Florida Auto Insurance for High Earners: Why High-Net-Worth Families Need Maxed Limits and an Umbrella

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 6, 2026

Key Takeaways

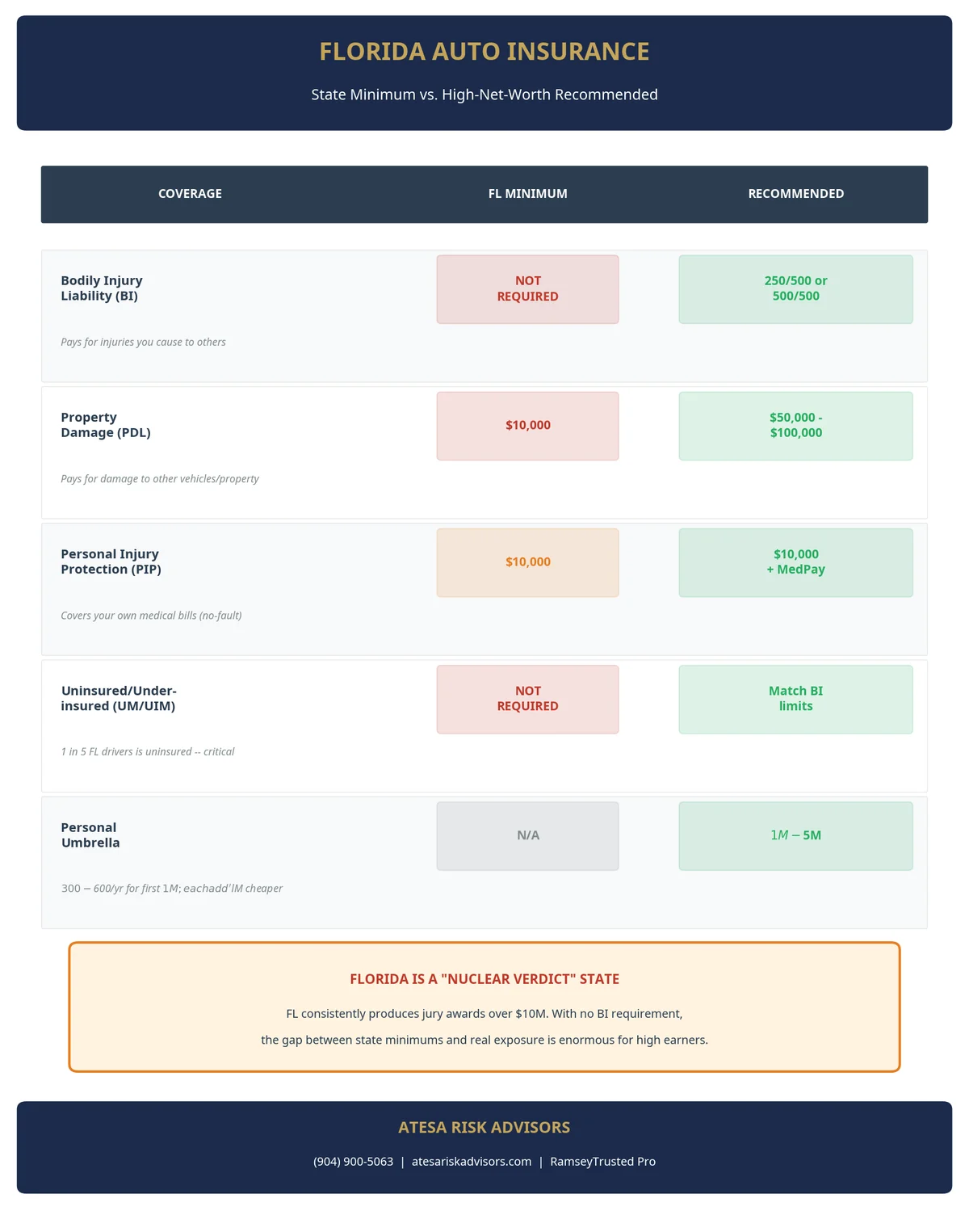

- Florida only requires $10,000 of Personal Injury Protection (PIP) — coverage for your own injuries — and $10,000 of property-damage liability, and it does not require any bodily-injury (BI) liability at all, the coverage that pays for injuries you cause to others. For a high earner, that is dangerously thin. [1][2]

- If you cause a serious crash, the injured party can pursue your non-exempt assets — brokerage and bank accounts, investment real estate — above your coverage. Your BI limit and umbrella are what stop the claim at the insurance company instead of your savings. [3]

