Florida Restaurant Insurance 2026: The Liquor Liability Gap That Can Close Your Doors

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 4, 2026

Key Takeaways

- Your general liability (GL) policy does not cover alcohol claims. Every standard commercial GL form contains a built-in liquor liability exclusion, so a single over-service lawsuit can be 100% uninsured unless you carry a separate liquor liability policy or endorsement.

- Florida's dram shop law (Statute § 768.125) is one of the most vendor-friendly in the country — you generally cannot be sued for serving a sober-appearing adult — but it still leaves two large exposures wide open: serving anyone underage and "knowingly" serving someone habitually addicted to alcohol.

- The threshold that reclassifies you from "restaurant" to "bar" for insurance is not the same one that governs your liquor license. Carriers re-rate you as a tavern when alcohol passes roughly 35–40% of sales; the state's special restaurant license requires food to be at least 51% of revenue.

- A Florida full-service restaurant bundle (GL, liquor liability, property, business interruption, workers' comp, and spoilage) typically runs $6,000–$15,000+ per year, with coastal wind and flood exposure the biggest swing factors.

- Assault-and-battery (A&B) sublimits are tightening. Many liquor policies now cap A&B at $250,000–$500,000 even on a $1 million policy — a critical detail for any venue with late-night hours or live entertainment.

- Hurricane losses for restaurants are rarely about the building. Spoiled inventory, a percentage wind deductible (2–5% of building value), and weeks of lost income from a power outage or evacuation are where restaurants actually get hurt — and each requires a specific coverage to respond.

- These exposures interact. The right bundle is assembled, not bought off a website — how a Florida broker classifies your alcohol ratio, structures your A&B limit, and sets your business-interruption period determines whether a claim is paid or denied.

Florida restaurant insurance is a bundle of coverages — general liability, liquor liability, commercial property, business interruption, workers' compensation, and food spoilage — built around one fact most owners miss: a standard liability policy specifically excludes alcohol claims. In 2026, a typical Florida full-service restaurant pays $6,000–$15,000 per year for the full stack, with liquor liability alone running $400–$2,500+ depending on how much of your revenue comes from alcohol, your operating hours, and whether you offer live entertainment.

Why "Restaurant Insurance" Is Really Six Policies Working Together

Most owners buy what an online quote engine calls a "BOP" — a Business Owners Policy, which packages general liability and commercial property into one bundle — and assume they are covered. A BOP is a fine foundation, but for a Florida restaurant that serves alcohol it is roughly half of what you need. The losses that actually close restaurants — an over-service lawsuit, a hurricane that takes out two weeks of revenue, a walk-in cooler full of spoiled product, a kitchen burn, a wage-and-hour claim — sit in coverages the basic package either excludes or leaves underfunded.

A correctly built Florida restaurant program coordinates six lines so the gaps between them are closed: general liability, liquor liability, commercial property, business interruption, workers' compensation, and food spoilage (with commercial auto, employment practices, and cyber added based on your operation). The reason this matters is that each policy points at the others. The single most expensive gap is the one between your general liability policy and the alcohol you serve.

The Liquor Liability Gap: The Coverage Your GL Policy Quietly Excludes

Open any standard commercial general liability policy and you will find a section called the liquor liability exclusion. It removes coverage for any business that is "in the business of" manufacturing, distributing, selling, serving, or furnishing alcoholic beverages. The moment your restaurant pours a glass of wine for money, that exclusion applies to you. If a patron is over-served, drives, and injures someone, and the injured party sues your restaurant, your GL carrier will read the exclusion and deny the claim outright — including the cost to defend it.

That denial is not a technicality. Defense costs alone on a single alcohol-related suit routinely exceed $50,000 before a dollar of any settlement. The only thing that responds is a separate liquor liability policy (sometimes called dram shop coverage) or a liquor liability endorsement added to your package. For a restaurant where alcohol is a modest share of sales, this is one of the least expensive coverages you will buy — and the one most likely to be missing.

Florida's Dram Shop Law: Friendly, Not a Force Field (§ 768.125)

"Dram shop" is an old term for a tavern — bars once sold gin by the "dram." Dram shop liability is the legal theory that holds the seller of alcohol responsible for harm caused by an intoxicated customer. Florida's version, Florida Statute § 768.125, is deliberately narrow. It says a person who sells or furnishes alcohol to someone of lawful drinking age does not become liable for injury or damage resulting from that person's intoxication — except in two situations:

- Willfully and unlawfully serving someone who is not of lawful drinking age (an underage patron), and

- Knowingly serving a person who is habitually addicted to alcohol.

