Florida Small Business Cyber Insurance 2026: The Buyer's Guide to Real Coverage in a Privacy Law Storm

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 26, 2026

Key Takeaways

- Florida's Information Protection Act (§ 501.171 F.S.) gives businesses exactly 30 days to notify affected residents after a breach — civil fines for missing that deadline reach $500,000 per breach event, enforced by the Florida Attorney General [1].

- Florida's Digital Bill of Rights (SB 262, 2023) created new third-party privacy liability that standard general liability and Business Owner's Policies explicitly exclude under ISO cyber exclusion endorsements added in 2014 [2].

- In 2026, every major cyber carrier — Chubb, Travelers, Beazley, Coalition, At-Bay — requires multi-factor authentication (MFA) on all email, VPN, and admin accounts as a hard condition of coverage, not a recommendation [5].

- A cyber policy has two distinct sections: first-party coverage (your own direct losses) and third-party coverage (claims customers, card brands, and regulators file against you). Most comparison platforms show only one.

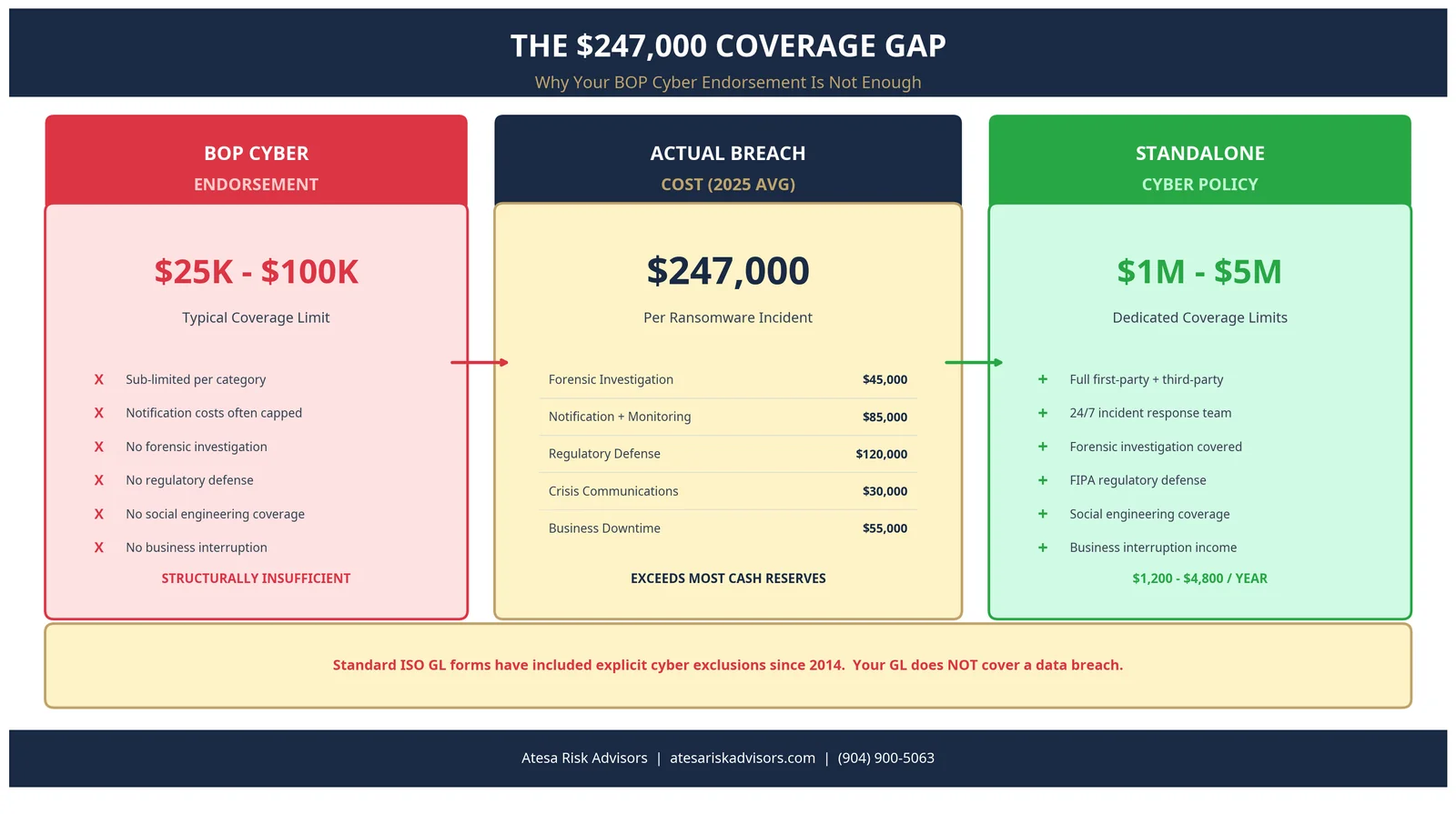

- Ransomware incidents affecting small businesses averaged $247,000 in total costs per event in 2025 — covering downtime, forensics, notification, and ransom — a figure that exceeds most small business cash reserves [4].