- Florida law shields your home (unlimited homestead), head-of-family wages, and retirement accounts from a judgment — but not your liquid, non-retirement money. That liquid money is exactly what a lawsuit reaches first. [3][4][5][6]

- Florida is consistently among the states producing the most "nuclear verdicts" — jury awards over $10 million — so high limits matter more here than almost anywhere. [7]

- A personal umbrella adds $1M–$5M of liability over your auto and home for roughly $300–$600 a year for the first $1 million in Florida — pennies against what it protects. [8]

- Our rule: if you hold $250,000 or more in readily liquid assets, max out your auto liability limits and add an umbrella. Liquid money is what a judgment can reach fastest, and the cost to protect it is trivial.

If you are a high earner or hold significant assets in Florida, the state's minimum auto coverage leaves you badly exposed — and you should carry the highest bodily-injury limits your carrier offers plus a personal umbrella. Florida requires only $10,000 of Personal Injury Protection (PIP) and $10,000 of property-damage liability, and mandates no bodily-injury (BI) liability — the coverage that pays for the injuries you cause to other people — at all. [1][2] For someone with a six-figure income and a brokerage account, a single at-fault crash with serious injuries can produce a judgment that dwarfs those limits, and the gap comes straight out of your own pocket. This guide explains exactly why, and shares the simple liquid-asset rule we use to decide who needs to level up.

Here is the uncomfortable truth that plaintiffs' attorneys understand well: in a serious-injury case, the size of the claim is driven by the injuries and by what the at-fault driver can pay. If your assets are visible and reachable, you are a more attractive target — and a bigger settlement. The good news is that this exposure is cheap to close. The hard part is knowing whether it applies to you, which is what the rule below is for.

Why Florida Is Uniquely Dangerous for High-Asset Drivers

Three things stack up against a high earner in Florida:

1. The state requires almost no liability coverage. Florida is one of the only states that does not require drivers to carry bodily-injury liability. The mandatory minimum is $10,000 of PIP (which pays a slice of your own medical bills) and $10,000 of property damage. [1][2] Many Florida drivers carry exactly that — nothing for the injuries they cause others — which also means that when you are hit, there is often little coverage on the other side.

2. If you are at fault, you are personally on the hook above your limits. PIP does not protect you from a lawsuit. When you cause serious injuries, the injured party sues you directly, and any judgment above your auto BI limit becomes your personal responsibility.

3. Florida's verdict climate is among the harshest in the country. Insurance researchers use the term "nuclear verdict" for a jury award above $10 million. Driven by "social inflation" — the trend of juries awarding ever-larger sums for pain and suffering — these awards have climbed sharply, and Florida is consistently one of the states that produces the most of them. [7] The 2023 tort-reform law (HB 837) tightened some lawsuit rules, but it did not cap the damages a sympathetic, badly-injured plaintiff can win.

Add in that roughly 1 in 5 Florida drivers is uninsured [8], and the picture is clear: high limits are not optional insurance-nerd advice here — they are basic asset protection.

What Florida Requires vs. What a High Earner Should Carry

| Coverage | Florida minimum | Recommended for high earners |

|---|---|---|

| Bodily Injury (BI) liability | Not required | 250/500, then 500/500, with an umbrella on top |

| Property Damage (PDL) | $10,000 | $50,000–$100,000 |

| Personal Injury Protection (PIP) | $10,000 | $10,000 (consider adding MedPay) |

| Uninsured/Underinsured Motorist (UM/UIM) | Not required (must be offered) | Match your BI limits, plus excess UM via the umbrella |

| Personal umbrella | — | $1M floor; $2M–$5M for most high-net-worth families |

"250/500" means $250,000 of injury coverage per person and $500,000 per accident. UM/UIM (uninsured/underinsured motorist) is the coverage that pays you when the at-fault driver has no insurance or not enough — critical in a state with so many uninsured drivers.

