The June 1st Countdown: Is Your Jacksonville Business Sitting on a $250,000 Liability?

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 13, 2026

Key Takeaways

- Duval and St. Johns County commercial hurricane deductibles in 2026 typically run 3 percent to 5 percent of total insured value (TIV) — meaning a $5M building carries a $150,000 to $250,000 out-of-pocket liability per named-storm event [1][2].

- A Deductible Buyback (also called a "buy-down") is a wrap-around policy that pays the difference between your primary policy''s high named-storm deductible and a flat retention you can actually budget for — typically $5,000 to $10,000 [3].

- Buyback premium typically runs 1.5 percent to 3 percent of the bought-down amount — roughly $8,500 to $15,000 per year to convert a $250,000 exposure into a $10,000 exposure [1].

- Florida commercial mortgage lenders (Ameris Bank, TIAA / EverBank, Synovus, regional credit unions) increasingly require a deductible cap as a loan covenant — a buyback is the fastest path to compliance without changing primary carriers [4].

- 17 new admitted-market carriers have entered Florida commercial property since HB 837 passed in March 2023, and several offer buyback capacity specifically targeting Duval and northern St. Johns owners — capacity is open in May 2026 but tightens sharply as June 1 approaches [5][6].

With Atlantic hurricane season starting June 1, 2026, the most cost-effective storm-prep move for most Duval and northern St. Johns commercial property owners is not a generator or new shutters — it''s a deductible buyback policy that converts a six-figure named-storm exposure into a flat $5,000 to $10,000 retention for $8,500 to $15,000 per year. Today is May 13, 2026. You have 18 days. Buyback carriers stop binding new business 7 to 14 days before season start, so your real deadline is closer to May 25.

