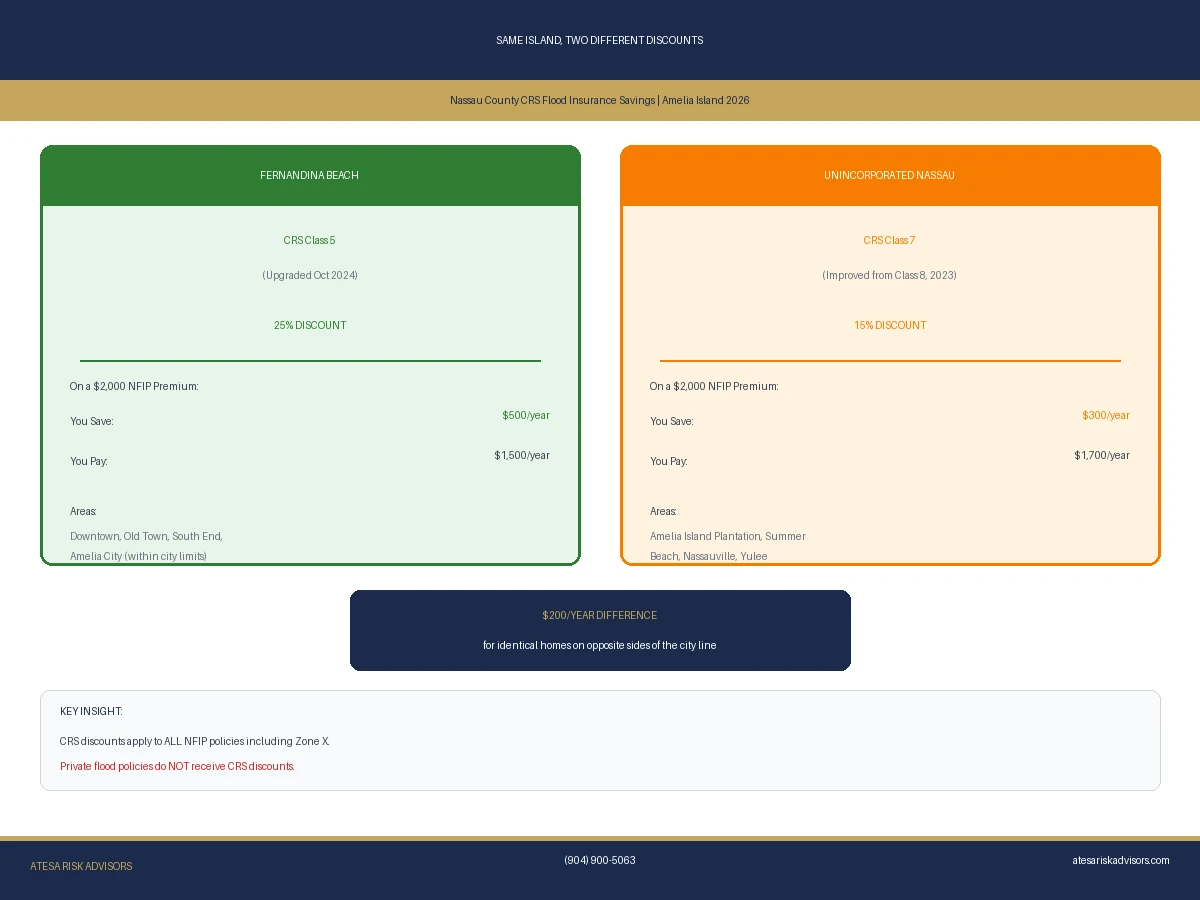

- Your community's Community Rating System (CRS) class sets an automatic discount on every National Flood Insurance Program (NFIP) policy in town. The City of Fernandina Beach is a CRS Class 5 (a discount of more than 25%), while unincorporated Nassau County is a CRS Class 7 (a 15% discount) [1][2][3].

- Same island, two different discounts. Whether your Amelia Island home sits inside the Fernandina Beach city limits or in unincorporated Nassau County decides whether you get the 25% break or the 15% break — a roughly 10-point gap on the same flood bill.

- Fernandina Beach improved from Class 6 (20% off) to Class 5 (25%+ off) for NFIP policies renewing on or after October 1, 2024, a change the city estimated would save local policyholders about $459,000 a year [2].

- Under FEMA's Risk Rating 2.0 pricing, the CRS discount now applies to every NFIP policy in the community — even homes mapped outside the high-risk Special Flood Hazard Area [4].

- The discount is automatic only if your policy is coded to the correct community. A policy accidentally written under the wrong jurisdiction quietly loses the discount — worth verifying line by line at renewal.

- NFIP's authorization is currently set to expire September 30, 2026 [5]. With private flood often cheaper than NFIP on the First Coast, this is the year to compare the two side by side rather than auto-renewing.

