Roof Age and Your Northeast Florida Home Insurance in 2026: The 15-Year Rule, Wind Mitigation, and the Grant That Saves Your Policy

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 9, 2026

Key Takeaways

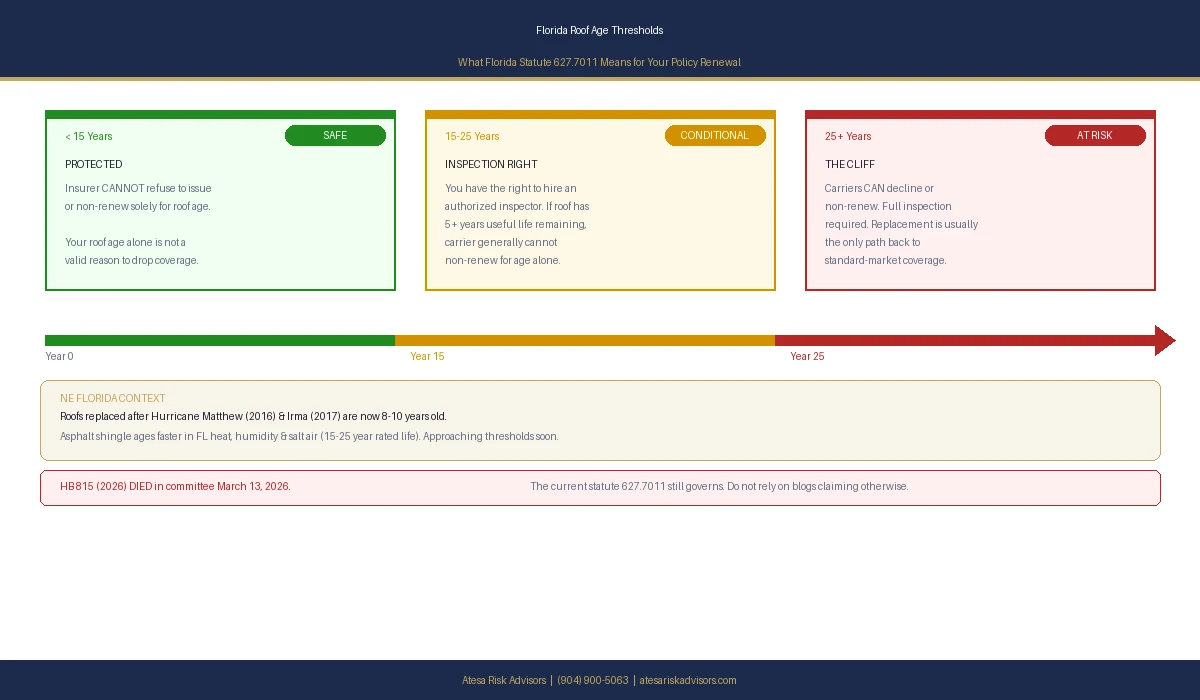

- Under Florida law (Statute 627.7011), an insurer cannot refuse to issue or non-renew your policy solely because your roof is less than 15 years old. Roof age alone is not a valid reason to drop a newer roof.

- Once a roof passes 15 years, you have the right to hire an authorized inspector. If the inspection shows the roof has at least 5 years of useful life remaining, the carrier generally cannot non-renew you for age alone.

- The real cliff is 25 years. Florida law lets carriers decline or non-renew roofs older than 25 years — and the wave of roofs replaced after Hurricanes Matthew (2016) and Irma (2017) is now aging into the danger zone across Duval, St. Johns, Clay, and Nassau counties.

- HB 815, the 2026 bill that would have added new roof-age protections, died in committee on March 13, 2026. Several roofing and law-firm blogs incorrectly claim it took effect July 1, 2026. It did not. The current statute still governs.