- Your Business Owner's Policy (BOP) almost certainly contains a cyber exclusion or a sub-limited endorsement of $25,000–$100,000 that is structurally insufficient for a real breach event.

- A licensed Florida independent broker accesses specialty markets — Beazley, Coalition, At-Bay, Cowbell — that do not appear on AI comparison platforms, with policy forms that are frequently broader at the same or lower premium.

Cyber insurance for Florida small businesses pays for direct financial losses and third-party claims arising from data breaches, ransomware attacks, and privacy law violations — covering forensic investigation, breach notification letters, customer credit monitoring, regulatory defense, and lost business income during system downtime. In Florida, a standalone cyber policy for a business under $5 million in annual revenue typically runs $1,200–$4,800 per year, depending on industry, data type handled, and security controls in place. Carriers in 2026 require multi-factor authentication (MFA) and endpoint detection software (EDR) as non-negotiable baseline conditions before they will bind a policy.

Why Florida Small Businesses Are Prime Targets in 2026

Florida processes more tourism transactions, real estate closings, and healthcare visits than nearly any other state. That concentration of personal data — credit card numbers, patient records, Social Security numbers, wire transfer instructions for property closings — makes Florida small businesses disproportionately attractive to cybercriminals who automate their targeting at industrial scale.

The FBI's Internet Crime Complaint Center (IC3) consistently ranks Florida among the top three states for total reported cyber losses nationwide [4]. Small businesses are specifically targeted because they hold high-value data while investing a fraction of what large enterprises spend on security. A ransomware group can encrypt a dental practice's patient records or a law firm's client files and extract six figures in ransom from a 10-person operation that has no dedicated IT staff and no documented incident response plan.

Florida small businesses carrying the highest exposure include:

- Medical, dental, and mental health practices — patient health records sell for $250–$1,000 each on criminal markets (versus pennies for a credit card number) because a medical identity is permanent and cannot be changed or cancelled like a card account.

- Real estate agencies, title companies, and mortgage brokers — wire transfer fraud (also called business email compromise, or BEC) is the single highest-cost cyber claim type in Florida; the FBI IC3 reports the average loss per wire fraud incident exceeds $118,000 [4].

- Restaurants and hospitality businesses — point-of-sale system compromise triggers PCI-DSS (the payment card industry's mandatory security standard) forensic investigations and card brand fines that general liability will not cover.

- Law firms — attorney-client privilege data commands ransom premiums and triggers Florida Bar reporting obligations in addition to FIPA's notification requirements.

- Contractors and construction subcontractors — payment diversion schemes targeting construction accounts payable have surged as project management moves to cloud-based platforms like Procore and Autodesk Build, creating new email compromise attack surfaces.

Florida's Privacy Law Landscape: Your Specific Legal Exposure

Buying cyber insurance without understanding Florida's specific legal framework is like buying flood insurance without knowing whether you are in a Special Flood Hazard Area. A Florida-licensed broker who understands the state's regulatory environment — not a generalist algorithm — is the person who identifies and closes the gaps that matter most to your specific business.

Florida Information Protection Act (FIPA) — § 501.171, Florida Statutes

FIPA is Florida's primary data breach notification statute [1]. Any business that maintains "personal information" of Florida residents — which includes Social Security numbers, driver's license numbers, financial account numbers, and medical or health insurance information — must notify all affected individuals within 30 days of determining that a breach has occurred and is likely to cause harm.

The civil penalties for non-compliance escalate quickly:

- $1,000 per day for each day notification is delayed beyond the 30-day window

- $50,000 per additional 30-day period thereafter

- Maximum civil penalty: $500,000 per breach event

The Florida Attorney General enforces FIPA and has pursued enforcement actions against businesses of all sizes. Breaches affecting more than 500 Florida residents also trigger mandatory notification to the Florida Department of Legal Affairs — a notification that becomes a public record, drawing media coverage and class-action attorney attention regardless of the underlying facts [9]. A cyber insurance policy covers the forensic investigation needed to calculate your notification obligations, the notification letters and credit monitoring services themselves, and legal defense if the Attorney General opens a civil inquiry.

Florida Digital Bill of Rights (SB 262, 2023 — Rule-Making Ongoing Through 2026)

The Florida Digital Bill of Rights (SB 262) grants consumers enumerated rights over personal data held by covered businesses: the right to access, correct, delete, and opt out of the sale of their data for advertising and profiling [2]. While the law currently applies most directly to businesses processing data of more than 100,000 Florida consumers per year, its scope is expanding through ongoing agency rule-making and litigation, and businesses in data-intensive sectors should assess their exposure proactively.