On Amelia Island, flood insurance is a near-certainty — your homeowners policy will not pay for rising water, and your lender will require a separate flood policy in most of the island's mapped zones. The good news is that both local governments earn you an automatic discount through FEMA's Community Rating System: the City of Fernandina Beach is rated CRS Class 5 (more than 25% off), and unincorporated Nassau County is rated Class 7 (15% off) [1][3]. Because that discount follows the city-limit line, two neighbors on the same street can pay very different premiums — and the discount only lands if your policy is coded to the right community. With NFIP set to expire September 30, 2026, 2026 is the year to confirm your discount and compare NFIP against private flood.

Why Flood Is the One Risk Your Amelia Island Homeowners Policy Will Never Cover

Every standard Florida homeowners (HO-3) policy excludes flood. Wind it covers; a tree through the roof it covers; rising water — storm surge off the Atlantic, the Amelia River backing up, sheet flooding from a stalled tropical system — it does not. That exclusion is universal across carriers, which is why flood is sold as a separate policy, either through the federal NFIP or a private flood insurer.

On a barrier island, that gap is not theoretical. Much of Amelia Island maps into FEMA's Special Flood Hazard Area (SFHA) — the AE and VE zones where there is at least a 1-in-4 chance of flooding over the life of a 30-year mortgage. If any part of your home sits in an SFHA and you carry a federally backed mortgage, your lender is legally required to make you buy flood coverage. Even off the high-risk zones, the marsh-and-creek geography of Nassau County means "low risk" is rarely "no risk." (For the broader picture of what your homeowners policy does and does not pay, see our guide to what a Florida homeowners policy actually covers.)

The Hidden Discount on Your Flood Bill: Nassau County's CRS Class

Here is the part most Amelia Island owners never hear about. FEMA runs a voluntary program called the Community Rating System (CRS), which rewards local governments that go beyond the minimum floodplain rules — better drainage, stricter building standards, public flood-risk education, open-space preservation. The reward is not paid to the city or county; it is passed straight through to residents as a discount on their NFIP flood premiums [4].

Communities are rated from Class 10 (no discount) down to Class 1 (the maximum 45% discount). Every step earns roughly 5 more percentage points off. Unincorporated Nassau County is currently a CRS Class 7, which delivers a 15% discount on NFIP policies countywide [3]. The county earned that rating by improving from Class 8 to Class 7 in 2023, after first joining the CRS in 2017 [3]. You do not apply for it and you do not fill out a form — if your home is in unincorporated Nassau County, the 15% is supposed to be baked into your NFIP premium automatically.

Same Island, Two Discounts: The Fernandina Beach City Line

The City of Fernandina Beach runs its own, better, CRS program. Fernandina Beach is a CRS Class 5, worth a discount of more than 25% for properties in the Special Flood Hazard Area [1]. The city reached Class 5 after completing its required five-year CRS audit, upgrading from Class 6 (a 20% discount); the improvement took effect for NFIP policies renewing on or after October 1, 2024, and the city estimated it would save local policyholders roughly $459,000 a year in combined premiums [2].

That creates a quirk unique to places like Amelia Island, where an incorporated city sits inside a participating county: your discount depends on which side of the city limit your parcel falls on. A home inside Fernandina Beach earns the 25%+ Class 5 discount; a home a few blocks away in unincorporated Nassau County earns the 15% Class 7 discount. On a $2,000 NFIP premium, that is the difference between roughly $500 and $300 off — about $200 a year for two otherwise identical houses. If you are not certain which jurisdiction your home is in, your property appraiser record or the city's flood-zone lookup will tell you, and it is worth confirming before you assume which discount you should be getting.

Risk Rating 2.0 Changed Who Gets the Discount

FEMA overhauled how it prices flood insurance with Risk Rating 2.0, the methodology that now sets every NFIP premium based on a property's specific characteristics — distance to water, elevation, rebuilding cost — rather than a one-size-fits-all flood-zone rate. The change quietly improved the CRS deal for many homeowners: under Risk Rating 2.0, the community's CRS discount applies to all NFIP policies in the community, including homes mapped outside the high-risk SFHA [4]. Previously, off-zone properties saw a much smaller CRS break.

For Amelia Island, that means even a home in an X zone (the lower-risk shading on the flood map) inside Fernandina Beach now benefits from the city's Class 5 discount on its NFIP policy. It also means the old advice to chase a flood-zone reclassification is less powerful than it used to be — your premium is now driven more by elevation and your home's individual risk than by the zone letter alone. An elevation certificate (a surveyor's record of how high your lowest floor sits relative to the expected flood height) can still help document a favorable rating, particularly for elevated coastal homes. (For how flood pricing works statewide, see how much flood insurance costs in Florida.)

The September 30, 2026 NFIP Deadline — and Why Private Flood Deserves a Look

There is a federal clock running in the background. The NFIP's authorization is currently set to expire September 30, 2026 [5]. Congress has reauthorized the program dozens of times on short-term extensions, and a lapse would not erase existing policies or stop claim payments on valid losses — but it would halt the sale and renewal of new NFIP policies, which can stall home closings [6]. It is not a reason to panic, but it is a reason to know where your coverage stands well before the fall.