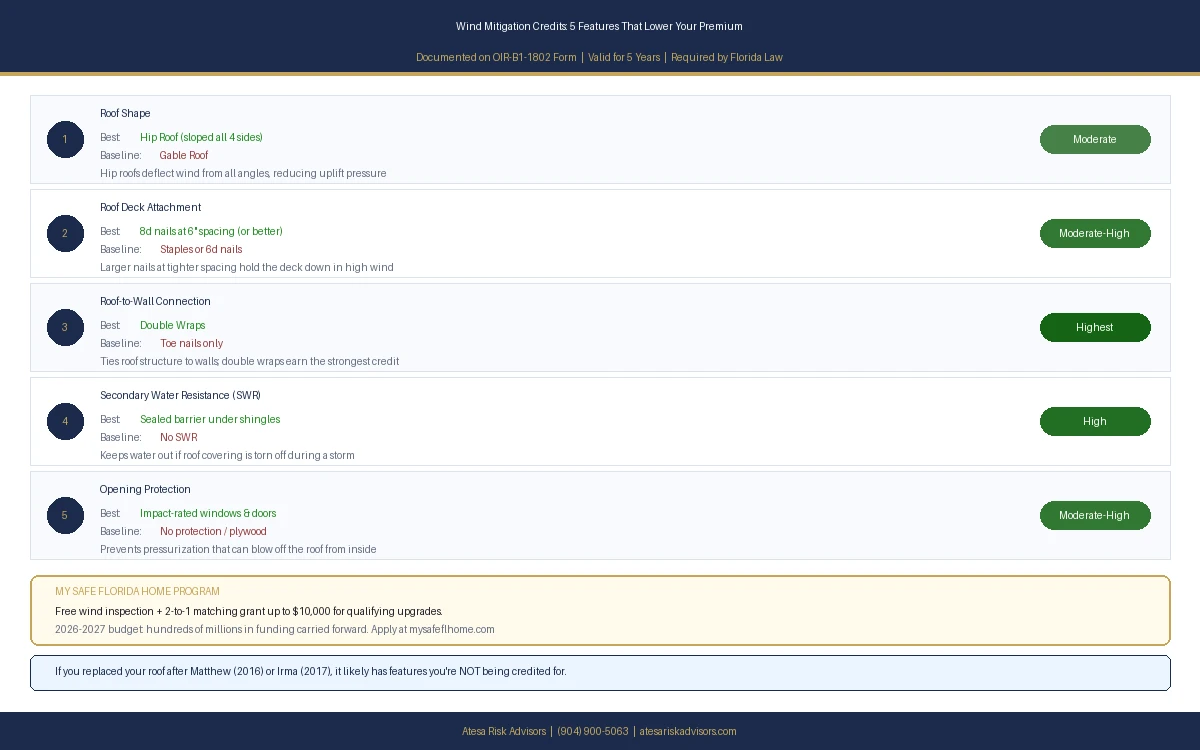

- A wind mitigation inspection (documented on the state Uniform Mitigation Verification form, OIR-B1-1802) is the single highest-value move for a coastal Northeast Florida home — credits for roof shape, deck attachment, roof-to-wall connections, and a secondary water barrier can cut the wind portion of your premium substantially and keep an older roof insurable.

- The My Safe Florida Home program offers a free wind inspection and a 2-to-1 matching grant up to $10,000 for qualifying upgrades. The 2026–2027 state budget carried hundreds of millions of dollars in funding forward, so the program remains active in 2026.

- When a roof ages out, an independent broker who shops 40-plus A-rated carriers and documents your mitigation features is often the difference between a renewal offer and a non-renewal letter.

In Northeast Florida, the age of your roof is the single most common reason homeowners get non-renewed — and in 2026 the rules have not loosened. Florida law (Statute 627.7011) bars an insurer from dropping you solely because your roof is under 15 years old, and once the roof passes 15 years you have the right to an inspection that can keep your policy in force if the roof has at least five years of useful life left. A bill that would have expanded those protections, HB 815, died in committee in March 2026, so the existing statute still controls. The fastest ways to protect your coverage and lower your premium are a wind mitigation inspection and the My Safe Florida Home grant.

Why Roof Age Is the #1 Reason Northeast Florida Homeowners Get Non-Renewed

Carriers writing homeowners policies in Duval, St. Johns, Clay, and Nassau counties live and die by hurricane wind risk, and the roof is the part of your home that takes the storm first. An older or worn roof is the strongest predictor of a future claim, so when a carrier trims its exposure in our coastal market, aging roofs are the first policies it sheds.

The timing matters locally. After Hurricane Matthew in 2016 and Hurricane Irma in 2017, tens of thousands of Northeast Florida homeowners replaced storm-damaged roofs. Those roofs are now eight to ten years old. Asphalt shingle — the most common covering here — is typically rated for 15 to 25 years, and in our heat, humidity, and salt air it ages on the faster end of that range. In other words, a large cohort of First Coast roofs is approaching the exact thresholds that govern whether a policy gets renewed. Understanding those thresholds is no longer optional.

What Florida Law Actually Says About Roof Age

Florida Statute 627.7011 sets the rules every admitted carrier and Citizens must follow. There are three numbers that matter.

Under 15 years — protected. An insurer may not refuse to issue or refuse to renew a homeowners policy solely because of the age of the roof if the roof is less than 15 years old [1]. If your roof is newer than 15 years and a carrier tries to drop you citing roof age, that is not a lawful reason on its own.