The key insurance exposure: if a consumer submits a data deletion request and your business subsequently suffers a breach that exposes data that should have been deleted, you face compounded liability — both for the breach itself and for failing to honor a statutory consumer right. The third-party privacy liability section of a comprehensive cyber policy covers legal defense costs and potential settlements from these claims.

Florida's 2026 Cybersecurity Immunity Bill (SB 692)

SB 692 (2026) creates a civil immunity safe harbor for Florida businesses whose cybersecurity programs substantially conform to a recognized national framework — the NIST Cybersecurity Framework, ISO/IEC 27001, or sector-specific standards including HIPAA's Security Rule for healthcare entities [3][8]. A business that suffers a breach despite a documented, implemented security program aligned to one of these frameworks can assert immunity against third-party civil claims arising from that breach.

The insurance implication is direct: the security controls that cyber carriers require as a condition of coverage in 2026 are the same controls that can qualify your business for SB 692 immunity. Investing in your security posture is not just about getting a better premium — it may also reduce or eliminate a significant portion of your third-party civil liability exposure if a breach occurs.

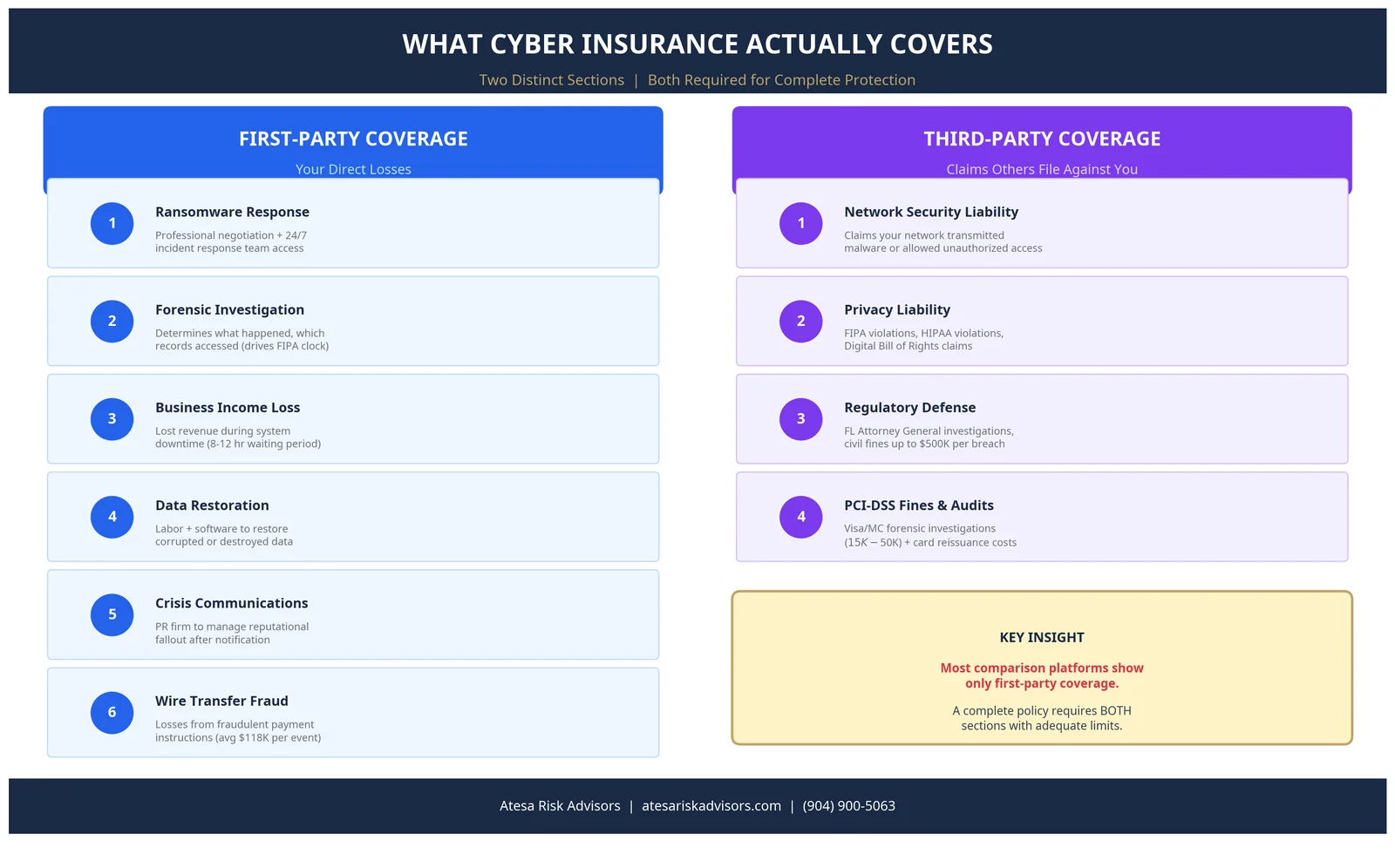

What Cyber Insurance Actually Covers: First-Party vs. Third-Party

Most small business owners evaluating cyber insurance focus on one number: the annual premium. The more consequential question is whether the policy covers both dimensions of a cyber event — the costs your business incurs directly, and the claims that customers, card brands, and regulators bring against you.

