Florida Condo Loss Assessment Coverage: What It Is and the 3 Most Common Claims (2026)

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 20, 2026

Key Takeaways

- Loss assessment coverage is an add-on to your Florida condo (HO-6) policy that pays your share of a special assessment when your association bills every owner to cover a loss its master policy does not fully pay [1].

- It responds only to a covered loss — storm, fire, or similar damage to the shared property, or a liability judgment against the association. It does not pay for maintenance or structural-reserve assessments.

- Florida law requires every HO-6 policy to include at least $2,000 of this coverage, and the policy pays up to the limit you buy [1].

- A higher limit mainly protects you against larger covered losses and liability claims; your share of the association's master-policy deductible is separately limited under the standard form [1].

- The three claims that trigger it most often in Florida: hurricane or windstorm damage to common areas, a liability judgment against the association, and fire or water damage to shared property.

Loss assessment coverage is the part of your Florida condo (HO-6) policy that pays your individual share of a special assessment when the association charges every owner to cover a loss its master policy cannot fully absorb. It applies only when that assessment traces back to a covered event — storm or fire damage to shared property, or a liability claim against the association — not to maintenance or reserve shortfalls. Florida requires at least $2,000 of it on every unit-owner policy, and you can carry more.

If you own a Florida condo, your protection comes from two policies working together. The association carries a master policy on the building and shared spaces; your HO-6 covers the inside of your unit and your personal liability. Loss assessment coverage is the bridge between them — it answers for the moment the association turns to owners to help pay for a shared loss. Here is what it is, how it helps your association recover, and the three situations that trigger it most.

What Loss Assessment Coverage Actually Is

Florida law requires your association to maintain a master policy on the common elements and, in most buildings, the original interior of each unit [2]. That policy has limits and a deductible. When a covered loss costs more than the master policy pays — because it runs past the policy's limit, or, more often, because of the policy's deductible — the association can levy a special assessment, charging every owner a share of the shortfall.

Loss assessment coverage on your HO-6 pays your share of that assessment, up to the limit you carry. Florida sets a floor: every unit-owner policy must include at least $2,000 of loss assessment coverage, and the policy pays up to whatever limit you buy above that [1]. The phrase that governs everything is covered loss — the assessment has to trace back to a peril your policy insures, such as windstorm or fire. If it does, you have a claim. If it does not, you do not.

How It Helps Your Association — and You

After a covered loss, an association has to raise money quickly to repair shared property and keep the building whole, and its main tool is the special assessment. When owners carry loss assessment coverage, they can pay their share through their HO-6 instead of out of savings — which helps the association collect what it needs and keep the repair on schedule. For you, the coverage turns a sudden, unbudgeted bill into an insurance claim. A single hurricane assessment on a coastal building can reach five figures per unit, and this is the coverage that stands between that notice and your own bank account.