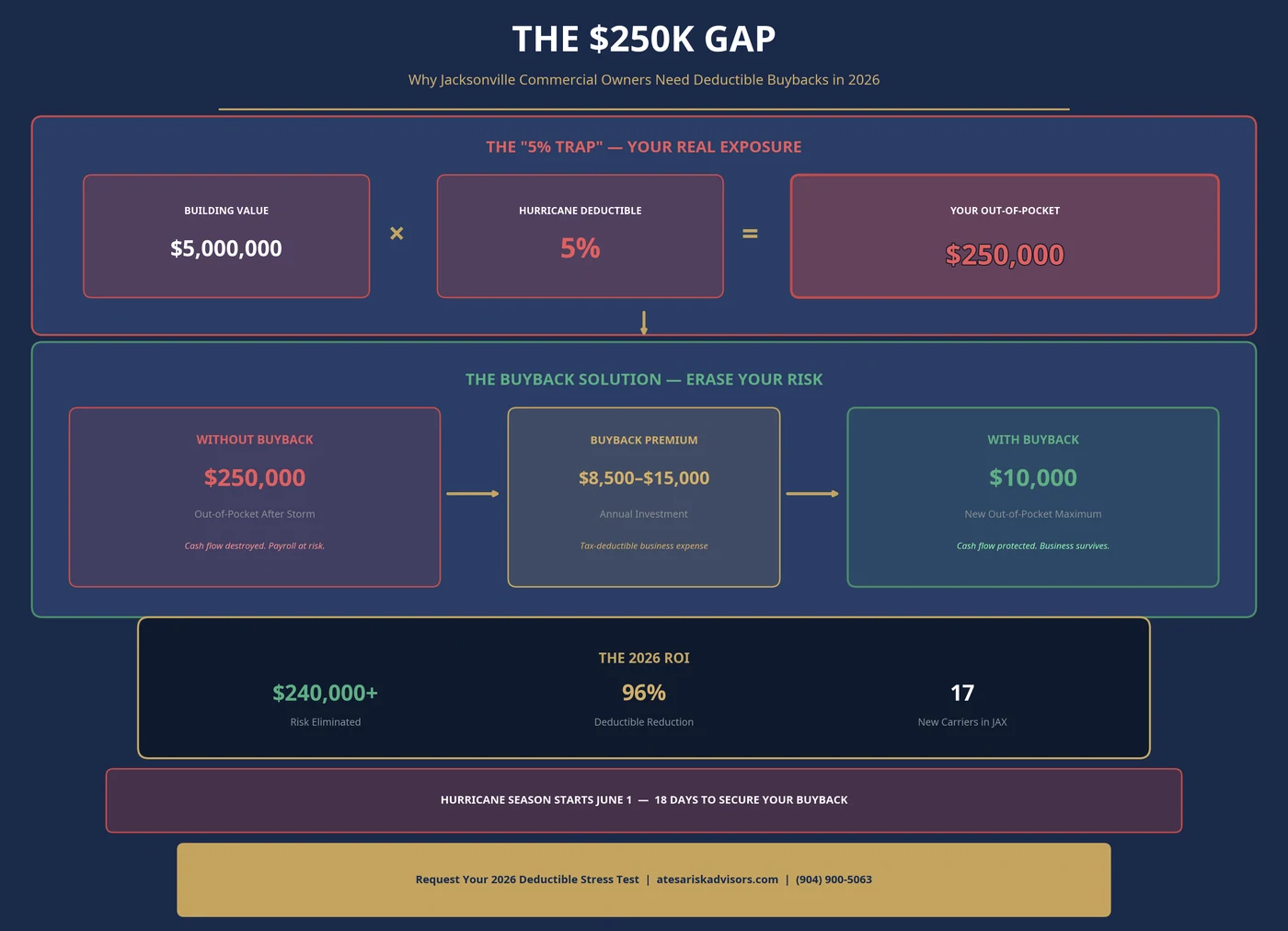

If you are the CFO, asset manager, or owner of a commercial building in Downtown Jacksonville, San Marco, Riverside, the Southside / Town Center, or the JAXPORT-adjacent industrial corridor, you are almost certainly carrying a six-figure named-storm deductible on your primary commercial property policy. Most owners we audit in 2026 do not realize this — they read "5% deductible" on their dec page and mentally treat it as a $5,000 number instead of 5 percent of total insured value. On a $5M building, that math gap is $245,000 of unbudgeted balance-sheet risk per storm.

The good news: the 2026 commercial property market is the healthiest it has been since pre-Ian. Seventeen new admitted-market carriers have re-entered Florida since HB 837 tort reform, and several are specifically writing buyback capacity for Jacksonville office, retail, and warehouse accounts in the $1M to $25M TIV range. The bad news: carriers tighten capacity dramatically in the final two weeks before June 1, and once a named storm is forecast for the Atlantic basin, binding stops cold. The window to act is now.

This guide walks through the math, the buyback policy mechanics, the lender-covenant angle, and the 18-day countdown calendar. The downloadable CFO Deductible Stress Test Worksheet at the bottom is the printable version you can walk through with your broker on a single call.

Why "standard" hurricane deductibles are failing Duval business owners in 2026

Between 2022 and 2024, Florida commercial property carriers moved almost exclusively to percentage-based "Named Storm" deductibles on new and renewing business. The old flat-dollar hurricane deductible — $25,000 or $50,000 regardless of building value — effectively disappeared from the admitted market. The replacement: a percentage of TIV (Total Insured Value, the dollar amount your building is insured for).

The math is brutal once you see it.

`` Out-of-Pocket Exposure = Total Insured Value (TIV) × Named-Storm Deductible % ``

A representative 2026 Duval commercial dec page reads something like:

- Total Insured Value: $5,000,000

- All-Other-Perils (AOP) deductible: $10,000 (flat — the "everyday" deductible for fire, theft, vandalism)

- Named Storm deductible: 5% of TIV

When you do the math, the Named Storm deductible is $250,000, not a number that fits comfortably in any CFO''s quarterly budget.

Two often-missed details that make this worse:

- It is per-event, not annual. If two named storms hit Duval in the same season (which has happened more than once in the last decade), you pay the full deductible twice. Three storms in one season = three deductibles. There is no annual aggregate cap on most Florida commercial policies.

- It is per-occurrence, not per-claim. A single named storm causes wind damage, water damage, and business interruption losses. All three are typically subject to one deductible — but the way the deductible is calculated against TIV (not against the loss) means a $40,000 covered loss on a $5M building still hits the full $250,000 deductible. You receive nothing on a loss smaller than the deductible.

