My Safe Florida Condo Grant 2026: The Northeast Florida Coastal Board's Guide to $175,000 in Hurricane-Hardening Matching Funds

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 23, 2026

Key Takeaways

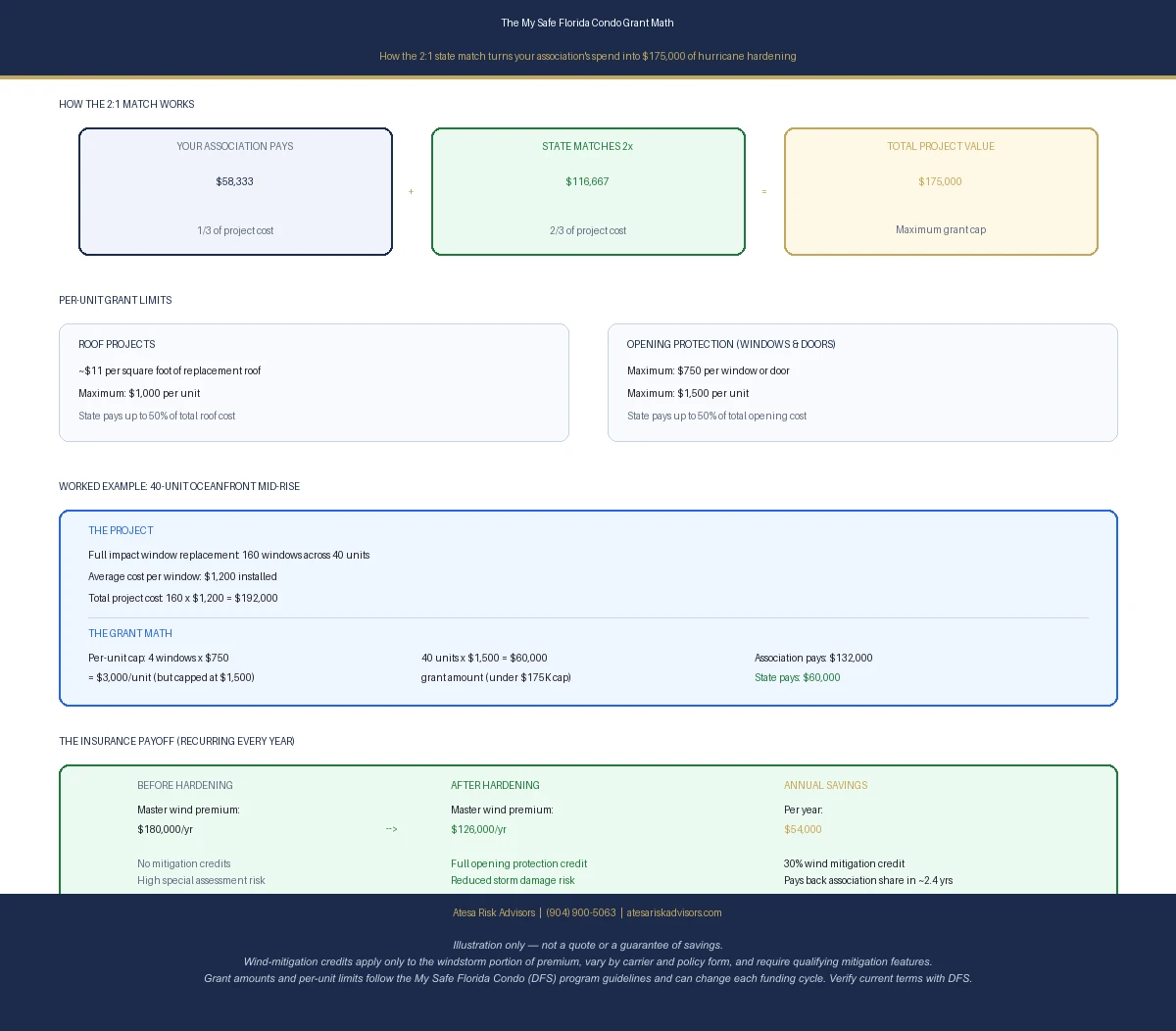

- The My Safe Florida Condo Pilot Program is a state grant that pays condominium associations $2 for every $1 they spend on hurricane hardening — impact-rated windows, exterior doors, and roof upgrades — up to a maximum of $175,000 per association [1][2].