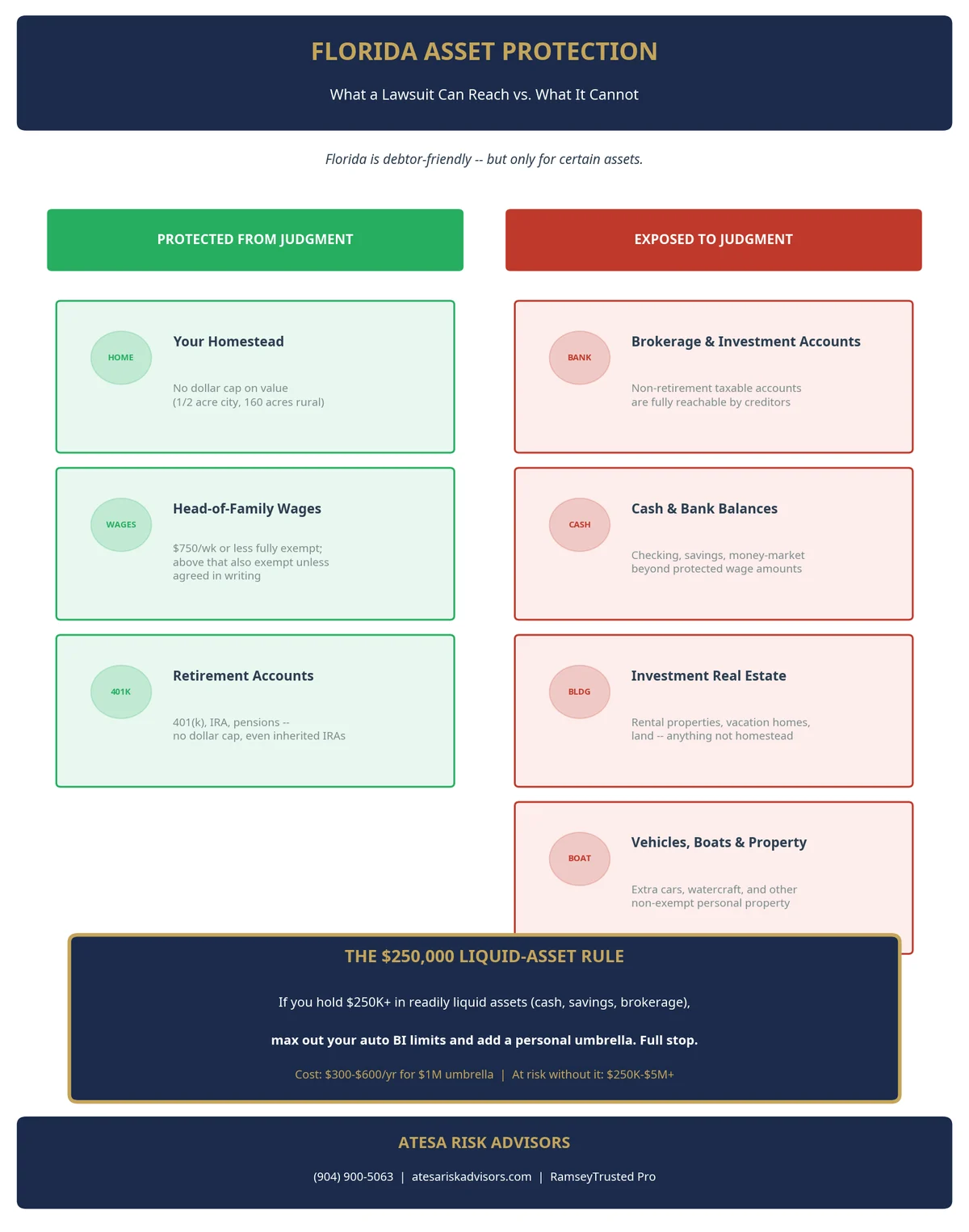

What a Lawsuit Can Actually Reach in Florida (and What It Can't)

This is the part most people get wrong, and it is the heart of how we think about limits. Florida is famously debtor-friendly — but only for certain assets.

Generally protected from a judgment:

- Your home. Florida's homestead protection has no dollar cap on value (up to ½ acre in a city, 160 acres outside one). A creditor generally cannot force its sale. [3][6]

- Head-of-family wages. If you provide more than half the support for a dependent, your disposable wages of $750/week or less are fully exempt, and amounts above that are exempt unless you agreed otherwise in writing. [4]

- Retirement accounts. 401(k)s, IRAs, and pensions are protected with no dollar cap under Florida law — even inherited IRAs. [5]

Generally exposed to a judgment:

- Non-retirement brokerage and investment accounts.

- Cash and bank balances beyond the protected wage amounts.

- Investment and rental real estate (anything that is not your homestead).

- Extra vehicles, boats, and other non-exempt personal property. [3]

See the pattern? The Florida assets a court can reach are your liquid, non-retirement assets — the very money you have worked to build outside your house and 401(k). That is the bucket an auto liability limit and an umbrella exist to protect.

Our Rule: The $250,000 Liquid-Asset Trigger

After years of placing coverage for Florida families, here is the simplest decision rule we use, and the one we will give you straight:

If you hold $250,000 or more in readily liquid assets, you should max out your auto bodily-injury limits and add a personal umbrella — full stop.