First-Party Coverage: Your Direct Losses

- Ransomware response and cyber extortion: Pays professional ransom negotiation services (not just the ransom payment itself) and provides immediate access to a breach response team. Specialty carriers — Beazley, Coalition, At-Bay — include 24/7 incident response services with a live forensics and legal team; that access is often worth more in a live event than the policy's dollar limits.

- Forensic investigation: Pays a licensed digital forensics firm to determine what happened, which systems were affected, and exactly which records were accessed. Without this investigation, you cannot calculate your 30-day FIPA notification clock, and you risk inadvertently excluding affected individuals from required notice.

- Business income interruption: Reimburses lost revenue and extra expenses during the period your systems are offline or degraded. Policies specify a "waiting period" — typically 8 to 12 hours — before this coverage activates. A shorter waiting period is meaningfully better for businesses where every hour of downtime directly costs revenue.

- Data restoration: Pays the labor and software costs to restore or recreate data that was corrupted or destroyed by the attack. This covers recovery costs, not the inherent value of the data itself.

- Crisis communications: Covers a public relations firm to manage reputational fallout. When a notification letter goes to 2,000 or 5,000 of your customers, the message framing can determine whether you retain 90% of them or lose 40%.

- Social engineering and funds transfer fraud: Covers losses from fraudulent wire transfer instructions — where a criminal impersonates a vendor, attorney, or client to redirect payment to a criminal account. This is one of the most frequent cyber claim types for Florida businesses. It is not included in all cyber policies, and many that do include it cap it at a sub-limit of $25,000. Confirm this coverage is present and that the limit reflects your typical transaction exposure before binding.

Third-Party Coverage: Claims Others File Against You

- Network security liability: Covers claims that your network transmitted malware to a third party, or that a security failure in your systems allowed unauthorized access to their data — common in vendor and supply chain breach scenarios.

- Privacy liability: Covers claims arising from FIPA violations, HIPAA violations (for healthcare businesses) [7], Florida Digital Bill of Rights claims, and other privacy statute breaches — including Florida Attorney General investigation costs and any resulting civil settlement or judgment.

- Regulatory fines and penalties: Covers civil fines where insurable under applicable law. FIPA penalties are civil in nature, and some policy forms cover them — but this varies significantly by carrier and policy form language. A broker reads this language so you do not discover the gap when filing a claim.

- PCI-DSS fines and forensic assessments: If your business accepts credit cards and suffers a cardholder data compromise, Visa and Mastercard can impose forensic audit requirements (a Qualified Security Assessor investigation typically costs $15,000–$50,000), card reissuance costs charged through your acquiring bank, and direct fines. A cyber policy that explicitly includes PCI coverage absorbs these costs.

The 2026 Underwriting Gauntlet: What Carriers Require Before They Will Bind

Cyber underwriting has transformed fundamentally since 2020. The days of a one-page application resulting in an automatic quote are gone. If your security posture does not meet baseline requirements, standard admitted-market carriers will decline your application — and that declination is recorded in industry databases.

The controls that Chubb, Travelers, Beazley, Coalition, Cowbell, and At-Bay now require as minimums for small business accounts [5]:

- Multi-Factor Authentication (MFA): Required on all email accounts (not just administrators), VPN connections, remote desktop access, cloud platforms (Microsoft 365, Google Workspace, AWS), and privileged admin portals. MFA is the single most effective control against credential theft — the root cause of more than 80% of breach events according to the Verizon Data Breach Investigations Report [5]. Carriers issue policy exclusions or outright denials for events originating from accounts not protected by MFA.

- Endpoint Detection and Response (EDR): Real-time behavioral monitoring software installed on every workstation and server — not signature-based antivirus that only detects known threats. EDR detects attackers moving laterally through a network before they can deploy ransomware across all devices. Must be deployed on 100% of managed endpoints.

- Offline or immutable backups: Backups must be physically or logically isolated from the production network so ransomware cannot reach and encrypt them. The industry standard is the 3-2-1 rule: three copies, two different storage media types, one copy offsite or air-gapped from the live network.

- Patch management: Operating systems and critical applications updated within 30 days of a vendor security patch release. Unpatched vulnerabilities remain the second most common ransomware entry vector after credential theft.

- Security awareness training: Documented annual phishing simulation and security training for all employees — with completion records that can be provided to the underwriter if requested.

- Privileged access management: Administrator-level system access limited to only employees who require it for their role, with access lists reviewed and reconciled at least annually.

