Restaurant Insurance 101 for Florida (2026): Every Coverage You Need and the Claims That Trigger Them

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 25, 2026

Key Takeaways

- A Florida restaurant's core insurance stack is six policies — general liability, commercial property, workers' compensation, liquor liability, commercial auto, and a commercial umbrella — and most owners bundle the first two into a single Business Owner's Policy (BOP).

- Workers' compensation is required by law once a restaurant has four or more employees, full- or part-time (Fla. Stat. 440.02) [4].

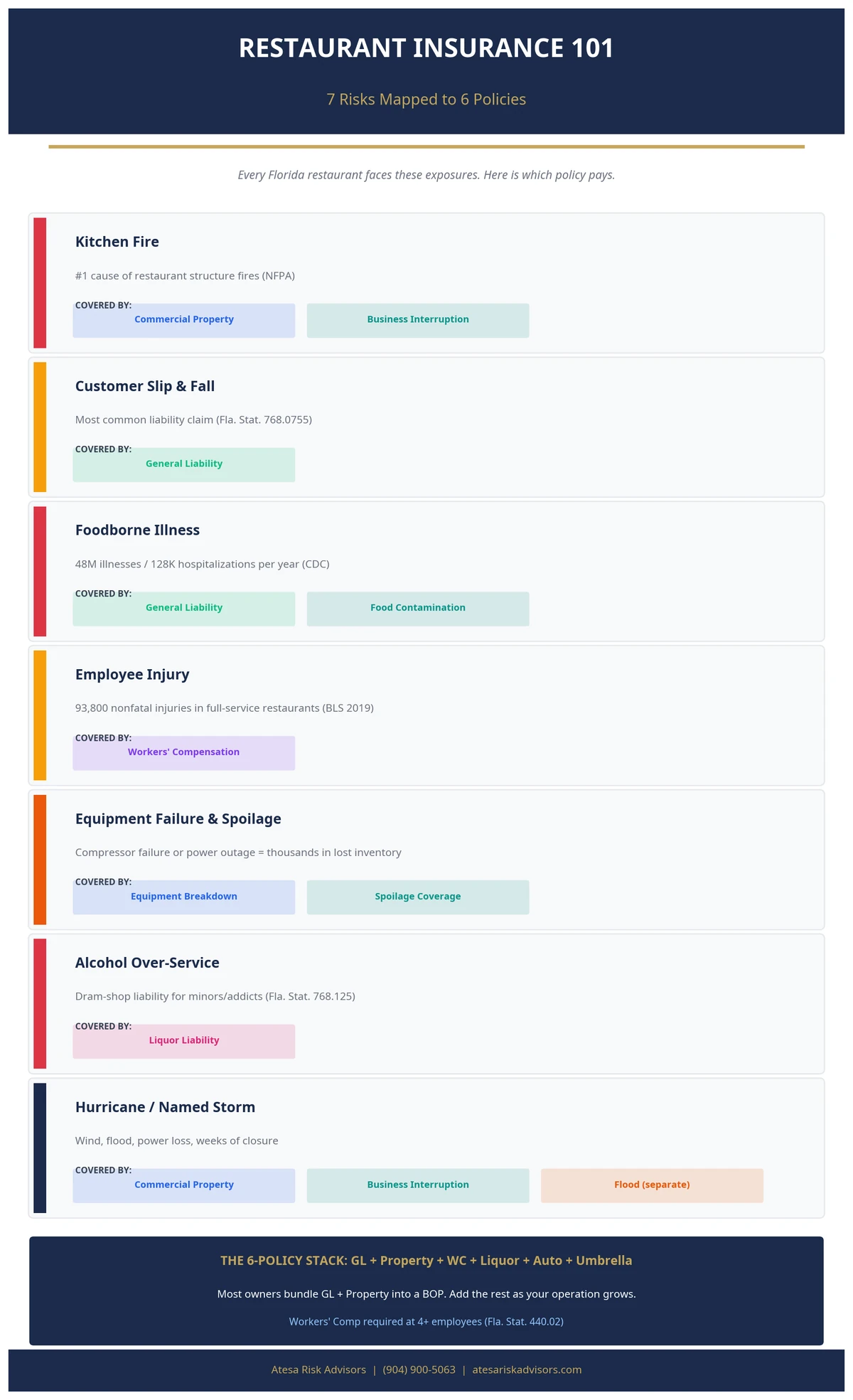

- Cooking equipment is the leading cause of restaurant structure fires [1], and the CDC estimates 48 million foodborne illnesses, 128,000 hospitalizations, and 3,000 deaths in the U.S. each year [2] — two exposures every restaurant policy has to cover.

- Florida's 2023 lawsuit-reform law (HB 837) shortened the deadline to sue for a customer injury from four years to two years, and now bars anyone found more than 50% at fault from recovering anything (Fla. Stat. 768.81, 95.11) [5].

- Under Florida's dram-shop law (Fla. Stat. 768.125), a restaurant generally is not liable for serving a sober adult of legal age, but is exposed for serving a minor or someone known to be habitually addicted to alcohol [6].

Every Florida restaurant should carry the same core stack: general liability for customer injuries and foodborne-illness claims, commercial property for the building and kitchen equipment, workers' compensation (required by law at four or more employees), liquor liability if you serve alcohol, commercial auto for delivery and catering, and a commercial umbrella for the large claims. Most independent restaurants combine general liability and property into one Business Owner's Policy — a BOP — and add the rest as their payroll, bar program, and delivery operation grow.

Restaurants are one of the harder small businesses to insure. You run open flame and hot oil a few feet from paying customers. The floor is wet for most of a shift. The food you serve can make someone sick. Your staff is often young, busy, and new. And in Florida, one storm can close your dining room for weeks. Each of those is a different kind of claim, and each is answered by a different policy.