By "readily liquid" we mean money you could convert to cash quickly: checking and savings, money-market funds, taxable brokerage accounts, and similar holdings. We deliberately exclude your homestead and retirement accounts from the count, because Florida already protects those. The question the rule answers is not "how rich are you?" — it is "how much reachable money would a judgment find?"

Why $250,000? Two reasons. First, it is the level at which you have real, exposed wealth that a plaintiff's attorney will pursue. Second, the cost of fixing the exposure is trivial in comparison — raising BI limits and adding a $1–2 million umbrella typically costs a few hundred dollars a year, against hundreds of thousands at risk. Below that threshold the math is closer; at or above it, going without maxed limits is one of the worst risk-for-dollar trades in personal finance.

A high income is its own flag, too. If you earn well into six figures, you are an attractive target even before the assets accumulate — and future earnings can be pursued in some circumstances. When income is high, we apply the same rule even if the liquid balance has not caught up yet.

In twenty years of writing Florida policies, I have never seen a client regret carrying too much liability coverage — but I have sat across from people who carried the state minimum and watched a single crash threaten everything they had built outside their home and 401(k). If you have a quarter-million dollars in reachable money, the umbrella is not a luxury. It is the cheapest peace of mind you will ever buy.

— Ricardo Alonso, Founder, Atesa Risk Advisors

How Much Umbrella Do You Actually Need?

A personal umbrella is extra liability coverage that sits on top of your auto and home policies; when a claim blows past those limits, the umbrella keeps paying — commonly in $1 million increments up to $5 million or more.

The working rule of thumb: carry umbrella limits at least equal to your net worth, and ideally net worth plus a few years of income. For most high-net-worth Florida families, $1 million is a floor, not a target; $2–5 million is common once you factor in a coastal home, a boat, or a teen driver. The marginal cost of each additional million is low — the second and third million cost far less than the first — so layering up is usually a bargain. [8]

Do not overlook excess UM/UIM on the umbrella. In a state where about 1 in 5 drivers is uninsured, this is the coverage that protects you and your family when someone with no insurance causes the crash. In Florida it must be offered and can only be reduced or rejected in writing, and high earners reject it by accident more often than you would think. [8]

A Florida Example: How a $1.2M Verdict Finds Your Brokerage Account

Picture a Jacksonville couple earning a combined $300,000, with a paid-off home (protected) and about $450,000 in a taxable brokerage account (exposed). Their auto policy carries 250/500 — better than most. One afternoon, a driver causes a multi-car crash that seriously injures two people.

A jury returns a $1.2 million verdict. The auto policy pays its $500,000 per-accident maximum and stops, leaving $700,000 unpaid. The home and any retirement accounts are shielded — but the $450,000 brokerage account is not, and a wage and asset pursuit can follow for the balance. The financial plan they spent a decade building is gutted.

Now run it again with a $2 million umbrella in place. The auto policy pays $500,000, the umbrella absorbs the $700,000, and the brokerage account is never touched. The annual cost of that umbrella was a few hundred dollars. That is the entire argument in one example.

Why High-Net-Worth Placement Takes a Human, Not a Quote Bot

Here is where an online quote engine fails an affluent family. Maxing out limits, coordinating an umbrella over multiple homes and vehicles, scheduling a boat, adding a teen driver, and keeping excess UM intact is exactly the kind of profile that standard carriers decline or misprice. A licensed advisor moves these accounts to high-net-worth markets built for them — Chubb, PURE, Cincinnati, Berkley One — that an algorithm never surfaces. The cheapest online quote is often the one that quietly stripped out the UM coverage or set the underlying limits too low for the umbrella to attach. For a high-asset household, that is precisely the wrong place to save $40 a year.

Florida-Specific Considerations

- Fla. Stat. § 627.736 sets the PIP (no-fault) requirement — still $10,000 in 2026. [1]

- Florida's financial-responsibility law requires $10,000 of property-damage liability but no bodily-injury liability for most drivers. [2]

- Fla. Stat. § 627.727 requires carriers to offer uninsured/underinsured motorist coverage; you can only reduce or reject it in writing.

- HB 837 (2023) reformed how injury lawsuits work but did not cap the damages a plaintiff can recover.

- Asset protection: the homestead (Fla. Const. Art. X, § 4) [6], head-of-family wages (§ 222.11) [4], and retirement accounts (§ 222.21) [5] are shielded; liquid, non-retirement assets are not. [3]

Your 5-Step High-Net-Worth Auto Review

- Tally your reachable money. Add up cash, savings, money-market, and taxable brokerage balances — not your home or retirement. If it is $250,000 or more, the rest of this list applies to you.