A Florida broker who specializes in cyber can conduct a pre-application security gap review, identify deficiencies before you submit to an underwriter, and direct you toward carriers whose criteria match your current posture. This matters because a declined cyber application is recorded in the CLUE commercial database — a record that can complicate future applications at carriers that did not even see the original declination.

The Coverage Gap You Almost Certainly Have Right Now

If your business carries a general liability policy or a Business Owner's Policy (BOP), you may have been told you have "some cyber coverage." For a real breach event, you almost certainly do not have adequate coverage.

Standard ISO general liability policy forms (CG 00 01) have included explicit electronic data and cyber exclusions since 2014. A standard GL policy does not cover a data breach. If you are uncertain, ask your current agent to identify the specific cyber sub-limit in your policy — not the overall GL limit, the cyber-specific sublimit — and compare it against the average $247,000 total cost of a small business ransomware incident in 2025 [4].

BOP cyber endorsements, when they exist, typically provide $25,000–$100,000 in coverage — frequently sub-limited further for specific cost categories like notification fees, forensic services, and business interruption. The notification and credit monitoring costs alone for a breach affecting 1,000 Florida residents can exceed $40,000. A $25,000 endorsement is not a backstop for a meaningful breach event.

The only structurally adequate solution is a standalone cyber liability policy — a dedicated policy form with limits calibrated to your actual revenue, industry, and data exposure.

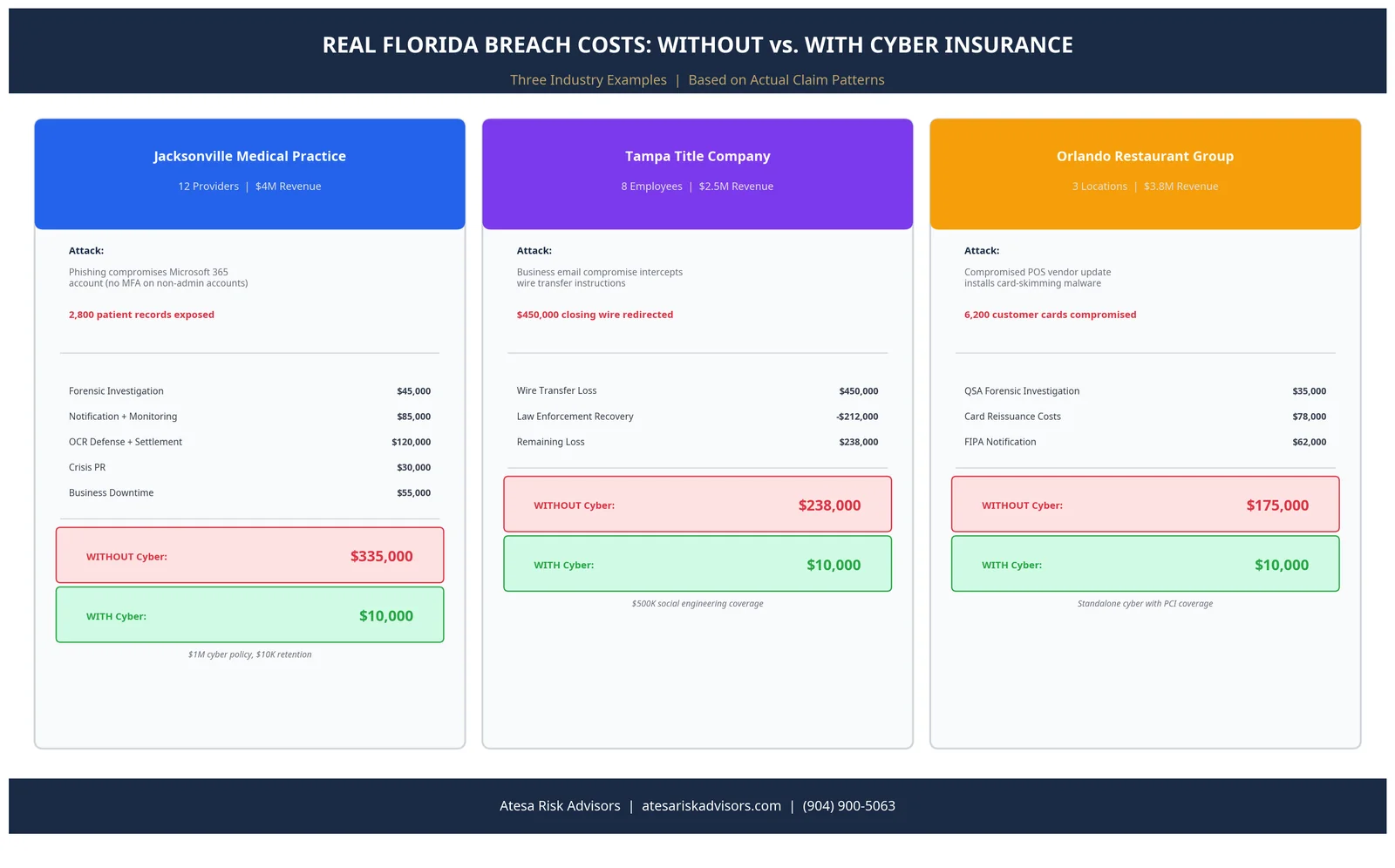

Florida Industry Examples: What a Real Cyber Event Costs

Jacksonville Medical Practice (12 Providers, $4M Revenue)

