Golf Cart vs. LSV Insurance in Florida (2026): Why Your Homeowners Policy Won't Cover That Neighborhood Crash

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 13, 2026

Key Takeaways

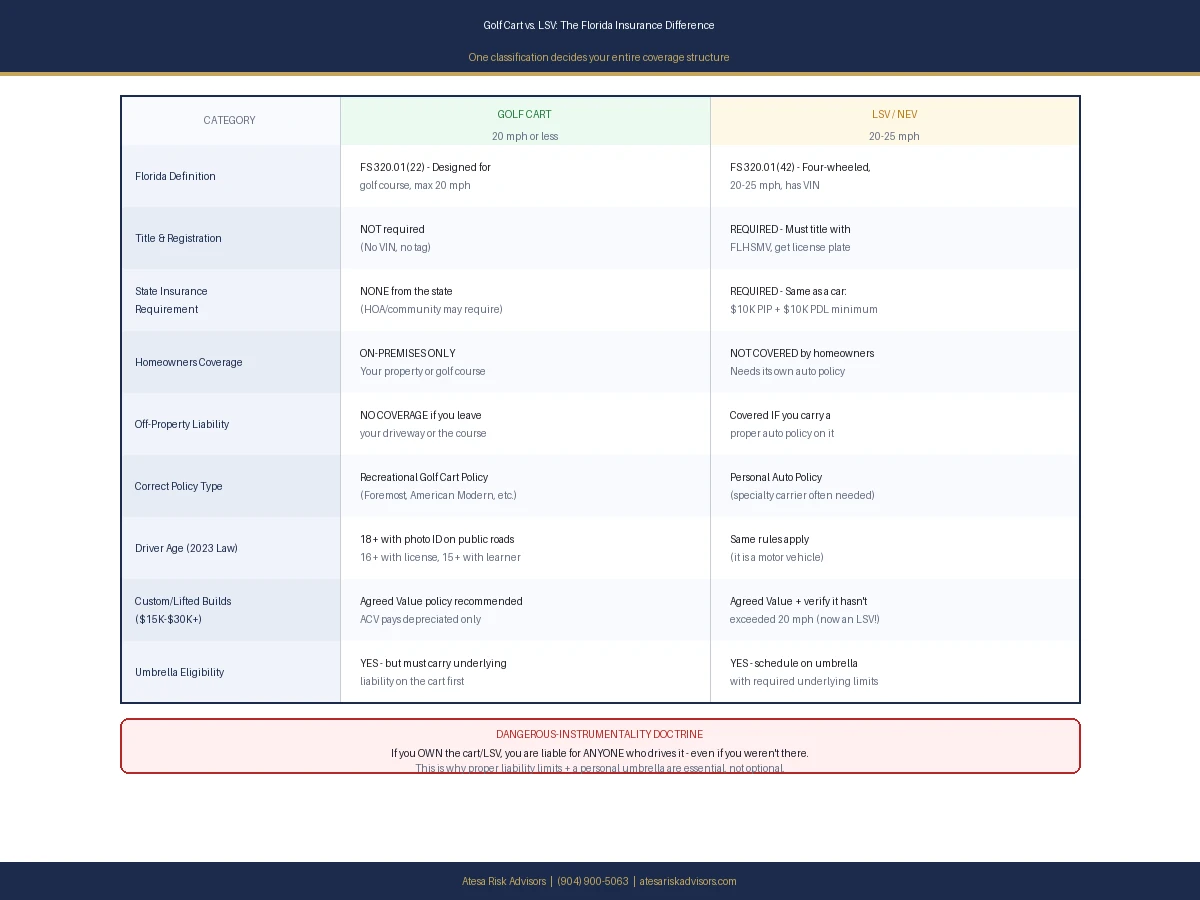

- In Florida, a "golf cart" (top speed 20 mph or less) and a "low-speed vehicle" or LSV (20–25 mph) are legally different machines — and that single distinction decides whether you need a registration, a tag, and a full auto policy.

- Most standard homeowners policies cover a golf cart only on your own property or a golf course. The moment you drive to a neighbor's house, the pool, or the community pad, your liability coverage can vanish.