AOP vs Named Storm — two different deductibles on the same policy

The All-Other-Perils (AOP) deductible is the flat-dollar deductible that applies to non-storm losses — fires, burglary, water damage, vandalism. It''s typically $5,000, $10,000, or $25,000. Most CFOs see this number on the dec page and mentally apply it to all losses.

The Named Storm deductible is a separate, higher deductible that only applies when a storm has been named by the National Hurricane Center. The activation trigger is the naming, not the landfall — so even a Cat 1 storm that brushes northeast Florida and never makes landfall in Duval can still trigger the percentage deductible if it caused covered wind damage in the territory.

The bottom line: your AOP deductible is what shows up in 90 percent of your covered losses. Your Named Storm deductible is what shows up in the one loss that actually matters for your balance sheet.

How a deductible buyback policy erases the six-figure balance sheet risk

A Deductible Buyback policy — also called a "buy-down" — is a specialized secondary insurance policy that wraps around your primary commercial property policy and pays the gap between your primary''s high deductible and a flat retention you can actually budget for.

Here''s the mechanics in plain English. After a covered named-storm loss:

- The primary carrier adjusts the claim in the normal way. They calculate the total covered damage, apply the Named Storm deductible (the $250,000 on our $5M example), and issue payment for everything above the deductible.

- The buyback carrier responds to the deductible. Your $250,000 deductible is the buyback policy''s covered loss. It pays $250,000 minus your retained $5,000 to $10,000 — typically $240,000 to $245,000 of the deductible amount.

- You write one small check. Your out-of-pocket on a $5M-building named-storm loss is the buyback retention plus any uncovered loss tail (usually nothing). You don''t liquidate a position. You don''t refinance. You don''t miss payroll.

The 2026 ROI on a typical Duval commercial buyback:

- Annual premium: $8,500 to $15,000 for a $5M building

- Exposure converted: $250,000 → $10,000 (a $240,000 reduction)

- Effective rate: 3.5% to 6% of the bought-down amount, paid annually

- Break-even math: one named-storm claim in a 16-30 year period pays for the entire buyback premium history

The lender-covenant hack. This is the angle most CFOs miss. Most commercial mortgages written by Florida lenders since 2022 — Ameris Bank, TIAA / EverBank (now branded "Citizens Trust" in some markets), Synovus, and most regional Florida credit unions — include a deductible cap covenant in the loan agreement. The typical 2026 covenant requires the deductible to be no more than 1 to 2 percent of TIV OR a flat $25,000, whichever is lower.

If your primary policy has a 5% Named Storm deductible, you are out of covenant compliance today. The lender can technically declare default. The fastest path to compliance — without changing your primary carrier and without re-shopping the whole account at renewal — is binding a buyback that brings the effective deductible to $5k or $10k. Most lenders accept the buyback policy as satisfaction of the covenant; the COI just needs to evidence the combined retention.

Who writes buyback capacity in Florida 2026? The buyback market is primarily specialty / Excess & Surplus (E&S) — the specialty market for hard-to-place risks. Names you''ll see on quotes include Lloyd''s of London syndicates, AmRisc (a Berkley Company), Munich Re America, Lexington / AIG E&S, and several smaller Florida-domiciled MGAs (Managing General Agents — companies that write policies on behalf of larger carriers) that specialize in CAT-exposed property layers. Your broker should be working at least three of these markets simultaneously on any submission.

Why JAXPORT and Northside industrial owners are binding in May

Three structural reasons the 2026 buyback market is actively writing Jacksonville commercial property — and why owners on the First Coast have a window that South Florida competitors don''t:

1. The "Capacity Surge" from HB 837 carrier re-entry. Seventeen new admitted-market carriers have entered Florida commercial property since the tort-reform bill passed in March 2023. Several of these carriers — Slide, American Coastal, Citizens-takeout entities, and reinsurance-backed startups — have filed buyback / wrap programs specifically priced for North Florida risk. Capacity is real but rationed.