A phishing email sent to a front-desk employee compromises her Microsoft 365 account because MFA had not been enabled on non-administrator accounts. The attacker pivots from her mailbox into the practice management system and extracts records for 2,800 patients. Under FIPA, the practice must notify all 2,800 patients within 30 days. HHS receives notification under HIPAA's breach notification rule [7]. An OCR investigation follows. Estimated total costs without cyber insurance: forensic investigation ($45,000), notification letters and credit monitoring ($85,000), OCR defense and settlement ($120,000), crisis PR ($30,000), lost revenue from system downtime ($55,000) — total $335,000. With a $1M cyber policy carrying a $10,000 retention: out-of-pocket exposure — $10,000.

Tampa Title Company (8 Employees, $2.5M Revenue)

A business email compromise attack intercepts an ongoing email thread between the title company and a buyer approaching a $450,000 property closing. The criminal — using a domain differing from the seller's attorney's address by one character — provides new wire transfer instructions. The buyer's funds are wired to the criminal's account. The title company's cyber policy includes $500,000 in social engineering / funds transfer fraud coverage. After law enforcement recovers $212,000, the policy pays the remaining $238,000 above the $10,000 retention. Net exposure above what insurance covers: $10,000.

Orlando Restaurant Group (Three Locations, $3.8M Revenue)

A compromised point-of-sale vendor update installs card-skimming malware across all three POS terminals, capturing card data for 6,200 customers over 90 days. Visa initiates a forensic investigation via a Qualified Security Assessor (cost: $35,000). Card reissuance costs assessed against the merchant: $78,000. FIPA notification to 6,200 Florida residents: $62,000. Without cyber insurance: $175,000 in immediate costs. With a standalone cyber policy including PCI coverage: all of the above covered above a $10,000 retention.

What a Licensed Florida Broker Delivers That No Platform Can Replicate

Online comparison tools and AI-powered platforms can return a cyber premium quote in minutes. Here is what they structurally cannot do:

- Access specialty cyber markets. Beazley, Coalition, At-Bay, and Cowbell do not distribute through all comparison platforms. These carriers' policy forms are frequently broader than standard admitted-market forms — some cover funds transfer fraud without a sub-limit; others bundle 24/7 incident response retainer access that standard carriers charge extra for; several use broader definitions of "computer fraud" that capture modern attack patterns legacy forms exclude.

- Negotiate sub-limits that match your actual exposure. A title company that regularly wires $500,000 at closing needs a social engineering limit that reflects that exposure — not the $25,000 default. A broker negotiates a higher limit or identifies a carrier whose base form does not cap it.

- Evaluate policy language, not just premium. The definition of "unauthorized access," the scope of "business interruption," whether "regulatory fines" are covered under the policy's governing law — these distinctions are invisible on a comparison platform but determine whether your claim is paid in full or disputed at the worst possible moment.

- Apply Florida-specific regulatory knowledge. FIPA's 30-day notification window, the evolving Digital Bill of Rights exposure, and the SB 692 immunity framework create specific coverage needs that are invisible to a national generalist tool that does not track Florida's legislative and regulatory environment.

- Advocate when a claim is disputed. When a carrier's initial response to a breach claim invokes an exclusion, your broker — who placed the policy, documented the coverage expectations at binding, and knows the underwriter — is positioned to push back effectively. This is where the difference between a specialist and a platform is most financially significant.

How Much Does Cyber Insurance Cost for Florida Small Businesses in 2026?

Cyber premiums are driven by annual revenue, industry and data type handled, security posture, and claims history. For Florida small businesses with documented MFA, EDR, and offline backups already in place, 2026 market benchmarks are [10]:

| Annual revenue | Typical premium | Typical policy limit |

|---|---|---|

| Under $1M | $800–$2,000 / year | $1M |

| $1M–$5M | $1,500–$4,800 / year | $1M–$2M |

| $5M–$10M | $4,000–$12,000 / year | $2M–$5M |

Healthcare businesses, financial services firms, and legal practices pay 30–80% above these benchmarks due to elevated data sensitivity and regulatory complexity. Businesses that cannot demonstrate baseline security controls are redirected to the excess and surplus (E&S) market — where premiums run 40–150% above admitted-market rates with more restrictive policy conditions.

Policy retention — the amount your business pays out of pocket before the policy responds, equivalent to a deductible — typically runs $2,500–$25,000 for small business cyber accounts. A $10,000 retention generally reduces premiums by 15–30% compared to a $2,500 retention. Choose the highest retention your business cash flow can absorb without jeopardizing operations in a worst-case breach scenario.