- An LSV is a motor vehicle under Florida law. It must be titled, registered with the FLHSMV, and carry at least $10,000 PIP and $10,000 PDL — the same floor as your car.

- Under Florida's dangerous-instrumentality doctrine, the cart's owner is on the hook for whatever a borrower, teenager, or guest does behind the wheel — even if you weren't there.

- A 2023 state law raised the minimum age and added a government-ID requirement for operating carts on public roads; enforcement and confusion both climbed into 2026.

- Custom, lifted, and lithium-converted carts now cost $15,000–$30,000+. Insuring them at "agreed value" rather than actual cash value is a placement decision, not a price you find on a quote engine.

- The right answer is rarely the cheapest add-on. Matching the machine to the correct policy form, then backing it with a personal umbrella, is where an experienced advisor earns the fee.

Florida homeowners ask one of two questions about golf carts: "Do I even need insurance?" and, far too often after a crash, "Why won't my homeowners policy pay?" The honest answer to both is the same — it depends entirely on how your machine is classified and where you drive it. A standard homeowners policy generally protects a golf cart only on your residence premises or while golfing; ride it through the neighborhood and you may have no liability coverage at all. An LSV, by contrast, is a registered motor vehicle that legally requires its own auto policy. Getting this wrong is a six-figure mistake.

Why Golf Carts Are Florida's Biggest Hidden Coverage Gap

No state lives on golf carts like Florida does. From The Villages and Lakewood Ranch to barrier-island beach towns and gated coastal communities, the cart is a second family vehicle. It carries kids to the pool, grandparents to the clubhouse, and groceries home from the corner store. And almost nobody insures it correctly.

The risk is not hypothetical. The U.S. sees roughly 15,000 golf-cart-related emergency-room visits a year, and Florida is the epicenter. The Villages alone was on pace to top 200 cart crashes in a single recent year. A 2025 pediatric study found golf-cart injuries among children and teens have climbed over the past decade, with falls and ejections — kids riding on laps, on running boards, or in laps without seat belts — driving nearly half of them. Summer, when school is out and a 15-year-old suddenly has the keys, is the worst stretch of the year. Hurricane season layers on a second exposure: a flooded or wind-tossed cart is a total loss that your homeowners policy may not touch.

The reason these losses turn into uncovered disasters is almost always the same — the owner assumed "the house policy has it." Let us walk through why that assumption fails, and what actually works.

Golf Cart vs. LSV vs. NEV: The Classification That Decides Everything

Before you can insure the machine, Florida law makes you classify it. Three terms get used loosely; only the legal definitions matter.

The Golf Cart (20 mph or less)

Under Florida Statutes § 320.01(22), a golf cart is a motor vehicle designed and manufactured for operation on a golf course and not capable of exceeding 20 miles per hour. A true golf cart has no VIN, is not titled, and is not registered with the state. Florida does not require you to insure it. That sounds like good news until you realize "not required" is not the same as "protected" — if your cart injures someone, you are personally liable whether or not you carry coverage.

The Low-Speed Vehicle (LSV / NEV)

Under § 320.01(42), a low-speed vehicle — sometimes called a neighborhood electric vehicle, or NEV — is any four-wheeled vehicle with a top speed greater than 20 but not more than 25 mph. Federal safety law (FMVSS No. 500, at 49 CFR 571.500) requires an LSV to carry real equipment: headlights, brake lights, turn signals, a parking brake, mirrors, a windshield, seat belts, and a 17-digit VIN. Because it has that VIN, Florida treats it as a motor vehicle. It must be titled, registered with the Florida Highway Safety and Motor Vehicles department (FLHSMV), and insured.

Why the Label Changes Your Whole Insurance Picture

Here is the part quoting engines bury: a "golf cart" you have upgraded — a lift kit, a bigger motor, a lithium battery swap — may now exceed 20 mph and has quietly become an LSV in the eyes of the law, even if the title still says golf cart and you never registered it. Drive that unregistered, uninsured LSV on a public road and you are operating an unregistered motor vehicle without insurance. After a crash, that is the first thing a plaintiff's attorney and your own carrier will check.