2. North Florida is the "safe haven" relative to South Florida wind PML. PML (Probable Maximum Loss) is the underwriting model that estimates the maximum loss from a 1-in-100-year wind event. Duval and St. Johns counties have a meaningfully lower 30-year hurricane-loss-per-policy track record than Miami-Dade, Broward, or Palm Beach. In 2026, carriers writing CAT capacity get higher returns per dollar of premium on First Coast property because the modeled losses are lower. Translation: your Jacksonville building qualifies for buyback capacity that a comparable Miami building would be declined for.

3. HB 815 (2024) condition-based roof laws. This is the under-discussed 2024 statute that matters most for older Jacksonville commercial inventory. Before HB 815, carriers could decline or non-renew a property purely on roof age. After HB 815, a well-maintained older roof in Riverside, Springfield, or San Marco that passes a current 4-point inspection cannot be declined on age alone. For owners with 15- to 25-year-old commercial roofs, this is the difference between qualifying for admitted-market buyback and being stuck in surplus-only territory.

The timing reality: bind by May 25. Buyback carriers stop binding new business 7 to 14 days before the official June 1 season start. Once a named storm enters the Atlantic basin and is forecast within 72 hours of the Florida coast, binding stops. This is a hard-coded underwriting rule, not a recommendation. The practical implication is that your real bind deadline in 2026 is May 25, 2026 — not June 1.

Wait until Memorial Day weekend and you will not get a policy.

The liquidity angle: faster Loss of Rents and Business Income payouts

The buyback''s other under-discussed benefit is speed. Loss of Rents (also called Business Income or Business Interruption — the coverage that pays your lease revenue while the building is uninhabitable after a covered loss) historically takes 90 to 180 days to start paying on a primary policy because the primary adjuster has to fully scope the damage and the cause-of-loss before triggering BI.

Most 2026 buyback policies trigger Loss of Rents coverage faster — typically 30 to 45 days from First Notice of Loss — because the buyback adjuster is dedicated to deductible-layer claims and works in parallel with the primary adjustment, not after it. For income-producing commercial real estate (multi-tenant office, retail, industrial flex), this is the difference between making payroll, paying the mortgage, and keeping the building staffed in the 60-day window after a storm hits — versus borrowing against the receivables.

Sub-limit benchmarks for 2026 Duval buybacks:

- Business Income / Loss of Rents: $250,000 to $1,000,000 available on most buyback forms

- Extra Expense (the cost of staying operational at a temporary location): $50,000 to $250,000 typical

- Ordinary Payroll (continuing payroll for non-revenue-generating staff during the rebuild): $100,000 to $500,000 available

These are sub-limits on top of whatever your primary policy carries. Treat the buyback as both deductible protection and a faster liquidity bridge.