Here is every coverage a Florida restaurant should think about, what each one pays for in plain English, and the claims that set them off most often. Where Florida law changes how a claim plays out, it is cited by statute number so you can check it yourself.

The Coverages Every Florida Restaurant Should Carry

1. General liability (GL). This is the foundation. It pays when a customer is injured or their property is damaged in connection with your business — the classic example is a guest who slips on a wet floor, but it also covers a server who spills hot coffee on someone or a claim that a meal caused food poisoning. In Florida, a customer slip-and-fall is governed by Fla. Stat. 768.0755: the injured person has to prove your restaurant knew, or should have known, about the dangerous condition and did not fix it [3]. GL funds your defense and any settlement.

2. Commercial property. This covers your physical assets: the building if you own it, your build-out and fixtures if you lease, plus kitchen equipment, furniture, signage, and inventory. The Florida wrinkle is wind — most property policies here carry a separate, percentage-based hurricane deductible, so read that number before you sign.

3. Business Owner's Policy (BOP). A BOP bundles general liability and commercial property into one policy, usually for less than buying them separately. For most independent and small-chain restaurants this is the starting point, and the other coverages bolt on around it.

4. Workers' compensation. This pays the medical bills and replaces lost wages when an employee is hurt on the job — and restaurant work produces a lot of those: grease burns, knife cuts, slips on a wet line, and back strains from lifting. In Florida, a non-construction business like a restaurant must carry workers' comp once it has four or more employees, full- or part-time (Fla. Stat. 440.02) [4].

5. Liquor liability. If you serve alcohol, your general liability policy will not cover an alcohol-related claim — you need separate liquor liability coverage. Florida's dram-shop law (Fla. Stat. 768.125) actually limits a vendor's exposure: you generally are not liable for serving a sober adult of legal age who later causes harm, but you can be liable for serving a minor, or for knowingly serving someone habitually addicted to alcohol [6]. The liquor-liability guide linked below covers this in depth.