15 to 25 years — your right to an inspection. Once a roof reaches 15 years, the carrier can ask for a roof inspection before renewing. But the statute cuts both ways: you have the right to have an authorized inspector assess the roof, and if that inspection shows the roof has 5 or more years of useful life remaining, the insurer generally may not refuse to renew based on age alone [1]. This is the provision most homeowners do not know they have — and it is exactly where an independent broker earns their keep, because the inspection has to be ordered, documented, and submitted correctly.

Over 25 years — the cliff. For roofs older than 25 years, carriers are permitted to require a full inspection and may decline or non-renew. This is the hard edge of the market. If your roof is in this range, a replacement is usually the only path back to standard-market coverage.

Separately, Senate Bill 4-D (2022) reshaped repair-versus-replace economics through the so-called 25% rule. For roofs built or updated to the 2007 Florida Building Code or later, only the damaged section generally needs to be brought up to code rather than the entire roof — a meaningful break for newer homes after a partial-damage storm [2]. Older roofs do not get that flexibility.

The 2026 Roof Bill That Died — and Why the Confusion Matters

Here is where Northeast Florida homeowners are being misled online. During the 2026 legislative session, House Bill 815 ("Roofing Requirements for Property Insurance") proposed expanding roof-age protections — among other things, sharpening the distinction between low-slope and steep-slope roofs and strengthening a homeowner's right to an inspection before forced replacement.

HB 815 did not pass. It died in the Insurance & Banking Subcommittee on March 13, 2026 [3]. There is no chapter law, and the Governor did not sign it. Despite that, a number of roofing-contractor and law-firm blog posts confidently state that HB 815 "took effect July 1, 2026." That is incorrect, and acting on it could cost you. The law that governs your renewal today is the existing Statute 627.7011 described above — not a bill that failed in committee. If a contractor pressures you into a decision by citing "the new July 2026 roof law," treat that as a reason to get a second opinion.

Wind Mitigation: The Inspection That Can Save You Hundreds — or Your Policy

In coastal Northeast Florida, the wind portion of your premium is often the largest single piece of the bill. The good news: Florida requires carriers to give premium credits for construction features that make your home more wind-resistant, and the way you capture those credits is a wind mitigation inspection.

A licensed inspector documents your home on the state's Uniform Mitigation Verification Inspection Form (OIR-B1-1802), which is valid for five years. The features that move the needle most:

- Roof shape — a hip roof (sloped on all four sides) earns a larger credit than a gable roof.

- Roof deck attachment — larger nails (8d) at tighter spacing hold the deck down in high wind.

- Roof-to-wall connection — clips, single wraps, or double wraps that tie the roof structure to the walls; double wraps earn the strongest credit.

- Secondary water resistance (SWR) — a sealed barrier under the shingles that keeps water out if the covering is torn off.

- Opening protection — impact-rated windows and doors or code-approved shutters.

For many First Coast homes, a single mitigation inspection pays for itself many times over, and it can be the deciding factor in whether a carrier will write an older roof at all. If you replaced your roof after Matthew or Irma, there is a good chance it was built to current code with features you are not yet being credited for. Documenting them is found money. (For the bigger picture on what drives your bill, see our guide to how much homeowners insurance costs in Florida.)

The My Safe Florida Home Grant: Free Inspection + Up to $10,000

If your roof or openings need upgrading to stay insurable, the state-run My Safe Florida Home (MSFH) program can help pay for it. The program offers eligible homeowners a free wind mitigation inspection and a 2-to-1 matching grant — the state contributes $2 for every $1 you spend on qualifying improvements, up to a $10,000 grant [4].

Qualifying improvements typically include roof upgrades, opening protection (impact windows, doors, and shutters), and reinforced garage and entry doors — the same features that drive wind mitigation credits. So the grant does double duty: it hardens your home against the next storm and helps you qualify for premium discounts and keep coverage on an aging roof.

Funding is the key question every year, and 2026 is favorable: the 2026–2027 state budget carried hundreds of millions of dollars in unused MSFH funds forward, much of it aimed at clearing the application backlog [4]. Demand is high and dollars are finite, so check the official program portal at mysafeflhome.com for current application windows and confirm your eligibility before counting on the grant.

What Northeast Florida Homeowners Should Do Right Now

With the 2026 hurricane season already underway — NOAA forecasts a below-normal season but stresses that it only takes one storm to make landfall [5] — this is the window to get ahead of your renewal, not after a non-renewal letter arrives.

- Find your roof's true age and remaining life. Pull your permit or replacement records. If the roof is approaching 15 or 25 years, you are in decision territory.

- Order a wind mitigation inspection if you do not have a current one (or yours is older than five years). Make sure every feature you qualify for is captured on the OIR-B1-1802 form.