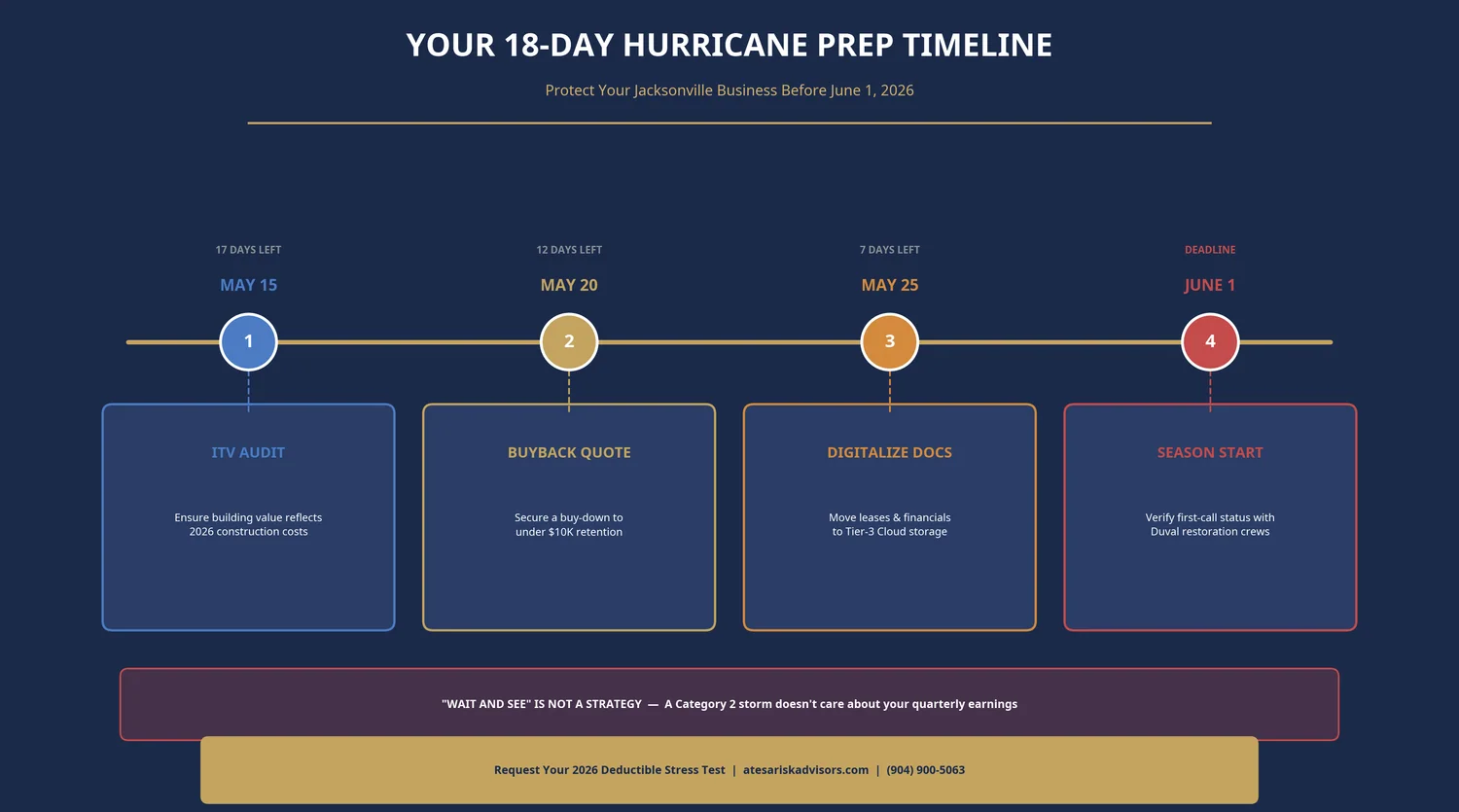

Your 18-day hurricane prep timeline (today: May 13)

This is the day-by-day countdown a typical Duval commercial owner can execute between today and the June 1 season start.

| Date | Task | Goal |

|---|---|---|

| May 15 | ITV audit | Re-check building value against 2026 RSMeans Jacksonville construction-cost data. Stale ITV from 2023 over-prices the buyback. |

| May 17 | Pull current commercial dec page + 5-year loss runs | Build the buyback submission package. Clean loss runs are required by every specialty market. |

| May 20 | Submit to 3 buyback carriers + 1 admitted-market quote refresh | Three E&S specialty markets plus a refreshed primary quote. Quote turnaround: 3 to 5 business days. |

| May 23 | Compare total cost (primary + buyback + lender covenant fit) | Lowest premium is not always lowest total cost. Compare all-in retention, exclusions, BI sub-limits. |

| May 25 | BIND buyback policy | Hard deadline. Carriers tighten capacity 7 to 14 days before June 1; do not roll the dice. |

| May 27 | Lender notification + COI distribution | Update the Schedule of Insurance for the loan servicer; issue new COIs to tenants, vendors, contractors. |

| May 29 | Document digitization | Move leases, financials, inventory records, and pre-loss photos to a Tier-3 cloud backup. Required for clean BI trigger. |

| June 1 | Season start | Verify "first-call" status with Duval restoration crews (LVI Services, Belfor, ServPro). Confirm primary and buyback carrier claims-reporting phone numbers in your binder. |

Download the printable worksheet → CFO Deductible Stress Test Worksheet (PDF). Two-page printable with the 7-step buyback audit checklist, the TIV × deductible exposure math, and the May 13 → June 1 countdown calendar.