Why Your Homeowners Policy Probably Won't Pay

The single most expensive misunderstanding in Florida personal lines is the belief that a homeowners policy follows the cart everywhere.

How the "Residence Premises" Rule Limits Your Homeowners Policy

Standard homeowners forms (the HO-3 and the broader HO-5) exclude liability and physical-damage coverage for most motorized vehicles. Golf carts get a narrow carve-out: coverage typically applies only while the cart is used on an insured location (your property or, in some communities, the common areas you have an insurable interest in) or while it is being used to play golf on a golf course. Cross the street to a neighbor's driveway, run to the community mailbox, or take the kids to the pool down the road, and you have stepped outside that carve-out. If the cart hurts someone there, your homeowners liability can deny the claim outright.

Even on-premises, physical damage to the cart itself is often limited or excluded. A cart destroyed by hurricane flooding in your garage may be paid only up to a small sub-limit — or not at all — under your homeowners contents coverage. A dedicated golf cart policy with comprehensive coverage is what pays for storm, theft, and flood damage to the machine.

The Dangerous-Instrumentality Doctrine: Owner Beware

Florida is one of the few states that applies the dangerous-instrumentality doctrine to recreational vehicles, and courts have applied it to golf carts. In plain English: if you own the cart and you let someone else drive it — your teenager, a houseguest, your snowbird neighbor — you are vicariously liable for the harm they cause, even though you were nowhere near the crash. The injured party can come after your home equity, your savings, and your future wages. This is precisely the exposure a homeowners denial leaves wide open, and precisely why owners need real liability limits plus a personal umbrella sitting on top.

The golf-cart claim blindsides good Florida families more than almost any other I see — they lend the cart to a neighbor's teenager for ten minutes and learn, the hard way, that "the house policy has it" was never true once it left the driveway. Classify the machine, put it on the right policy form, and sit an umbrella on top. That structure costs a fraction of what a single ejection claim does.

— Ricardo Alonso, Founder, Atesa Risk Advisors

What Florida Law Actually Requires in 2026

Registration and the $10k / $10k Minimum for LSVs

If your machine is an LSV, § 316.2126, Florida Statutes, lets it operate on public roads with a posted speed limit of 35 mph or less, but only once it is titled, registered, and insured. The insurance floor is Florida's standard motor-vehicle minimum: $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). You will need proof of that coverage and a valid driver license to complete registration at the tax collector's office. A true under-20-mph golf cart needs none of this from the state — though many cities and gated communities impose their own insurance requirement as a condition of driving on community roads, so always check the local ordinance and HOA rules.

Age, ID, and the 2023 Law That Still Trips People Up

A 2023 Florida law (Chapter 2023-174, Laws of Florida) tightened who may drive a cart on public roads. Under § 316.2126 as amended, a person operating a golf cart on a public road must generally be 18 or older with a valid government-issued photo ID, or 15 with a learner's license, or 16 with a valid driver license — and must carry that credential while driving. Before the change, 14-year-olds could legally operate carts on public roads. The rule sounds simple, but two summers later, communities are still wrestling with enforcement, and parents who hand the keys to a 14-year-old are now both breaking the law and handing a plaintiff's attorney a gift.

How to Actually Insure It: Placement Is Where an Advisor Earns the Fee

This is the part an AI quote engine cannot do for you, because the right structure depends on the machine, how you use it, and what else you own.

Recreational Golf Cart Policy vs. Auto Policy

For a true golf cart, the right home is usually a recreational golf cart policy — a specialty product written by carriers such as Foremost, American Modern, Progressive, Safeco, or your homeowners insurer as an endorsement. These can offer liability, medical payments, comprehensive (storm, theft, flood, fire), collision, and even uninsured-motorist coverage for the cart. For an LSV, you generally need a personal auto policy, because the state requires PIP and PDL on a titled motor vehicle. Here is the friction point: many standard auto carriers will not write an LSV at all, so placement often moves to a specialty market. An advisor who knows which carriers accept LSVs — and which exclude them — saves you from buying a policy that quietly does not cover the vehicle you own.