- Eligibility reads almost like a description of the coastal Northeast Florida condo market: the building must be three stories or taller, have at least two residential units, and sit within 15 miles of the coastline [2].

- That captures the mid-rise and high-rise condos lining Jacksonville Beach, Neptune Beach, Atlantic Beach, Ponte Vedra Beach, St. Augustine Beach and Anastasia Island, and Amelia Island in Fernandina Beach — exactly the buildings getting hammered on their master wind policy.

- The grant starts with a free wind mitigation inspection paid for by the state [1]. That same inspection is the document an insurer uses to apply wind mitigation credits — discounts Florida law requires carriers to offer — to the master policy [6].

- Hardening the building does two things at once: it lowers the master windstorm premium (usually the single largest line item on a coastal association budget) and it reduces the special assessments owners absorb after a storm.

- Funding runs in limited cycles and has historically been claimed fast. Lawmakers reappropriated unused mitigation dollars in the 2026–2027 state budget [4][5], but boards that wait for the next hurricane scare end up competing against everyone else who waited too.

If you sit on a condo board anywhere along the Northeast Florida coast — from the Jacksonville Beaches down to St. Augustine Beach or up to Amelia Island — you have almost certainly watched your association's windstorm premium climb faster than any other cost on the budget. The My Safe Florida Condo Pilot Program is a state-funded matching grant that pays $2 for every $1 your association spends on impact windows, exterior doors, and roof hardening — up to $175,000 — and the same upgrades that earn the grant also qualify the building for the wind mitigation credits that lower your master policy. It is the rare program that cuts a capital cost and an insurance cost in the same move. Here is how it works, who qualifies, and why 2026 is the year to act.

Why This Grant Lands Hard in Coastal Northeast Florida

Coastal condo associations in our region are caught in a three-way squeeze. First, the master windstorm policy — the association's coverage for hurricane damage to the building structure — has repeated double-digit renewal increases since 2022, driven by a hardened reinsurance market and the concentration of insured value sitting a few hundred feet from the Atlantic. Second, Florida's post-Surfside reserve rules now force three-story-and-taller buildings to fully fund Structural Integrity Reserve Studies (SIRS), eliminating the waiver votes boards once used to keep dues low. Third, owners are absorbing the difference through higher dues and special assessments — the one-time charges levied when the budget or a claim outruns reserves.

The My Safe Florida Condo Pilot Program attacks the first and third of those pressures directly. By paying most of the cost of hurricane upgrades, it lets a building harden itself without a six-figure assessment, and the hardened building then earns a lower windstorm premium for years afterward. The eligibility rules — three stories or taller, within 15 miles of the coast [2] — were essentially written for the oceanfront and Intracoastal mid-rises of Duval, St. Johns, and Nassau counties.

What the My Safe Florida Condo Pilot Program Actually Pays For

The program, created under Florida Statute 215.55871 and administered by the Department of Financial Services through its contractor Michael Baker International, works in two stages [6].

Stage one is a free wind mitigation inspection. The state pays a licensed inspector to evaluate the building's roof covering, roof-to-wall connections, roof-deck attachment, and opening protection — the windows, exterior doors, and garage doors that keep storm-force wind and water out of the structure [1]. There is no cost to the association for the inspection, and it is yours to keep regardless of whether you proceed.

Stage two is the matching grant. For approved projects, the state contributes $2 for every $1 the association spends, capped at 50% of the project cost and a hard ceiling of $175,000 per association [1][2]. Within that, the program sets per-unit limits:

- Roof projects: roughly $11 per square foot of replacement roof, not to exceed $1,000 per unit, up to 50% of the cost [2].

- Opening protection (impact windows and doors): a maximum of $750 per replacement window or door, not to exceed $1,500 per unit, up to 50% of the cost [2].

For a mid-rise oceanfront building, the $175,000 ceiling is most efficiently spent on opening protection across the units or a major roof replacement that the reserve study was already pointing toward.

Does Your Building Qualify? The Eligibility Checklist

A condominium building generally qualifies if it meets all of the following [2][4]:

- It is three stories or taller.