Decision matrix: buyback vs higher limits vs lender-required cap

Not every Duval commercial owner needs a buyback. The right strategy depends on cash position, lender covenants, and the maturity of your primary carrier relationship.

| Strategy | Cost | Retained Exposure | Lender-Compliant? | Best For |

|---|---|---|---|---|

| Status quo (5% deductible) | $0 | $250,000 per storm | Often No | Cash-rich owners with no covenant constraint |

| Lower primary deductible (1–2%) | $15k–$25k/yr | $50k–$100k per storm | Yes | Owners with mature primary relationship and willing to pay the premium delta |

| Deductible Buyback wrap | $8.5k–$15k/yr | $5k–$10k per storm | Yes | Owners who want both: keep primary, satisfy lender, minimize total cost |

| Self-Insured Retention (SIR) | $0 ongoing | $250k formally documented | Sometimes | Sophisticated owners with proven reserves and lender accommodation |

For most Duval commercial owners with active loan covenants, the Deductible Buyback wrap is the lowest-total-cost path to compliance. For owners with cash reserves and no lender pressure, the math is closer — but the speed benefit on Loss of Rents alone often justifies the buyback premium.

What we see on Duval commercial buyback submissions in May 2026

"I had a Northside warehouse owner call me on May 8 — 10 days before the 2024 season — saying his lender had just notified him that his 5 percent Named Storm deductible violated his loan covenant. The math on his $8M building was a $400,000 exposure. We placed a buyback with Lloyd''s syndicates in 7 days at a $12,000 annual premium, bringing his effective retention to $10,000. The covenant cleared, and he still bound before Memorial Day. If he had called me the week of May 25, no carrier would have looked at the submission — the binding window was already closed. The 2026 timing reality is identical: bind by May 25 or you''re rolling dice with your lender and your balance sheet."

— Ricardo Alonso, Founder, Atesa Risk Advisors

Florida-Specific Considerations

Florida Statute 627.701(3)(a) — the "one-deductible per named storm" rule. Florida law defines a single hurricane / named-storm deductible per calendar event, not per claim. This means damage from one named storm — even spread across multiple buildings on the same policy schedule — is subject to one deductible. But two separate named storms in a single season = two separate deductibles. The statute applies to commercial property identically to residential [7].

Florida Statute 627.0629 — rate filings for admitted commercial property. All admitted-market commercial property rate changes are filed with the Florida OIR. Buyback / E&S policies are not subject to OIR rate filing because they''re surplus lines, which is why pricing varies more across the buyback market than the primary admitted market [4].

Florida Statute 626.913–932 — Surplus Lines Law. Most buyback policies are surplus lines (E&S) and carry the 5 percent Florida Surplus Lines Tax under FS 626.932. The tax applies to the buyback premium, not the underlying primary premium. Factor it into your total cost when comparing quotes [4].

HB 815 (2024) — condition-based roof inspection rules. Carriers cannot decline or non-renew a Florida property purely on roof age if a current 4-point inspection passes. This is the legislative reason older Jacksonville inventory can now qualify for admitted-market buyback capacity that was unavailable in 2024 [8].

HB 837 (March 2023) — tort reform. Modified comparative negligence, repealed one-way attorney fees for property claims, tightened the bad-faith framework. This is the legislative reason 17 new admitted-market carriers have re-entered Florida commercial property in 2026 — and the reason buyback capacity exists at competitive pricing [5].

NFIP commercial flood vs Private Flood. Buyback policies typically exclude flood (named storm wind only). For complete coverage, layer a private flood policy on top — most Duval / St. Johns commercial owners can replace NFIP''s $500,000 cap with $5M to $25M of private flood for less money. The buyback and the flood policies coordinate cleanly with each other and with your primary [9].