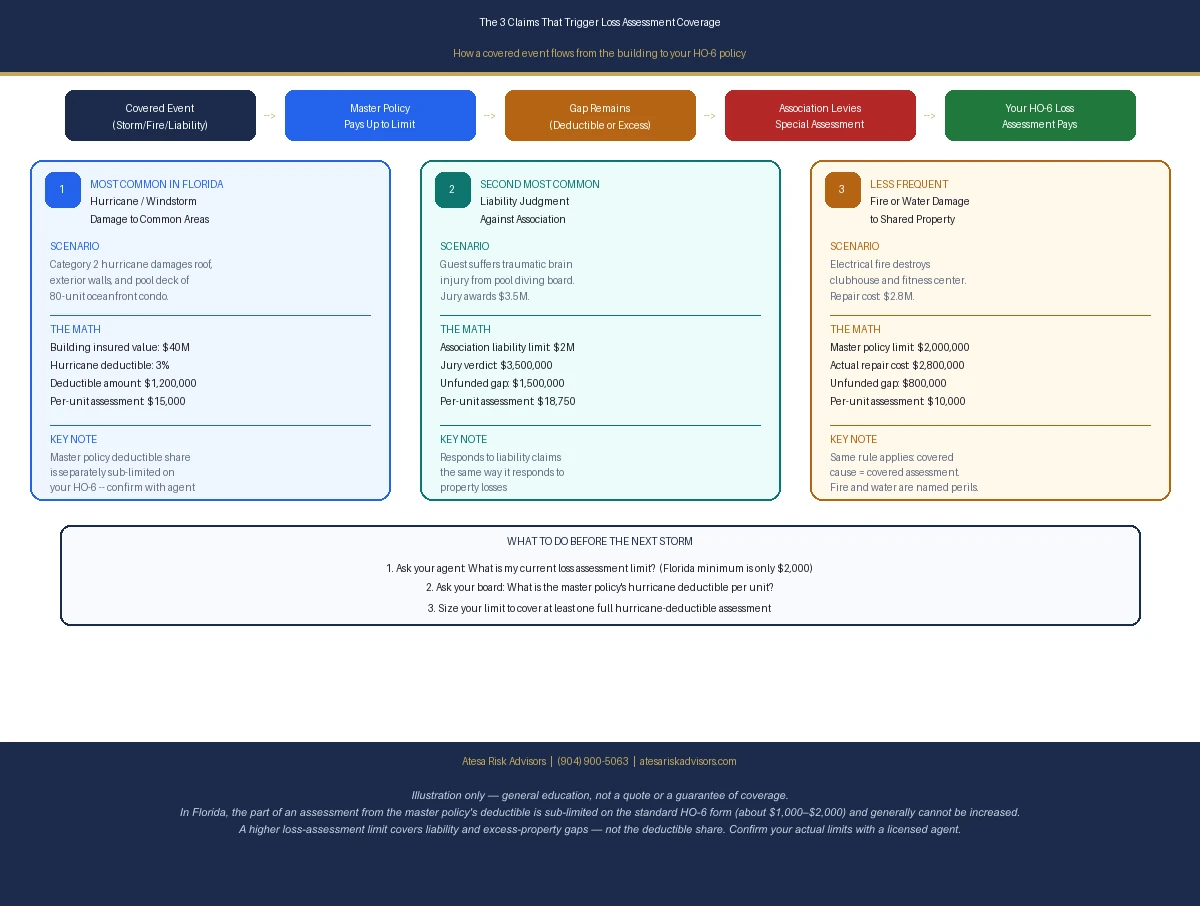

The Three Most Common Loss Assessment Claims

1. Hurricane or windstorm damage to the common areas

This is the one Florida owners face most. Master policies here carry a hurricane deductible set as a percentage of the building's insured value — commonly 2% to 5% — which on a large building can be hundreds of thousands of dollars the master policy will not pay. After a storm, the association assesses owners to fund that gap. Because windstorm is a covered peril, your loss assessment coverage responds to your share. One detail to confirm on your own policy: the portion of an assessment tied specifically to the association's master-policy deductible is separately limited under the standard unit-owner form, so ask your agent exactly how much of your limit applies to it.

2. A liability claim against the association

If someone is seriously injured in a common area — a fall on a wet walkway, a pool accident, an elevator failure — and the resulting judgment or settlement is larger than the association's liability coverage, the association can assess owners for the difference. Loss assessment coverage can pay your share of that liability assessment, the same way it responds to a property loss.

3. Fire or water damage to shared property

A fire in the clubhouse, or water from a burst pipe in the common plumbing, can damage shared structures beyond what the master policy covers. When the association assesses owners to close that gap, your loss assessment coverage responds, because the cause is a covered peril. These claims are less frequent than hurricane assessments, but they follow the same rule: a covered cause makes for a covered assessment.