This makes Florida one of the most vendor-friendly states in the country. In many states you can be sued simply for serving a visibly intoxicated adult; in Florida, that alone is generally not enough. But owners read this statute and reach the wrong conclusion. The two exceptions are exactly the exposures a busy restaurant faces. Underage service is a constant risk in a state full of college towns and tourist nightlife — Gainesville, Tallahassee, Daytona Beach, Miami Beach — where fake IDs are routine and a single slip by a new server creates liability. And "knowingly serving a habitually addicted" patron is a fact question a plaintiff's attorney will happily put in front of a jury. Most importantly, § 768.125 sets the standard for losing a case; it does nothing to stop you from being sued. Liquor liability insurance pays to defend you even when the law is ultimately on your side.

The Assault and Battery Sublimit Most Owners Never Read

If your restaurant has a bar scene, late-night hours, or live entertainment, there is a second clause that decides claims: the assault and battery (A&B) provision. A&B losses are fights, bouncer injuries, parking-lot altercations, and similar physical confrontations on your premises. Many liquor and liability policies now apply a sublimit to A&B — a cap that is lower than your overall policy limit. It is common in 2026 to see a $1 million liquor policy that quietly caps A&B at $250,000 or $500,000, and high-energy venues may find A&B excluded entirely. If a brawl injures a patron and the judgment exceeds your A&B sublimit, the difference comes out of your business. Knowing your sublimit — and negotiating it up where the carrier allows — is exactly the kind of detail a generalist quote engine will never surface.