6. Commercial auto and hired/non-owned auto. If your restaurant owns any vehicle — a delivery car, a catering van — it needs a commercial auto policy; a personal policy will deny a business-use claim. If your employees run deliveries in their own cars, you also want hired and non-owned auto coverage, which protects the business when a worker crashes a vehicle you do not own while on the job.

7. Equipment breakdown. Property insurance pays when a fire or storm damages your walk-in cooler; it does not pay when the cooler's compressor simply dies. Equipment breakdown covers that mechanical and electrical failure — refrigeration, HVAC, ovens, and fryers — which on a commercial kitchen line is a frequent and expensive event.

8. Food spoilage and contamination. When refrigerated or frozen inventory is lost — to a power outage, a failed cooler, or contamination — this coverage pays to replace it and clean up. In Florida, where a hurricane can knock out power for days, spoilage coverage matters more than almost anywhere else.

9. Business interruption. If a covered loss like a kitchen fire or hurricane forces you to close, business interruption replaces the income you would have earned while you rebuild and keeps covering payroll and rent. For a Florida restaurant, this is often the difference between reopening and not.

10. Employment practices liability (EPLI). Restaurants have high headcount and high turnover, which makes them a common target for wage-and-hour, harassment, and wrongful-termination claims. EPLI covers your defense and damages for those employee suits, which a general liability policy excludes.

11. Cyber liability. Your point-of-sale system and online-ordering platform hold customer card data, and a breach there triggers notification costs, fines, and lawsuits. Cyber coverage handles the response. The Florida small-business cyber guide below goes deeper.

12. Commercial crime / employee dishonesty. Restaurants handle cash and move inventory constantly, which makes internal theft a real and recurring loss. Crime coverage reimburses you for employee theft of money or property.

What Each Coverage Pays For

| Coverage | What it pays for | Typically needed by |

|---|---|---|

| General liability | Customer injuries, foodborne-illness claims, property damage | Every restaurant |

| Commercial property | Building, build-out, equipment, inventory | Every restaurant |

| Workers' compensation | Employee injuries — medical and lost wages | Required at 4+ employees |

| Liquor liability | Alcohol-related injury claims | Anyone serving alcohol |

| Commercial / non-owned auto | Crashes involving business or delivery driving | Delivery, catering, any owned vehicle |

| Equipment breakdown | Mechanical / electrical failure of kitchen equipment | Every restaurant |

| Food spoilage | Inventory lost to outage or equipment failure | Every restaurant (critical in FL) |

| Business interruption | Lost income while closed for a covered loss | Every restaurant |

| EPLI | Employee lawsuits (wage, harassment, termination) | Most restaurants |

| Cyber liability | POS / data-breach response and liability | Any card-accepting restaurant |

The Most Common Restaurant Claims in Florida

Kitchen fires. Cooking equipment is the leading cause of restaurant structure fires — it is involved in more of them than any other source [1]. Grease, fryers, and ranges are the usual culprits, and a single fire can hit your property, your income (business interruption), and your equipment all at once.

Customer slip-and-fall injuries. A wet floor near the kitchen door or a spill in the dining room is the most routine liability claim a restaurant faces. Florida law (Fla. Stat. 768.0755) requires the customer to prove you knew or should have known about the hazard [3] — but defending even a weak claim costs money, which is what your general liability policy is for.

Foodborne illness. The CDC estimates 48 million foodborne illnesses, 128,000 hospitalizations, and 3,000 deaths in the U.S. every year [2]. A single outbreak traced to your kitchen can produce multiple injury claims plus the cost of a temporary closure — both general liability and food-contamination coverage come into play.

Employee injuries. Restaurant work is physical and hot. Full-service restaurants alone reported roughly 93,800 nonfatal employee injuries and illnesses in 2019, led by burns, cuts, slips, and strains [7]. These are workers' compensation claims, which is why the law makes the coverage mandatory at four employees.