What It Will Not Pay

Loss assessment coverage insures losses, not upkeep. It does not pay assessments for milestone-inspection repairs, structural-reserve shortfalls under Florida's Structural Integrity Reserve Study requirements [3], concrete restoration, code upgrades, deferred maintenance, or a board's decision to renovate. Those are maintenance and capital obligations, not insured losses — and they account for many of the assessments Florida owners are seeing now, which is why so many are surprised to learn this coverage does not apply to them. Knowing the line in advance lets you plan for both kinds of assessment instead of assuming one policy covers everything.

Most owners I talk to assume the association's master policy and their own HO-6 already have the whole building covered. The assessment notice after a storm is usually where they find the gap — and whether they carry loss assessment coverage decides if that notice becomes an insurance claim or a check they write themselves.

— Ricardo Alonso, Founder, Atesa Risk Advisors

Frequently Asked Questions

What is loss assessment coverage on a condo policy?

It is an add-on to your HO-6 unit-owner policy that pays your share of a special assessment the association levies after a covered loss to shared property, or after a liability judgment against the association. It pays up to the limit you carry.

Does loss assessment coverage pay for any special assessment?

No. It pays only assessments that trace back to a covered loss, such as windstorm or fire damage to the common elements, or a liability claim against the association. Assessments for maintenance, repairs, or reserves are not covered.

What are the most common loss assessment claims in Florida?

Three lead the list: hurricane or windstorm damage to the common areas (usually the master policy's hurricane deductible passed on to owners), a liability judgment against the association that exceeds its coverage, and fire or water damage to shared property beyond what the master policy pays.

How much loss assessment coverage should I carry?

Florida requires at least $2,000, but that is a floor. Many owners carry more to protect against larger covered losses and liability assessments. Your share of the master-policy deductible is separately limited, so size the coverage with an agent who has read your association's master policy.

Does loss assessment coverage pay for hurricane damage to my building?

It pays your share of an assessment the association charges after windstorm damage to the common areas, up to your limit, with the deductible-related portion separately limited. It does not cover damage inside your own unit — that is the rest of your HO-6 policy.

Does it cover SIRS or milestone-inspection assessments?

No. Structural-reserve shortfalls, milestone-inspection repairs, and concrete restoration are maintenance and reserve obligations, not insured losses, so loss assessment coverage does not respond to them.

How Atesa Risk Advisors Can Help

Loss assessment coverage is inexpensive, but getting it right takes reading the documents most owners never see. We pull your association's master-policy declarations to find its deductible and limits, set your loss assessment coverage to the exposure that actually applies to you, and confirm how your policy treats the deductible portion — so the number on your declarations page means what you think it means. We place your HO-6 and loss assessment coverage alongside your other policies, and when an assessment notice arrives, we help you determine whether it is a covered claim before you pay it.

As an independent, RamseyTrusted brokerage, we work for you rather than one carrier — which matters on a coverage where the right limit depends entirely on your specific building.

Own a Florida condo and not sure your loss assessment coverage fits your building? Get a free policy review and quote at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] The 2025 Florida Statutes — Section 627.714, Residential condominium unit owner coverage

[2] The 2025 Florida Statutes — Section 718.111(11), Condominium association insurance requirements

[4] Insurance Information Institute — Condo Insurance

Related Reading

- How Much HO-6 Coverage Do You Need? The Florida Condo Sizing Guide — where loss assessment fits in the full HO-6 sizing decision, including the deductible-portion sublimit.

- Florida Personal Umbrella Insurance in 2026 — broader liability protection that pairs with your HO-6

- What Your Florida Homeowners Policy Actually Covers — how the unit-owner policy fits together

- What Does Your Condo HO-6 Policy Actually Cover? The Florida Walls-In Guide — the complete walls-in picture of what an HO-6 insures beyond the loss assessment line

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a Master of Liberal Arts in Finance from Harvard University and a background in construction, he helps Florida condo owners and associations place coverage that actually fits the building.