Agreed Value, Custom Equipment, and Lithium Upgrades

Today's carts are not the bare-bones machines of a decade ago. Lifted suspensions, premium wheels, stereo systems, enclosures, and lithium-battery conversions routinely push a build to $15,000–$30,000 and beyond. If you insure that cart on an actual cash value (ACV) basis, a total loss pays the depreciated value — often a fraction of what you spent. The better structure for a high-value or custom build is agreed value (or stated value), where you and the carrier lock in the payout up front, the same way collectors insure classic cars. Documenting and scheduling those upgrades is a bespoke valuation exercise, not a checkbox — and getting it wrong only shows up at claim time.

Stacking Liability and Your Umbrella

If you own a home, a boat, or significant assets, the cart's liability limit should not be an afterthought. A personal umbrella can extend $1 million or more of liability over the cart — but only if the umbrella carrier accepts the exposure and you carry the required underlying liability limit on the cart or LSV first. Leave the cart uninsured, and the umbrella has nothing to sit on; it will not "drop down" to cover a vehicle you failed to schedule. Coordinating the cart, the auto policy, the homeowners policy, and the umbrella so they actually stack is the core of personal-lines placement.

The Claim Nobody Plans For

Picture a common Florida Saturday. A 16-year-old borrows the family LSV to pick up two friends. One rides on the back seat without a belt, the cart turns sharply, and the friend is ejected and seriously hurt. Now the questions come fast: Was the cart registered and insured? Was the driver legally licensed for it? Does the homeowners policy apply off-premises (usually no)? Does any auto policy respond? Because of the dangerous-instrumentality doctrine, the owner — the parents — face direct liability for medical bills that can run into six figures.

This is where claims advocacy, not a chatbot, decides the outcome. The right advisor knows which policy should respond first, pushes back when a carrier wrongly disclaims, coordinates PIP with the injured family's own coverage, manages the subrogation crossfire between carriers, and makes sure the umbrella is tendered correctly. The difference between a smooth payout and a personal financial catastrophe is often the human who built the program before the crash and fights for it afterward.

A Florida Cart Owner's Checklist Before You Ride This Summer

- Classify the machine. Confirm whether your vehicle tops out at 20 mph (golf cart) or 20–25 mph (LSV). Check for a 17-digit VIN — if it has one, it is an LSV and must be registered and insured.

- Read your homeowners policy's motor-vehicle exclusion. Find the golf-cart carve-out and note exactly where coverage stops. Assume off-premises liability is excluded unless your agent confirms otherwise in writing.

- Place a real policy. A recreational golf cart policy for under-20 carts; a personal auto policy meeting the $10k PIP / $10k PDL minimum for LSVs.

- Insure custom value at agreed value. Document lifts, lithium conversions, and accessories, and schedule them.

- Add comprehensive. Hurricane flood and wind, theft, and fire damage to the cart itself need physical-damage coverage — your homeowners policy likely will not pay.

- Set liability high and add an umbrella. Carry meaningful liability on the cart and confirm your personal umbrella extends over it.

- Lock down who drives. Enforce the age and license rules, require seat belts, and never let an unlicensed minor onto a public road.

A golf cart feels like a toy. Florida law, the courts, and the emergency rooms treat it like a vehicle. Insure it like one.

Related reading: Florida Personal Umbrella Insurance in 2026, Florida Parents' Complete Guide to Teen Driver Insurance, and What Your Florida Homeowners Policy Actually Covers.

Sources

[1] Florida Statutes § 320.01 — Definitions (golf cart and low-speed vehicle) [2] Florida Statutes § 316.2126 — Authorized use of golf carts, low-speed vehicles, and utility vehicles [3] Florida Statutes § 316.2125 — Operation of golf carts on certain roadways [4] Florida Highway Safety and Motor Vehicles (FLHSMV) — Registrations and Titles [5] NHTSA / Federal Motor Vehicle Safety Standard No. 500, Low-Speed Vehicles (49 CFR 571.500) [6] Florida Senate — HB 949 (2023), golf cart operation [7] Insurance Information Institute (Triple-I) — Recreational vehicle and specialty insurance [8] Florida Department of Financial Services — Consumer insurance resources

Frequently Asked Questions

Is golf cart insurance required in Florida? For a true golf cart that tops out at 20 mph and is not titled, the state does not require insurance. But many cities and HOAs require it to drive on community roads, and you are personally liable for any harm the cart causes — so coverage is strongly recommended.