Equipment failure and spoilage. A compressor that quits on a Friday night, or a multi-day power outage after a storm, can spoil thousands of dollars of inventory and stop service. Equipment breakdown and spoilage coverage absorb the loss; a basic property policy alone usually will not.

Liquor-related incidents. If you serve alcohol, an over-service claim is a real exposure — limited but real under Florida's dram-shop statute (Fla. Stat. 768.125), especially anything involving a minor [6].

Which Coverages by Restaurant Type

| Coverage | Coffee shop / QSR (no alcohol) | Full-service with bar | Delivery / ghost kitchen |

|---|---|---|---|

| BOP (GL + property) | Yes | Yes | Yes |

| Workers' comp (4+ staff) | Yes | Yes | Yes |

| Liquor liability | No | Yes | If alcohol sold |

| Commercial / non-owned auto | If delivery | If catering / delivery | Yes — core |

| Equipment breakdown + spoilage | Yes | Yes | Yes |

| Business interruption | Yes | Yes | Yes |

| Cyber liability | Yes | Yes | Yes |

The most common mistake I see is an owner who buys a general liability policy and assumes it covers the whole restaurant. It does not touch a workers' comp injury, an alcohol claim, a blown compressor, or the income you lose while you are closed after a storm. By the time someone finds the gap, there is usually already a claim sitting in it. A restaurant runs on a stack of coverages, and the value is in making that stack fit how you actually operate.

— Ricardo Alonso, Founder, Atesa Risk Advisors

Florida-Specific Considerations

Workers' comp at four employees. Florida requires a non-construction business to carry workers' compensation once it employs four or more people, full- or part-time (Fla. Stat. 440.02) [4]. Corporate officers and LLC members generally count toward that total. Operating uninsured past four employees exposes you to state stop-work orders and penalties.

The dram-shop limit on liquor claims. Florida is more protective of alcohol vendors than many states. Under Fla. Stat. 768.125, serving a sober adult of legal age who later causes harm generally does not make you liable — but willfully serving a minor, or knowingly serving someone habitually addicted to alcohol, can [6]. That narrow exposure is exactly what liquor liability coverage is priced for.

The 2023 lawsuit reforms (HB 837). Two changes from Florida's 2023 tort-reform law affect every restaurant injury claim. First, the deadline for a customer to file a general negligence suit dropped from four years to two (Fla. Stat. 95.11). Second, Florida switched to modified comparative negligence: a person found more than 50% at fault for their own injury now recovers nothing (Fla. Stat. 768.81) [5]. Both tend to help the defense in a slip-and-fall, but neither removes your need to carry and defend the coverage.

Hurricane season. Wind, flooding, and power loss make Florida property and income coverage different from the rest of the country. Confirm your hurricane deductible, make sure business interruption and food-spoilage coverage are in place before June 1, and remember that flood is a separate policy — standard commercial property does not cover rising water.

Your Restaurant Coverage Checklist

| Step | Action |

|---|---|

| 1. Map your exposures | List what you own, who you employ, whether you serve alcohol, and how food leaves the building. |

| 2. Start with a BOP | Combine general liability and commercial property as your base policy. |

| 3. Add workers' comp before hire #4 | Florida requires it at four employees; put it in place before you cross the line. |

| 4. Layer liquor liability | If you serve alcohol, add a dedicated liquor-liability policy. |

| 5. Cover vehicles and delivery | Add commercial auto for owned vehicles and hired/non-owned auto for staff deliveries. |

| 6. Protect the kitchen | Add equipment breakdown and food-spoilage coverage for refrigeration and outages. |

| 7. Cap it and review yearly | Add a commercial umbrella for large claims, and re-check limits every renewal. |

FAQ for Florida Restaurant Owners

Q: What insurance does a restaurant need in Florida?

A: At minimum, general liability and commercial property (usually bundled as a Business Owner's Policy), plus workers' compensation once you have four employees. If you serve alcohol you add liquor liability; if you deliver or cater you add commercial and hired/non-owned auto; and most restaurants also carry equipment breakdown, food spoilage, business interruption, and a commercial umbrella.