- It has at least two residential units.

- It is located within 15 miles of the coastline — which covers essentially every beachside and Intracoastal condo from Fernandina Beach to St. Augustine Beach.

- It is not a development of detached units on separate parcels (true condominiums, not detached "condo" homes).

A 2026 bill (HB 1497) proposed steering the program toward older, pre-2008 buildings and lower-income complexes, but it died in committee, so no construction-year priority is in effect — any qualifying three-story-or-taller coastal building can apply. The underlying point still holds, though: the oceanfront and riverfront mid-rises built in Jacksonville Beach, Ponte Vedra, and on Anastasia Island during the 1980s, '90s, and early 2000s are exactly the buildings with the most to gain from hardening. The association — not the individual owner — applies, so the board needs to authorize the application and the matching spend through its normal budgeting process.

The Real Prize: A Lower Master Wind Policy

The grant pays for the upgrade, but the lasting value is on the insurance side. Florida law requires property insurers to offer premium discounts for hurricane loss mitigation, and the steepest credits apply to the two things this program funds: a code-compliant roof and full opening protection, meaning every window and exterior door is impact-rated or shuttered [6].

On a single-family home, comprehensive wind mitigation can take 20% to 40% off the windstorm portion of the premium. On a master condo policy the dollars at stake are larger, and a credit recurs for as long as the building stays hardened — but master-policy credits are not a fixed percentage. They depend on the carrier, the policy form, and whether the building reaches full opening protection, so they have to be quoted, not assumed. In practice, a board that uses the grant to bring a building to full opening protection is often making a documented case for a materially lower renewal at the same time it cuts the special-assessment risk that uninsured hurricane damage would create.

I came up in construction before I came into insurance, so I look at a coastal condo the way an underwriter and a builder both would: the cheapest claim is the one the building's envelope never lets happen. When the state is willing to pay two-thirds of the cost to get a 1990s oceanfront mid-rise to full impact protection, and that same work resets the master wind premium for years, a board that lets the window close is leaving money on the table twice.

— Ricardo Alonso, Founder, Atesa Risk Advisors

Why 2026 Is the Year to Move

This is a pilot program with a finite appropriation, not a permanent entitlement, and it has historically run through its funding quickly once boards realize what it offers. The encouraging news for 2026 is that the Legislature reappropriated unused mitigation dollars in the 2026–2027 state budget to keep both the My Safe Florida Home and the My Safe Florida Condo Pilot programs running [4][5]. The discouraging news is that there is a backlog of completed inspections statewide waiting on grant dollars, which means the associations that get their inspection scheduled and their application in early are the ones most likely to be funded.

There is also a calendar reason that is specific to condo boards. Most three-story-plus Northeast Florida buildings have already completed — or are completing — their SIRS and milestone inspections, so reserve plans for roofs and major components are fresh. That is the ideal moment to fold a grant-funded roof or window project into the capital plan, because the engineering work is already done and the board can match the grant against money it was going to spend anyway.

How a Coastal Northeast Florida Board Should Approach This — Step by Step

- Confirm the building fits the profile. Three or more stories, two or more units, within 15 miles of the coast. Nearly every beachside mid-rise in our region clears this bar.

- Request the free state inspection through the program portal or by contacting the Department of Financial Services condo pilot team. There is no cost and no obligation.

- Match the inspection to your reserve study. If your SIRS already flags the roof or aging single-pane windows, you have found the project the grant should fund.

- Get your insurance review running in parallel. Before you spend, have your broker confirm how the planned upgrades will move your wind mitigation credits and model the master-policy savings — so the board is voting with the full picture.

- Apply early in the funding cycle. Funding is limited and claimed in order; a completed application beats a good intention.

- Document everything for the carrier. Keep the wind mitigation inspection, permits, and product approvals — they are what convert the construction work into a lower renewal.

Frequently Asked Questions

What is the My Safe Florida Condo Pilot Program?

It is a Florida state program that gives condominium associations a free wind mitigation inspection and a matching grant — $2 of state money for every $1 the association spends — to pay for hurricane-hardening upgrades such as impact windows, impact-rated exterior doors, and roof improvements. The grant is capped at 50% of project cost and a maximum of $175,000 per association.