Your 7-Step Buyback Stress Test Timeline

| Step | Time | What happens |

|---|---|---|

| 1. Pull your current commercial dec page | 5 min | Confirm primary TIV, Named Storm deductible %, AOP deductible |

| 2. Calculate raw exposure | 10 min | TIV × Named Storm % = your worst-case out-of-pocket per storm |

| 3. Submit dec page to broker for buyback quotes | 30 min | Three specialty markets (Lloyd''s, AmRisc, Lexington-style) + admitted-market quote refresh |

| 4. Review quotes within 24 hours | 1 day | Compare premium vs retention vs lender covenant fit; verify exclusions and BI sub-limits |

| 5. Verify lender covenant compliance | 2 hours | Send draft binder language to loan servicer; get written acknowledgment |

| 6. Bind buyback policy BEFORE May 25 | 4 hours | Effective date June 1 (season start) or earlier; capacity closes 7–14 days before season |

| 7. Issue updated COIs to lender, tenants, vendors | 24 hours | Document deductible-cap compliance; update lender Schedule of Insurance |

FAQ for Jacksonville commercial property owners

Q: What is a hurricane deductible buyback policy in plain English?

A: It''s a separate insurance policy that wraps around your primary commercial property policy and pays the gap between your primary''s percentage-based Named Storm deductible (typically $150,000 to $250,000 on a Duval commercial building) and a small flat retention you choose (typically $5,000 to $10,000). When a covered named-storm loss happens, the primary carrier adjusts the claim, and the buyback carrier pays the deductible amount above your retained $5k–$10k. You write one small check instead of a six-figure one.

Q: How much does a buyback policy cost for a $5M Jacksonville office building?

A: In the 2026 Duval market, $8,500 to $15,000 per year of annual premium is typical to buy down a $250,000 Named Storm deductible to a $5,000 to $10,000 retention. Pricing depends on building age, occupancy class, wind-mitigation construction features, loss history, and the specific carrier writing the layer. Owners with clean 5-year loss runs and post-2017 construction price at the low end of the range; older buildings or accounts with recent losses price higher.

Q: Will my commercial lender accept a buyback as deductible-cap compliance?

A: In 2026, yes — almost universally. The major Florida commercial lenders (Ameris Bank, TIAA / EverBank, Synovus, Truist commercial RE division, and most regional Florida banks and credit unions) have accepted buyback policies as satisfaction of loan covenant deductible caps since approximately 2022. The lender''s loan-servicing department needs to see a COI evidencing the combined retention ($5k or $10k) in writing; that document is provided by the broker on the day of binding. Some lenders may also request a separate "evidence of insurance" letter signed by the buyback carrier or its underwriter.

Q: What''s the difference between an All-Other-Perils deductible and a Named Storm deductible in Florida 2026?

A: The All-Other-Perils (AOP) deductible is a flat-dollar deductible — typically $5,000, $10,000, or $25,000 — that applies to non-storm covered losses like fires, burglary, vandalism, and most water damage. The Named Storm deductible is a separate, much higher percentage deductible (3 to 5 percent of TIV) that only activates when a storm has been officially named by the National Hurricane Center. The two are independent: you can have a $10,000 AOP and a 5 percent Named Storm deductible on the same policy, applying to different perils.

Q: Does a buyback cover flood damage from the St. Johns River?

A: No. Buyback policies typically exclude flood entirely — they buy down the wind deductible only. For flood coverage on Duval / St. Johns commercial property, you need a separate flood policy: either NFIP commercial (capped at $500,000 building / $500,000 contents) or, more commonly in 2026, a private flood policy with $5M to $25M limits. The buyback, the primary, and the private flood policy all coordinate independently with each other.

Q: How late in the season can I bind a buyback policy?

A: The practical deadline in any Florida hurricane season is May 25 — about 7 days before the official June 1 season start. Once any named storm is forecast within 72 hours of the Florida coast, all specialty markets stop binding new business until the threat passes (a rule called the "binding moratorium"). Some carriers maintain stricter cutoffs at May 20 or even May 15. The safest practice: complete the audit by May 17, get firm quotes by May 22, bind by May 25.

Q: Does Florida Statute 627.701 apply to commercial property the same way it does to residential?

A: Yes. FS 627.701(3)(a) — Florida''s "one deductible per named storm" rule — applies to both residential and commercial property policies. The deductible attaches at the moment the National Hurricane Center names the storm, and only one Named Storm deductible applies to all covered damage from that single calendar event (even across multiple buildings on the same policy schedule). However, two distinct named storms in one season = two separate deductibles applied. There is no annual aggregate cap by statute.