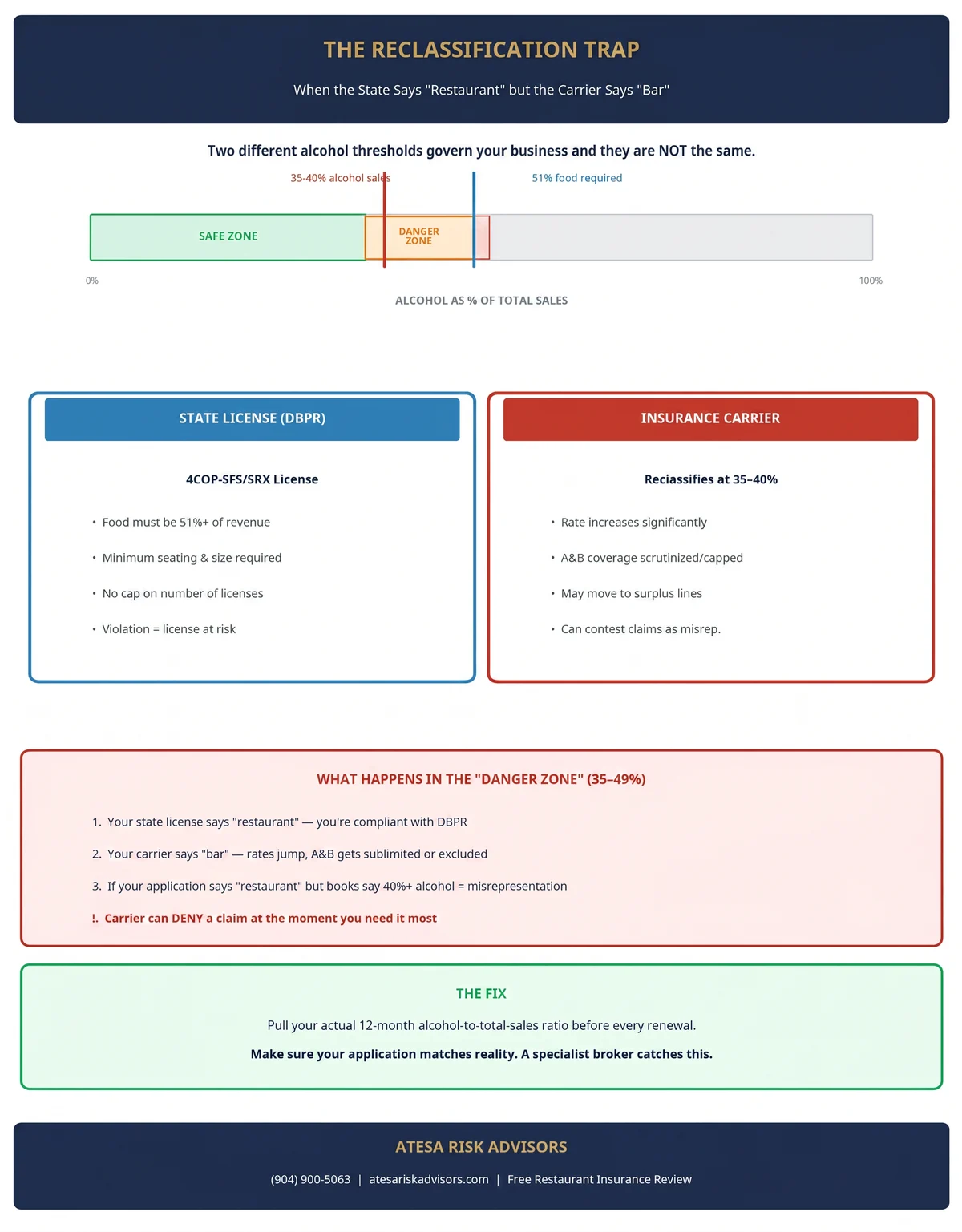

The Reclassification Trap: When the State Says "Restaurant" but the Carrier Says "Bar"

Florida restaurant owners get tripped up by two different alcohol thresholds that sound similar and are not.

The regulatory threshold governs your liquor license. The most common full-liquor restaurant license, the 4COP-SFS/SRX special restaurant license issued by the Division of Alcoholic Beverages and Tobacco (ABT) within the Department of Business and Professional Regulation (DBPR), requires that you operate as a bona fide food-service establishment, meet minimum size and seating requirements under Florida Statute § 561.20, and derive at least 51% of gross revenue from food and non-alcoholic beverages. Unlike a quota license — the limited, population-based licenses that trade for six figures on the open market — there is no statewide cap on the number of SFS/SRX restaurant licenses.

The underwriting threshold is entirely separate and lower. Insurance carriers re-rate a venue from "restaurant" to "bar" or "tavern" when alcohol receipts pass roughly 35–40% of total sales. Cross that line and three things happen: your rate rises, your A&B coverage gets scrutinized or sublimited, and you may be moved into the surplus lines market — non-admitted carriers that write higher-hazard risks but are not backed by the Florida Insurance Guaranty Association (FIGA) and carry a 5% state surplus lines tax.

Here is where restaurants get hurt. A successful happy hour, a craft-cocktail program, or a brewpub concept can easily drift above 40% alcohol without the owner re-checking the math. If your insurance application says "restaurant" and your books say "bar," a carrier can allege misrepresentation and contest a claim at exactly the moment you need it paid. The fix is unglamorous: pull your actual 12-month alcohol-to-total-sales ratio before every renewal and make sure your application matches reality.

The Coverages in a Florida Restaurant Bundle — and What Each Pays

- General liability — Slip-and-falls, a guest who alleges foodborne illness, property damage to others. This is your premises-and-operations baseline; Florida restaurants average roughly $1,900/year for GL alone. See our guide to general liability insurance costs in Florida.

- Liquor liability — The alcohol carve-out described above. Typically $400–$2,500+ depending on alcohol ratio and hours.

- Commercial property — Your building (if owned), kitchen equipment, furniture, and inventory. Coastal restaurants commonly pay $3,000–$8,500/year because of hurricane exposure.

- Business interruption — Replaces lost income and pays continuing expenses (rent, payroll, loan payments) while you are closed for a covered loss. The key setting is the period of restoration — how long the policy will keep paying.

- Food spoilage and equipment breakdown — Pays for inventory lost when a power outage or a failed walk-in cooler or compressor spoils product. Usually a few hundred dollars a year as an endorsement, and one of the highest-value add-ons in Florida.

- Workers' compensation — Required in Florida for most non-construction employers with four or more employees under Florida Statute § 440. Kitchens produce burns, cuts, slips, and grease fires; comp covers the medical bills and lost wages. Compare current Florida workers' comp rates.

Depending on your operation, a complete program also adds commercial auto (catering, delivery, and hired/non-owned auto for staff running errands), employment practices liability (EPLI) — wage-and-hour, tip-credit, and harassment claims are among the most frequent and expensive losses in hospitality — and cyber coverage for point-of-sale data breaches.