Is LSV insurance required in Florida? Yes. A low-speed vehicle (20–25 mph) is a registered motor vehicle and must carry at least $10,000 PIP and $10,000 PDL, the same minimums as a car, before it can be titled and tagged.

Does my homeowners policy cover my golf cart? Generally only while the cart is on your residence premises or being used to play golf. Off-premises neighborhood use is typically excluded, and physical damage to the cart may be limited or uncovered.

What is the difference between a golf cart and an LSV in Florida? Speed and registration. A golf cart cannot exceed 20 mph and is not titled. An LSV exceeds 20 mph (up to 25), has a 17-digit VIN, and must be titled, registered, and insured.

Can I drive my golf cart on the road in Florida? Only where local rules allow, generally on roads posted 30 mph or less for golf carts and 35 mph or less for LSVs, and only if you meet the equipment, age, and (for LSVs) registration and insurance requirements.

How old do you have to be to drive a golf cart in Florida? Under the 2023 law, generally 18 with a valid government photo ID, 15 with a learner's license, or 16 with a valid driver license to operate on a public road — and you must carry that credential.

Who is liable if someone else crashes my golf cart? In Florida, the owner can be held vicariously liable under the dangerous-instrumentality doctrine, even if you were not driving and only lent the cart to a friend or family member.

Does golf cart insurance cover hurricane and flood damage? Only if you carry comprehensive (physical damage) coverage on a dedicated golf cart or LSV policy. Standard homeowners coverage rarely pays for storm or flood damage to a cart.

Should I insure a custom golf cart at agreed value or actual cash value? For lifted, lithium-converted, or high-dollar custom carts, agreed value protects your investment by locking in the payout. Actual cash value pays only depreciated value after a total loss.

Will my personal umbrella cover a golf cart accident? It can, but only if you carry the required underlying liability limit on the cart or LSV first. An umbrella will not drop down to cover an uninsured, unscheduled cart.

Do I need a separate policy for my LSV, or can I add it to my auto policy? An LSV is a motor vehicle, so it is usually insured on a personal auto policy. Many standard carriers decline LSVs, which is why placement often moves to a specialty market.

What happens if I upgraded my golf cart and it now goes faster than 20 mph? It may legally be an LSV, even if the title still says golf cart. Driving it unregistered and uninsured on a public road exposes you to citations and a denied claim after any crash.

Related Reading

- Florida Personal Umbrella Insurance in 2026: The Liability Shield That Protects Your Assets — the liability layer that can sit above a golf-cart claim.

- Florida Auto Insurance for High Earners: Why High-Net-Worth Families Need Maxed Limits and an Umbrella — limits strategy when a neighborhood crash gets expensive.

- Florida Auto Insurance: Understanding PIP, Bodily Injury, and What You Actually Need — how Florida auto coverage actually works.

How Atesa Risk Advisors Can Help

At Atesa Risk Advisors, golf cart and LSV coverage is exactly the kind of placement a quote engine cannot do for you. We start by classifying your machine — confirming whether it is a true under-20-mph golf cart or has quietly become an LSV — then match it to the right policy form: a recreational golf cart policy, or a personal auto policy meeting Florida's $10,000 PIP and $10,000 PDL minimum for an LSV. We know which specialty carriers actually accept LSVs and custom builds, schedule lifted and lithium-converted carts at agreed value so a total loss pays what you spent, and coordinate the cart, your auto, your homeowners, and a personal umbrella so the liability limits actually stack.

As an independent, RamseyTrusted brokerage, we work for you rather than a single carrier — and on a vehicle the dangerous-instrumentality doctrine ties directly to your personal assets, getting the structure right before a crash is the whole game.

Want your golf cart or LSV insured the right way before summer? Get a free coverage review and quote at atesariskadvisors.com/get-quote or call (904) 900-5063.

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. A Licensed 2-20 General Lines Agent with a Master of Liberal Arts in Finance from Harvard University and a background in construction, he helps Florida families place golf carts, LSVs, and the umbrella coverage that protects their assets when a neighborhood ride goes wrong.