Q: If my building has multiple named storms in one season, does the buyback respond multiple times?

A: Yes — most 2026 buyback policies have no per-season aggregate cap on the number of named-storm events they will respond to. Each named-storm event triggers a separate deductible on the primary and a separate response from the buyback. Confirm this in writing with your broker before binding; a few specialty carriers do impose per-season aggregates ($500k–$1M typical), and you want to know which form you''re buying.

Related Reading

- How to Lower Commercial Property Insurance in Duval County: The 2026 Market Guide — The CFO audit for Duval office, retail, and industrial — 10–18% rate softening in 2026.

- Got Non-Renewed in Jacksonville? Your 30-Day Replacement Playbook (2026) — The day-by-day replacement playbook if your current carrier just dropped you.

- Does Commercial Property Insurance Cover Hurricanes in Florida? The 2026 Reality Check — The companion piece on what your primary policy does (and doesn''t) cover when the storm hits.

How Atesa Risk Advisors Can Help

Print the worksheet first → Download the CFO Deductible Stress Test Worksheet. Two pages: the 7-step buyback audit checklist plus the May 13 → June 1 countdown calendar.

Atesa is a Florida independent insurance brokerage that places deductible buyback wraps for Duval / St. Johns commercial property owners every week during the May binding window. We work the specialty (E&S) markets — Lloyd''s syndicates, AmRisc, Munich Re America, Lexington, and the new 2026 admitted carriers — in parallel, and we know which markets are still writing capacity in the final two weeks before season.

If your 2026 renewal already passed and you''re now stuck with a percentage-based Named Storm deductible you cannot afford, the buyback is your fastest path to compliance and to a sleepable balance sheet. The audit takes one phone call. The submission goes out within 24 hours. The binding window closes May 25.

Need to close a six-figure deductible gap before June 1? Get your free 24-hour buyback stress test at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Florida Office of Insurance Regulation, Commercial Property Insurance Market Report Q1 2026 — Duval / First Coast Named Storm deductible benchmarks and buyback layer pricing — floir.com

[2] Florida OIR, 2026 Commercial Rate Filing Database — Named Storm deductible filings by admitted carrier

[3] Insurance Information Institute (III), Deductible Buyback and Wrap Policy Overview — iii.org

[4] Florida Statute 627.0629 — Florida commercial property rate filings — leg.state.fl.us/statutes/627.0629; Florida Statute 626.913–932 — Surplus Lines Law and 5% surplus lines tax — leg.state.fl.us/statutes/626.913

[5] Florida House Bill 837 (2023) — Civil Remedies / tort reform — flsenate.gov/Session/Bill/2023/837

[6] Florida OIR Property Insurance Stability Report 2025 — admitted carrier re-entry tracking

[7] Florida Statute 627.701(3)(a) — Hurricane / named storm deductible (one-event rule) — leg.state.fl.us/statutes/627.701

[8] Florida House Bill 815 (2024) — Property Insurance, condition-based roof inspection — flsenate.gov/Session/Bill/2024/815

[9] FEMA National Flood Insurance Program (NFIP) — Commercial flood limits and Risk Rating 2.0 methodology — fema.gov/flood-insurance

External Resources for Jacksonville commercial property owners:

- City of Jacksonville Emergency Preparedness Division — Duval hurricane evacuation zones, shelter information, and pre-storm checklists

- JAX Chamber of Commerce — Jacksonville business community resources, commercial real-estate market intelligence, and hurricane-season business continuity planning

- Florida Office of Insurance Regulation Company Search — Verify carrier admitted status and financial-stability ratings before binding

- Florida Department of Financial Services — Division of Consumer Services — Carrier complaints and licensing verification. Hotline: 1-877-693-5236

- National Hurricane Center — Atlantic basin tropical outlook and named-storm tracking

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. Ricardo has structured deductible buybacks for Jacksonville-area commercial owners through every hurricane season since the post-Ian carrier exits began in 2022.