- Pull your auto declarations page. Find your current bodily-injury (BI) and uninsured-motorist (UM/UIM) limits. State-minimum or 100/300 is too low for this profile.

- Raise BI to 250/500 or 500/500 and match your UM/UIM. This is the foundation the umbrella sits on — and it is exactly the underlying limit an umbrella carrier requires before it will attach.

- Add or raise a personal umbrella to at least your net worth. Start at $1 million; layer to $2–5 million — the extra millions are inexpensive.

- Place it with a high-net-worth carrier and review annually. Re-check after every major change: a new home, a new boat, a new teen driver, a jump in assets.

FAQ for High-Net-Worth Florida Drivers

How much auto insurance should a high earner in Florida carry? At least 250/500 bodily-injury liability (many high earners go to 500/500), matching uninsured-motorist limits, and a personal umbrella of $1 million or more. Florida's $10,000 minimums are far too low for anyone with assets or income to protect. [1][2]

Does Florida require bodily-injury liability? No. Florida requires only $10,000 of PIP and $10,000 of property-damage liability. Bodily-injury liability — the coverage that pays for injuries you cause others — is not mandated, which is exactly why high earners must add it voluntarily at high limits. [1][2]

What assets can a lawsuit actually take in Florida? Generally, your non-retirement brokerage and bank accounts, investment real estate, and extra vehicles. Your homestead, head-of-family wages, and retirement accounts are generally protected. [3][4][5][6]

I have $250,000 in a brokerage account — do I really need an umbrella? By our rule, yes. That brokerage balance is reachable by a judgment, and an umbrella that protects it costs only a few hundred dollars a year. It is one of the highest-leverage moves in personal finance. [8]

How much does a $1–5 million umbrella cost in Florida? The first $1 million typically runs about $300–$600 a year in Florida, and each additional million costs far less than the first. [8]

Is my home or retirement account at risk in a car-accident lawsuit? Generally no. Florida's unlimited homestead protection and its retirement-account exemptions shield those assets from most judgments. The exposure is your liquid, non-retirement money. [3][5][6]

What is excess UM/UIM and why does it matter for high earners? Uninsured/underinsured motorist coverage pays you when the at-fault driver has no insurance or too little. With roughly 1 in 5 Florida drivers uninsured, a high earner's own UM/UIM — extended by the umbrella — is often the only thing that fully covers a serious injury caused by an underinsured driver. [8]

Can I rely on my income being protected from garnishment? Only partly. Florida's head-of-family wage protection is strong, but it does not cover everyone, money loses protection once it is commingled in accounts over time, and — most importantly — your liquid investments are fully exposed. Do not treat wage protection as a substitute for adequate limits. [3][4]

Related Reading

- Florida Auto Insurance: PIP, Bodily Injury, and What You Actually Need — the coverage architecture behind these recommendations.

- Florida Personal Umbrella Insurance in 2026 — a deeper look at how umbrellas work, what they cost, and how to place them.

How Atesa Risk Advisors Can Help

At Atesa Risk Advisors, building coverage for high earners and high-net-worth families is core to what we do. We tally your real exposure, raise your auto liability and uninsured-motorist limits to where they belong, and coordinate a personal umbrella across your home, autos, and watercraft — placed with carriers built for affluent households, not the cheapest online quote. We will tell you plainly whether our $250,000 liquid-asset rule applies to you, and exactly how little it costs to close the gap.

Want to know if your limits actually protect what you have built? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Florida Statutes § 627.736 — Personal Injury Protection (no-fault)

[2] Florida Department of Highway Safety and Motor Vehicles — Insurance Requirements

[3] The Florida Bar — Consumer Pamphlet: Debtors' Rights in Florida

[4] Florida Statutes § 222.11 — Exemption of Wages from Garnishment

[5] Florida Statutes § 222.21 — Exemption of Pension and Retirement Accounts

[6] Florida Constitution, Article X, Section 4 — Homestead Protection

[7] Insurance Information Institute (Triple-I) — Background on Social Inflation

[8] Insurance Information Institute (Triple-I) — Understanding Umbrella / Excess Liability Insurance

External Resources for high-net-worth Florida households:

- Florida Statutes, Chapter 222 — Homestead and Exemptions

- Insurance Information Institute — Auto Insurance Basics

*Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. He helps Florida high earners and high-net-worth families align their insurance limits with the assets and income they actually need to protect.