Q: Is workers' compensation required for a restaurant in Florida?

A: Yes, once you have four or more employees, full- or part-time (Fla. Stat. 440.02). Corporate officers and LLC members generally count toward the four. Below four employees it is optional, but still worth carrying, because an employee injury otherwise comes straight out of the business.

Q: Does restaurant general liability cover a customer who slips and falls?

A: Yes — slip-and-fall is one of the most common general liability claims a restaurant sees. Under Florida law (Fla. Stat. 768.0755), the customer must prove you knew or should have known about the hazard, but your policy covers the defense and any settlement regardless.

Q: Is my restaurant liable if a customer gets drunk and causes a crash?

A: Usually not, if the customer was a sober adult of legal age when served — Florida's dram-shop law (Fla. Stat. 768.125) limits that exposure. You can be liable for serving a minor or someone known to be habitually addicted, which is exactly what liquor liability coverage protects against.

Q: Does restaurant insurance cover food spoilage from a power outage?

A: Not under a basic property policy by itself. You need food-spoilage (and often equipment-breakdown) coverage, which pays to replace refrigerated and frozen inventory lost to an outage or a cooler failure. In hurricane-prone Florida, this is one of the most useful add-ons a restaurant can carry.

Q: Does business insurance cover hurricane damage to my restaurant?

A: Commercial property covers hurricane wind damage, usually subject to a separate percentage-based hurricane deductible, and business interruption replaces lost income while you are closed. Flooding is not covered by standard property insurance — that requires a separate flood policy.

Q: What is the difference between a BOP and general liability?

A: General liability covers only injuries and damage to other people. A Business Owner's Policy (BOP) bundles that general liability together with commercial property — your building, equipment, and inventory — usually at a lower combined price. Most restaurants start with a BOP and build from there.

Q: How much does restaurant insurance cost in Florida?

A: It depends on your size, your sales, your payroll, whether you serve alcohol, and your location's storm exposure, so the only accurate number is a quoted one. The base BOP is the largest single piece for most restaurants, with workers' comp scaling to payroll and liquor liability scaling to alcohol sales.

Related Reading

- Florida Restaurant Insurance 2026: The Liquor Liability Gap That Can Close Your Doors — the deep dive on dram-shop law and liquor coverage.

- How Much Does General Liability Insurance Cost in Florida? (2026 Rates) — what the foundation coverage actually runs.

- Florida Workers' Comp Rates in 2026: What Employers Need to Know — how the required coverage is priced.

- Florida Small Business Cyber Insurance 2026 — protecting your POS and customer data.

How Atesa Risk Advisors Can Help

We place the whole restaurant stack — not just one policy — and build it around how your restaurant actually runs: your menu, your bar program, your delivery setup, your payroll, and your storm exposure. As an independent, RamseyTrusted Florida brokerage, we shop your coverage across multiple carriers instead of selling one company's product, and we read the fine print that decides claims: your hurricane deductible, your liquor exclusions, and whether your spoilage and business-interruption limits would actually carry you through a closure.

When a claim comes — a fire, a fall, a storm, an injured line cook — the difference between a smooth recovery and a fight usually traces back to a decision made at the quoting stage. We make those decisions with you, before anything goes wrong, and review the whole stack every renewal as your restaurant changes.

Opening, expanding, or just not sure your restaurant is fully covered? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] NFPA — Structure Fires in Eating and Drinking Establishments

[4] Fla. Stat. 440.02 — Workers' compensation definitions (the four-or-more-employee threshold)

[8] Insurance Information Institute — Insurance for food service businesses

External Resources for Florida restaurant owners:

- Florida Division of Workers' Compensation — coverage requirements

- Florida Department of Business & Professional Regulation — Hotels & Restaurants

*Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University and a background in construction and small business. He helps Florida restaurant owners build coverage that fits how their kitchen actually runs.