Which Northeast Florida condos are eligible?

Buildings that are three stories or taller, have at least two residential units, and sit within 15 miles of the coastline. That covers the great majority of oceanfront and Intracoastal condos in Jacksonville Beach, Neptune Beach, Atlantic Beach, Ponte Vedra Beach, St. Augustine Beach, Anastasia Island, and Amelia Island.

How much can our association actually receive?

The state pays $2 for every $1 the association spends, up to 50% of the project and a hard cap of $175,000 per association. Within that, roof work is limited to about $1,000 per unit and opening protection to $1,500 per unit. The exact figure depends on your building's size and the scope of the upgrade.

Will this actually lower our master insurance premium?

It can, and that is the point. Florida law requires insurers to offer premium discounts for verified hurricane mitigation, and the largest credits apply to a compliant roof and full opening protection — precisely what the grant funds. Once the wind mitigation inspection documents the upgrades, your broker can present them to the carrier at renewal. Savings vary by building, so model them before you commit.

Does the individual unit owner apply, or the association?

The association applies. Because the upgrades involve the building's common-element roof and exterior openings, the board must authorize the application and the matching spend through its normal budget and voting process. Individual owners benefit through lower dues and reduced assessment risk, not by applying themselves.

Is funding still available in 2026?

The program is a pilot with a limited appropriation, and the 2026–2027 state budget reappropriated unused mitigation funds to keep it operating. Because demand is high and there is a statewide backlog of completed inspections, availability can change quickly — confirm the current cycle status before planning around any deadline, and get your inspection and application in early.

How Atesa Risk Advisors Can Help

At Atesa Risk Advisors, we work the insurance side of this equation for coastal Northeast Florida condo boards. Before your association spends a dollar matching the grant, we review your current master wind policy, model how the planned roof or opening-protection upgrades will move your wind mitigation credits, and shop the renewal across our panel of A-rated carriers so the board can see the premium impact alongside the construction cost. After the work is done, we make sure the wind mitigation inspection and product approvals are documented the way underwriters want them — so the savings actually show up on the renewal rather than getting lost in the paperwork.

As an independent, RamseyTrusted brokerage that represents more than 40 carriers rather than a single company, we are positioned to put your hardened building in front of the markets most likely to reward it. That independence matters most on a master condo policy, where the difference between carriers on a well-mitigated coastal building can run into tens of thousands of dollars a year.

Sit on a condo board in Jacksonville Beach, Ponte Vedra, St. Augustine Beach, Amelia Island, or anywhere along the Northeast Florida coast? Get a free review of your master wind policy and mitigation strategy at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] My Florida CFO — My Safe Florida Condo Pilot Project (official program page)

[3] My Florida CFO — CFO Patronis Launches the 'My Safe Florida Condo' Pilot Program (press release)

[4] Florida House of Representatives — CS/HB 1497 (2026): My Safe Florida Condominium Pilot Program

[5] WCTV — Senate approves changes to My Safe Florida Condo Pilot Program (2026)

[6] Florida Office of Insurance Regulation — Premium Discounts for Hurricane Loss Mitigation

[7] Michael Baker International — My Safe Florida Condominium Pilot Program

Related Reading

- SIRS Compliance or Non-Renewal? The 2026 Board Member's Guide to Structural Reserves

- Florida Statute 718 Insurance Requirements: What Every HOA Board Member Must Know (2026 Guide)

- Florida Condo Loss Assessment Coverage: What It Is and the 3 Most Common Claims (2026)

- How Much Does Condo Association Insurance Cost in Florida? (2026 Guide)

- Roof Age and Your Northeast Florida Home Insurance in 2026: The 15-Year Rule, Wind Mitigation, and the Grant That Saves Your Policy

- Small Building, Big Deadlines: The 2026 Survival Guide for 25-50 Unit Condo Boards

Pairing a grant-funded retrofit with the right condo & HOA insurance for Northeast Florida associations is how boards turn hardening dollars into lower master-policy premiums.

*Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a Master of Liberal Arts in Finance from Harvard University and a background in construction, he helps condo associations and boards across Jacksonville, St. Johns County, and Northeast Florida lower master-policy costs through smart mitigation and competitive shopping.