What a Florida Restaurant Bundle Costs in 2026

For a typical Florida full-service restaurant, expect the combined program to land in the $6,000–$15,000 per year range, and higher on the coast or with a heavy bar component. The major pieces in 2026:

- General liability: roughly $800–$2,800/year

- Liquor liability: roughly $400–$2,500+/year (driven by alcohol ratio and hours)

- Commercial property: $3,000–$8,500/year on the coast

- Business interruption: often $600–$2,000/year as part of the package

- Food spoilage: a few hundred dollars/year

- Workers' compensation: varies with payroll and class code

The biggest cost drivers are location (a Jacksonville Beach or Key West restaurant pays far more than one in Lake City or Ocala), your alcohol-to-food ratio, operating hours and live entertainment, prior claims, square footage, and whether you have a commercial fryer and hood system (a major fire variable). For the broader market backdrop, see our overview of Florida commercial insurance rates in 2026.

The Hurricane Layer Florida Restaurants Underestimate

For a Florida restaurant, the storm rarely flattens the building — yet it still produces the worst year of your business life through three mechanisms most owners overlook.

First, the percentage wind deductible. Coastal property policies replace a flat dollar deductible with a windstorm or named-storm deductible of 2–5% of the insured building value. On a building insured for $1 million, a 3% wind deductible is $30,000 out of your pocket before the policy pays a cent. Knowing that number in dollars — not just as a percentage buried on the declarations page — is essential to your hurricane cash plan. Our commercial hurricane deductible breakdown explains how buy-back options work.

Second, flood is not in your property policy. Wind and flood are separate perils in Florida. Flood coverage comes through the National Flood Insurance Program (NFIP) or a private flood carrier and commonly costs a Florida restaurant $1,000–$5,000+/year depending on flood zone. A storm surge that ruins your dining room is a flood loss, and without a flood policy it is uninsured.

Third — and most damaging — business interruption. Two to four weeks closed after a storm, an evacuation order, or a prolonged power outage can erase a quarter's profit. Make sure your period of restoration is realistic (post-storm rebuilds and permit backlogs in Florida run long), that extra expense coverage will fund a temporary kitchen or generator, and that civil authority coverage responds when officials close your area even if your building is untouched. Pair it with spoilage coverage so the inventory you lose to a dark walk-in cooler is reimbursed.

How to Build a Florida Restaurant Insurance Bundle

- Calculate your true alcohol-to-total-sales ratio from the last 12 months of POS data, so you know whether carriers will rate you as a restaurant or a bar.

- Confirm your liquor license type (4COP-SFS/SRX, 2COP beer and wine, or a quota license) and the food-revenue requirement that comes with it.

- Quote GL and liquor liability together and read the assault-and-battery sublimit — negotiate it up if you have late-night or entertainment exposure.

- Right-size property limits to replacement cost and add equipment breakdown and food spoilage endorsements.

- Set a realistic business-interruption period of restoration, with extra expense and civil authority coverage included.

- Add flood coverage and confirm your wind deductible in dollars, not just as a percentage.

- Verify workers' comp class codes and add EPLI and cyber based on your staffing and POS setup.

- Have a specialist broker package the program — coordinated bundling can unlock 10–20% in savings and, more importantly, prevent the classification and limit mistakes that cause claim denials.

Sources

[1] Florida Statute § 768.125 — Liability for Injury or Damage Resulting from Intoxication

[2] Florida Statute § 561.20 — Limitation on Number of Licenses (Quota and Special Restaurant Licenses)

[3] Florida DBPR — Division of Alcoholic Beverages and Tobacco (ABT) License Types

[4] Florida Statute § 440 — Workers' Compensation

[5] Insurance Information Institute — Business Interruption Insurance

[6] Insurance Information Institute — Business Insurance Basics

[7] National Restaurant Association — Operations and Risk Resources

[8] Insurance Journal — Restaurants and Bars: Liquor Sales, Risk Transfer and Other Trends (March 2026)

[9] FEMA — National Flood Insurance Program (NFIP)

[10] Florida Office of Insurance Regulation — Surplus Lines and Property Market Data

Frequently Asked Questions

Does general liability insurance cover liquor-related claims in Florida?