Your 7-Step Cyber Insurance Timeline

| Step | Action | Why |

|---|---|---|

| 1 | Assess your current security posture. Confirm MFA on all email/VPN/admin, EDR deployed on all devices, and offline/immutable backups (3-2-1 rule). | These are hard underwriting requirements — gaps result in declined applications or coverage exclusions. |

| 2 | Inventory your data exposure. Identify what categories of Florida residents' personal data your business holds and the maximum number of individuals. | Determines your FIPA notification risk and the policy limits you need. |

| 3 | Engage a licensed Florida cyber broker. Work with a broker who can access specialty markets — Beazley, Coalition, At-Bay, Cowbell. | Pre-qualification before submission avoids a declined application in the CLUE commercial database. |

| 4 | Complete the cyber underwriting application. Provide supporting documentation of security controls. | Speeds approval and improves offer terms. |

| 5 | Compare policy forms, not just premiums. Confirm social engineering coverage is present and limits match your typical transaction exposure. Verify both first-party and third-party sections. | Premium-shopping alone misses the gap that decides whether your claim is paid. |

| 6 | Select your retention and bind the policy. Choose the highest retention your operating cash flow can absorb without disrupting payroll. | A $10,000 retention produces meaningful premium savings without unmanageable out-of-pocket exposure. |

| 7 | Save your carrier's breach response hotline. | FIPA's 30-day clock starts when you determine a breach occurred — the worst time to search for a phone number is during an active ransomware event. |

Florida-Specific Considerations

Florida's regulatory environment is in active rule-making for cyber and privacy compliance through 2026 and 2027. SB 262 (Digital Bill of Rights) implementing rules are still being clarified by the Florida Department of Legal Affairs [9]. SB 692's cybersecurity immunity framework rewards businesses with documented programs aligned to recognized frameworks — work that often happens during cyber insurance binding because carriers ask the same documentation questions [3][8]. Aligning your security program to the NIST Cybersecurity Framework [6] simultaneously qualifies you for better cyber premium AND for SB 692 immunity.

For Florida small businesses, the practical sequence is: (1) implement carrier-required controls (MFA, EDR, backups), (2) document them, (3) bind a standalone cyber policy with the documentation you just produced, (4) keep the documentation current for any future SB 692 immunity claim.

FAQ for Florida Small Business Owners

Q: Does my general liability or Business Owner's Policy cover a data breach?

A: Almost certainly not with adequate limits. Standard ISO GL policy forms (CG 00 01) have included explicit electronic data exclusions since 2014. Standard GL does not cover a data breach or ransomware event. BOP cyber endorsements typically cap coverage at $25,000–$100,000 — far below the average $247,000 total cost of a small business ransomware incident. A standalone cyber policy is the only structurally adequate solution.

Q: What is the difference between first-party and third-party cyber coverage?

A: First-party coverage pays your own direct losses: forensic investigation, ransomware response, business interruption income, breach notification, and crisis PR. Third-party coverage pays when others file claims against you: customer lawsuits for exposed data, PCI card brand fines, FIPA regulatory penalties, and HIPAA investigation costs. A complete policy includes both. Many lower-cost policies provide primarily first-party coverage — confirm both sections are present and adequately limited before binding.

Q: Does Florida law require small businesses to carry cyber insurance?

A: Florida does not currently mandate cyber insurance for most businesses. However, FIPA (§ 501.171 F.S.) imposes mandatory breach notification obligations and civil fines up to $500,000 per breach for violations — costs that cyber insurance is specifically designed to fund. Many commercial leases, vendor contracts, and professional service agreements now include cyber insurance as a contractual requirement regardless of statute.

Q: What is FIPA and how does the 30-day notification window work?

A: FIPA is the Florida Information Protection Act (§ 501.171, Florida Statutes). It requires any business maintaining personal information of Florida residents to notify all affected individuals within 30 days of determining a breach has occurred and is likely to cause harm. "Personal information" includes Social Security numbers, driver's license numbers, financial account data, and health or medical insurance information. Late notification triggers civil penalties of $1,000 per day (days 1–30) and $50,000 per additional 30-day period thereafter, up to a maximum of $500,000.

Q: Can I be personally liable as a business owner for my company's data breach?

A: Potentially. Sole proprietors and general partners face direct personal liability because no corporate structure separates personal assets from business obligations. For LLC and corporation owners, liability generally remains at the entity level — but personal exposure can arise from personal guarantees in contracts requiring cyber insurance, or in cases where courts pierce the corporate veil due to evidence of grossly negligent security practices.

Q: What security controls do I need to qualify for cyber coverage in 2026?

A: The mandatory baseline for standard-market carriers: MFA on all email, remote access, and admin accounts; EDR software deployed on every device; offline or immutable backups following the 3-2-1 standard; active patch management within 30 days of patch release; and documented annual employee security training. Missing MFA on any admin or email account will result in either a declined application or a policy with a specific exclusion for events originating from unprotected accounts — effectively negating coverage for the most common attack type.