It is also a reason to shop. The private flood insurance market has expanded rapidly in Florida, and on the First Coast a private policy is frequently cheaper than NFIP and offers higher limits than NFIP's $250,000 building cap. The trade-off is that private carriers do not pass through the CRS discount the way NFIP does, so the only way to know which wins for your specific home is to price both. That is exactly the kind of side-by-side an independent broker runs as a matter of course. (We break the two markets down in detail in our guide to private flood insurance vs. NFIP in Florida.)

What Amelia Island Owners Should Do Before Their Next Renewal

- Confirm your jurisdiction. Check whether your home is inside the City of Fernandina Beach (Class 5, 25%+) or in unincorporated Nassau County (Class 7, 15%). Your county property record or the city flood-map lookup will settle it.

- Read your NFIP declarations page. The CRS discount should appear as a line-item percentage. If you are in Fernandina Beach and see a 15% (or 0%) discount, your policy may be coded to the wrong community — flag it.

- Pull or update your elevation certificate if you own an elevated or waterfront home; it is the single best document for proving a favorable Risk Rating 2.0 result.

- Price NFIP against private flood ahead of the September 30, 2026 reauthorization date, comparing both premium and limits — not just the headline number.

- Don't auto-renew on autopilot. A barrier-island flood policy is too expensive to leave unexamined for another year.

Flood pricing on Amelia Island rewards the people who check the details — the right community code, the right elevation data, the right market. As an independent, RamseyTrusted brokerage, Atesa shops 40-plus A-rated carriers and runs NFIP against private flood side by side, and our founder's construction background means we read an elevation certificate the way an underwriter does. If you own on Amelia Island — or anywhere in Nassau County — let us confirm you are getting every discount you are owed before your next renewal.

Own on Amelia Island or anywhere in Nassau County and want to make sure you are getting every flood discount you are owed? Get a free flood-coverage review and quote at atesariskadvisors.com/get-quote or call (904) 900-5063.

Frequently Asked Questions

Does my homeowners insurance cover flooding on Amelia Island?

No. Every standard Florida homeowners policy excludes flood damage from rising water, including storm surge and coastal flooding. You need a separate flood policy through the NFIP or a private flood insurer. If any part of your home is in a mapped Special Flood Hazard Area and you have a federally backed mortgage, your lender will require it.

How much is the flood insurance discount in Fernandina Beach versus Nassau County?

The City of Fernandina Beach is a CRS Class 5 community, which provides a discount of more than 25% on NFIP flood premiums. Unincorporated Nassau County is a CRS Class 7, which provides a 15% discount. Whether you get the 25% or the 15% depends on whether your property sits inside the Fernandina Beach city limits.

Do I have to apply for the CRS flood discount?

No. The CRS discount is automatic and is built into your NFIP premium based on your community's class — you do not file anything. The catch is that your policy has to be coded to the correct community. If you live in Fernandina Beach but your declarations page shows the county's 15% instead of the city's 25%+, ask your agent to verify the community number.

When did Fernandina Beach's flood insurance discount improve to 25%?

Fernandina Beach upgraded from CRS Class 6 (a 20% discount) to CRS Class 5 (more than 25%) following its five-year CRS audit. The improved discount applies to NFIP policies that renew on or after October 1, 2024, and the city estimated the change would save policyholders about $459,000 a year.

Is the NFIP going away on September 30, 2026?

Not necessarily. The NFIP's authorization is currently set to expire September 30, 2026, but Congress has repeatedly extended it through short-term reauthorizations. Even if it lapses, existing policies stay in force and valid claims are still paid; the main effect of a lapse is that new policies cannot be issued or renewed, which can hold up home sales. It is a deadline to track, not a reason to drop coverage.

Is private flood insurance better than NFIP for an Amelia Island home?

It depends on the home. Private flood is often cheaper than NFIP on the First Coast and can offer building limits above NFIP's $250,000 cap, but private carriers do not pass through the CRS discount the way NFIP does. The only way to know which is cheaper for your property is to price both, which an independent broker can do in one sitting.

Sources

[1] City of Fernandina Beach — Flood Protection and Community Rating System

[2] Amelia Island Chamber of Commerce — Reduced Cost of Flood Insurance in the City of Fernandina Beach

[3] Nassau County, FL — Community Rating System (CRS)

[4] FEMA — National Flood Insurance Program Community Rating System

[5] National Association of Realtors — FAQ: National Flood Insurance Program Expires September 30, 2026

[6] FEMA — Congressional Reauthorization for the National Flood Insurance Program

Related Reading

- Private Flood Insurance vs. NFIP in Florida (2026): The September 30 Deadline, Risk Rating 2.0, and the $250,000 Gap

- How Much Does Flood Insurance Cost in Florida? (2026 Guide)

- The Citizens Flood Deadline: What Northeast Florida Coastal Homeowners Must Do Before January 1, 2027

- Do You Need Flood Insurance for a New Home in St. Johns County? The 2026 Nocatee, SilverLeaf & RiverTown Buyer's Guide

- What Is an Independent Insurance Agent? Why It Matters for Your Wallet

*Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a Master of Liberal Arts in Finance from Harvard University and a background in construction, he helps homeowners across Nassau, Duval, St. Johns, and Clay counties navigate flood, wind, and coastal property risk.