- Apply to My Safe Florida Home before you pay out of pocket for upgrades you might otherwise have gotten matching funds for.

- If you are non-renewed, do not panic — and do not auto-default to Citizens. An independent broker can often place an aging-roof home with a private A-rated carrier once the mitigation and inspection paperwork is in order.

Roof age is a solvable problem when you address it early and document it properly. As an independent, RamseyTrusted brokerage, Atesa shops 40-plus A-rated carriers — and our founder's construction background means we read a roof report the way an underwriter does. If your renewal is coming up or you have already gotten a notice, let us look at your options before the clock runs out.

Frequently Asked Questions

Can my insurance company drop me just because my roof is old?

Not if your roof is under 15 years old — Florida Statute 627.7011 prohibits non-renewal based solely on the age of a roof younger than 15 years. For roofs 15 years and older, the carrier can request an inspection, but if an authorized inspector finds at least 5 years of useful life remaining, the insurer generally cannot non-renew you for age alone. Roofs older than 25 years can be declined.

Did Florida pass a new roof-age insurance law that takes effect July 1, 2026?

No. HB 815, the 2026 bill that would have expanded roof-age protections, died in the Insurance & Banking Subcommittee on March 13, 2026, and was never signed into law. Blog posts claiming a new roof law took effect July 1, 2026 are inaccurate; the existing Statute 627.7011 still governs.

How old can a roof be to get homeowners insurance in Florida?

Most standard carriers will write a roof up to about 15 years without an inspection, will require an inspection between 15 and 25 years, and may decline roofs older than 25 years. Asphalt shingle roofs in Northeast Florida often need replacement near the 20-year mark due to heat, humidity, and salt exposure, so plan ahead as you approach these thresholds.

What is a wind mitigation inspection and how much can it save me?

A wind mitigation inspection documents storm-resistant features of your home — roof shape, deck attachment, roof-to-wall connections, secondary water resistance, and opening protection — on the state Uniform Mitigation Verification form (OIR-B1-1802). Because the wind portion of a coastal Northeast Florida premium is so large, these credits can produce meaningful savings and, just as importantly, can make an older roof insurable. The form is valid for five years.

Does the My Safe Florida Home program still have funding in 2026?

Yes. The program is active in 2026, and the 2026–2027 state budget carried significant unused funds forward to address the application backlog. It offers a free wind inspection and a 2-to-1 matching grant up to $10,000 for qualifying upgrades, but funding is limited and applications open in income- and age-based windows, so check mysafeflhome.com for current availability.

My roof was replaced after Hurricane Matthew or Irma — am I in good shape?

Likely yes, but confirm it. Roofs replaced in 2016–2017 are now eight to ten years old and were generally built to modern code, which means they may include mitigation features you are not yet being credited for. Order a wind mitigation inspection so those features are documented and reflected in your premium.

If I get non-renewed over my roof, is Citizens my only option?

No. Citizens is the state-backed insurer of last resort, but an aging-roof home can often be placed with a private A-rated carrier once a wind mitigation inspection and any required roof inspection are completed and submitted. An independent broker can shop your risk across many carriers rather than leaving you to default into Citizens.

Sources

[2] Citizens Property Insurance Corporation — Roof Rule Changes

[4] My Safe Florida Home — Official Program Portal

[5] NOAA — NOAA Predicts Below-Normal 2026 Atlantic Hurricane Season

[6] The 2025 Florida Statutes — Section 553.844, Windstorm loss mitigation; requirements

Related Reading

- Wildlight Is Adding 4,000 Homes: The Yulee New-Construction Home Insurance Guide for Nassau County Buyers (2026) — why a new Wildlight build is one of the cheapest homes to insure in Northeast Florida, and how to document it.

- Clay County Homeowners Insurance in 2026: The Inland Advantage and New-Construction Credits

- How Much Is Homeowners Insurance in Florida? The Surprising 2026 Reality

- What Your Florida Homeowners Policy Actually Covers (and What It Doesn't)

- Hurricane Season 2026: What Every Florida Homeowner Needs to Know

- The Citizens Flood Deadline: What Northeast Florida Coastal Homeowners Must Do Before January 1, 2027

- What Is an Independent Insurance Agent? Why It Matters for Your Wallet

- Is Your Florida Home Underinsured? The 2026 Replacement-Cost Gap That Leaves Owners Paying to Rebuild — how a roof on an ACV settlement fits the larger replacement-cost picture.

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a Master of Liberal Arts in Finance from Harvard University and a background in construction, he helps homeowners across Northeast Florida navigate roof-age, wind, and coastal property risk.