Q: Does cyber insurance cover ransomware attacks?

A: Yes. Ransomware response is a core covered peril under most cyber policies. Coverage includes professional ransom negotiation services, forensic investigation, system restoration costs, and lost business income during system downtime. Some policies also cover the ransom payment itself, subject to OFAC (U.S. Treasury) screening to confirm no payment is directed to a sanctioned threat actor or nation-state.

Q: What is a cyber policy "retention" and how much should I carry?

A: A retention is the amount your business pays out of pocket before the cyber policy responds — functionally identical to a deductible. Retentions for small business cyber typically range from $2,500 to $25,000. A $10,000 retention generally reduces premiums by 15–30% versus a $2,500 retention. Choose the highest retention your cash flow can absorb in a genuine emergency without jeopardizing your ability to pay employees, vendors, and operating costs simultaneously.

Q: Does a solo professional or sole proprietor need cyber insurance?

A: Yes, particularly in professional service fields. A solo accountant, therapist, real estate agent, or attorney who handles client personal data faces identical FIPA notification obligations and third-party liability exposure as a larger firm — with fewer resources to absorb the costs unaided. Policies for very small businesses with minimal revenue can run as low as $800 per year and provide meaningful protection for the breach scenarios most likely to affect a solo practice.

Q: What is social engineering / wire transfer fraud coverage and why does it matter for Florida businesses?

A: Social engineering coverage — also called funds transfer fraud or BEC coverage — protects against losses from fraudulent payment instructions, where a criminal impersonates a trusted party to redirect a wire transfer or ACH payment to a criminal account. The FBI IC3 reports the average loss per BEC wire fraud incident exceeds $118,000 [4]. This is among the most frequent cyber claim types for Florida businesses in real estate, construction, title, and professional services. Many policies sub-limit this coverage at $25,000 — if your business sends wire transfers regularly, confirm the limit reflects your typical transaction size.

Q: How does the Florida Digital Bill of Rights (SB 262) create insurance exposure?

A: SB 262 grants Florida consumers rights to access, correct, and delete their personal data. If a consumer submits a deletion request and your business subsequently suffers a breach exposing data that should have been deleted, you face compounded liability — for the breach and for violating a statutory consumer right. SB 262 compliance inquiries and regulatory investigations require legal defense — costs covered under the privacy liability section of a comprehensive cyber policy.

Q: How long does it take to get a cyber insurance quote in Florida?

A: For small businesses under $5 million in annual revenue with MFA and EDR already deployed: 24–72 hours after completing the application. Larger or higher-risk accounts — healthcare practices, financial services firms, law firms — typically require 5–10 business days for underwriter review, and some carriers conduct automated external scans of your internet-facing systems as part of underwriting. A broker who pre-qualifies your account and routes you to the right carrier for your risk profile significantly reduces turnaround time and improves offer terms.

Related Reading

- General Liability Insurance Cost in Florida (2026) — How standard GL is priced in Florida and why it does not backstop a cyber event.

- Florida Commercial Insurance Rates 2026: The Business Owner's Guide — Market context for premium expectations across all commercial lines.

- 5 Insurance Mistakes Florida Business Owners Make — The most expensive coverage gaps we audit out of new client policies.

How Atesa Risk Advisors Can Help

Atesa Risk Advisors is a Jacksonville-based, Florida-licensed (2-20 General Lines) independent brokerage serving Florida businesses statewide. We are a RamseyTrusted provider and shop 40+ A-rated carriers — including the specialty cyber markets (Beazley, Coalition, At-Bay, Cowbell) that most national comparison platforms cannot reach.

Cyber underwriting in 2026 is more like a security audit than an insurance application. Working with a broker who knows which questions the carriers ask, which controls they require, and which policy forms include the coverage that matters for Florida regulatory exposure can be the difference between a declined application that stays on your record and a competitive quote bound on the first submission.

Want a cyber pre-qualification review for your Florida small business? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] § 501.171, Florida Statutes — Florida Information Protection Act (FIPA)

[2] Florida SB 262 — Florida Digital Bill of Rights (2023)

[3] Florida SB 692 — Cybersecurity Standards Immunity Bill (2026)

[4] FBI Internet Crime Complaint Center (IC3) — Annual Reports

[5] Verizon Data Breach Investigations Report (DBIR)

[6] NIST Cybersecurity Framework

[7] HHS — HIPAA Breach Notification Rule

[8] IAPP — Florida SB 692 Data Breach Immunity Analysis

[9] Florida Department of Legal Affairs — Data Breach Notification Registry

[10] Florida Office of Insurance Regulation (OIR)

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. He works with Florida small businesses to align cybersecurity posture and insurance coverage so a breach event does not become an existential financial event.