No. Every standard commercial general liability policy contains a liquor liability exclusion that applies to any business in the business of selling, serving, or furnishing alcohol. If a customer or a third party sues over an alcohol-related injury, your GL carrier will deny the claim — including defense costs. You need a separate liquor liability policy or endorsement for that exposure to be covered.

Is liquor liability insurance required by law in Florida?

Florida does not impose a blanket statutory requirement that every alcohol seller carry liquor liability insurance, but it is effectively mandatory in practice. Most commercial leases, franchise agreements, and SBA or commercial lenders require it as a condition of the lease or loan, and operating without it leaves alcohol claims entirely uninsured.

How much does liquor liability insurance cost for a Florida restaurant?

For a restaurant where alcohol is a modest share of sales, liquor liability commonly runs from a few hundred dollars to about $2,500 per year. Bars, nightclubs, and venues with late-night hours or live entertainment pay substantially more because of higher over-service and assault-and-battery exposure.

What is Florida's dram shop law?

Florida's dram shop law, Statute § 768.125, generally protects a vendor from liability for serving a lawful-age adult, with two exceptions: willfully and unlawfully serving an underage person, and knowingly serving someone habitually addicted to alcohol. It is one of the most vendor-friendly dram shop laws in the country, but it still allows lawsuits in those two situations and does not prevent you from being sued and having to defend.

At what point does my restaurant get classified as a bar for insurance?

Most carriers reclassify a venue from restaurant to bar or tavern when alcohol receipts exceed roughly 35–40% of total sales. This is different from — and lower than — the 51% food-revenue requirement attached to Florida's 4COP-SFS/SRX special restaurant license. If your books cross the carrier's threshold but your application still says "restaurant," the carrier can allege misrepresentation and contest a claim.

What is an assault and battery exclusion or sublimit?

Assault and battery (A&B) coverage responds to fights and physical altercations on your premises. Many liquor and liability policies now cap A&B at a sublimit — often $250,000 to $500,000 even on a $1 million policy — or exclude it entirely for higher-risk venues. If a judgment exceeds the sublimit, your business pays the difference, so reviewing and negotiating this figure is important for any venue with a bar scene.

Does my restaurant need business interruption insurance for hurricanes?

Yes. For most Florida restaurants, the largest storm loss is not building damage but lost income during a closure caused by a hurricane, evacuation order, or extended power outage. Business interruption coverage replaces lost revenue and continuing expenses; make sure the period of restoration is realistic and that extra expense and civil authority coverage are included.

What is food spoilage coverage and do I need it?

Food spoilage coverage reimburses inventory lost when a power outage or refrigeration breakdown spoils product. It is usually added as an endorsement for a few hundred dollars a year and is one of the highest-value additions for a Florida restaurant, where hurricane-related outages are common and a single dark walk-in cooler can destroy thousands of dollars of inventory.

Do I still need liquor liability if I have a 4COP-SFS/SRX license?

Yes. A liquor license is government permission to sell alcohol; it provides no insurance whatsoever. Your license confirms you are allowed to serve, but only a liquor liability policy pays to defend and settle alcohol-related claims. The two are unrelated, and many lenders and landlords require the insurance regardless of license type.

Does my commercial lease or franchise require liquor liability coverage?

Frequently, yes. Many restaurant leases require tenants to carry liquor liability and name the landlord as an additional insured, and franchise agreements almost universally mandate it. Some SBA and commercial lenders also require liquor liability as a condition of financing, so review your lease and loan documents before you assume the coverage is optional.

What is the difference between host liquor liability and liquor liability?

Host liquor liability covers a business that occasionally serves alcohol but is not in the business of selling it — for example, an office that hosts a holiday party. A restaurant that sells alcohol for profit needs full liquor liability, because the host liquor coverage built into some general liability policies does not apply once you are "in the business" of serving alcohol.

Are surplus lines liquor policies safe, and are they backed by FIGA?

Surplus lines (non-admitted) carriers legally write higher-hazard restaurant and bar risks that standard admitted carriers decline, and many are financially strong. However, surplus lines policies are not backed by the Florida Insurance Guaranty Association (FIGA) and carry a 5% state surplus lines tax. A specialist broker should confirm the carrier's financial rating and disclose the tax before you bind.

Related Reading

- Restaurant Insurance 101 for Florida (2026): Every Coverage You Need and the Claims That Trigger Them — the full coverage stack beyond liquor liability, and the claims that trigger each policy.