Florida Personal Umbrella Insurance in 2026: The Liability Shield That Protects Your Assets

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 6, 2026

Key Takeaways

- A personal umbrella policy is extra liability coverage that sits on top of your home and auto policies — when a lawsuit blows past those limits, the umbrella pays the rest, up to $1 million, $5 million, or more.

- Florida is one of the few states that does not require Bodily Injury (BI) liability, so many drivers carry little or none. When you cause a crash, the injured party can sue you for their medical bills and pain and suffering — and your $10,000 PIP will not shield your assets; your liability and umbrella limits will.

- Florida is one of only four states that together produce more than half of the nation's "nuclear verdicts" (jury awards over $10 million). Awards above $10 million rose roughly 52% in 2024, and the average has climbed past $51 million.

- Most carriers require underlying limits of about 250/500 on auto and $300,000 on home liability before they will sell you an umbrella — meeting those minimums is the first hurdle, not the last.

- The most overlooked feature is excess uninsured/underinsured motorist (UM/UIM) coverage — vital in a state where roughly 1 in 5 drivers is uninsured. In Florida it must be offered and rejected in writing, and many buyers reject it by accident.

- High-value coastal households with boats, jet skis, teen drivers, pools, or a rental condo are exactly the risks that automated quoting engines decline — placement here takes a human who knows which carriers will say yes.

- In Florida, the first $1 million of umbrella coverage typically runs $300 to $600 a year; layering to $5 million is far cheaper per million than most people assume.

A personal umbrella policy is excess liability insurance that pays after your home and auto liability limits are exhausted, protecting your savings, home equity, and future wages from a large lawsuit. It is especially important in Florida, where drivers are not required to carry Bodily Injury liability, an at-fault driver is personally liable for the injuries they cause, and the legal climate produces some of the largest jury verdicts in the country.

What a Personal Umbrella Policy Actually Does

Think of your insurance as stacked layers. Your auto policy and your homeowners policy each include "liability" coverage — the part that pays when you are legally responsible for hurting someone or damaging their property. But those layers have ceilings. A typical Florida auto policy might cap bodily injury liability at $100,000 or $250,000 per person. A homeowners policy might cap personal liability at $300,000 or $500,000.

A personal umbrella policy is a separate layer that sits above all of those. When a covered claim exhausts the underlying limit, the umbrella picks up where that policy stops and keeps paying — commonly up to $1 million, and in $1 million increments up to $5 million or more for high-net-worth households. It also covers some liability your base policies exclude entirely, such as libel, slander, and false arrest.

Here is the part most buyers miss: an umbrella is not just for the wealthy, but the wealthy cannot do without it. The reason is simple math. If a jury awards $900,000 against you and your auto policy stops at $250,000, the remaining $650,000 comes from you — your bank accounts, your home equity above Florida's homestead protection, and a court-ordered garnishment of your future wages. The umbrella exists to make that number stop at the insurance company.

Why Florida''s Liability Math Demands an Umbrella

Most people assume Florida requires drivers to cover the injuries they cause. It does not. Florida''s mandatory auto minimum is just $10,000 of Personal Injury Protection (PIP) — which pays a slice of your own medical bills — plus $10,000 of property damage. The state does not require Bodily Injury (BI) liability at all, so a large share of Florida drivers carry little or none. PIP has faced repeated repeal proposals (SB 54 was vetoed in 2021; SB 522 and HB 769 died in committee in 2026), but as of 2026 it remains the law under Fla. Stat. § 627.736. [1]

Here is why that matters for your assets: PIP only ever covers a sliver of your own bills. If you are the at-fault driver, the injured party can sue you directly for their medical bills, lost wages, and pain and suffering. Florida''s modified-comparative-negligence rule from the 2023 tort-reform law (HB 837) means a plaintiff who is less than 51% at fault can still recover from you. [2][3]

And the limits most drivers carry are dangerously thin. Even those who buy BI often carry just 10/20 or 25/50 — and a single ambulance ride, surgery, and a few months of physical therapy can blow through $25,000 before lunch. Whatever a verdict exceeds your auto BI limit is your personal problem: your savings, your home equity above Florida''s homestead protection, and a garnishment of your future wages. That is precisely the gap a personal umbrella is built to close. If you have not revisited your auto liability limits recently, raise those first, then come back here for the excess layer.

Florida Is Ground Zero for Nuclear Verdicts

There is a reason Florida liability is expensive: the verdicts are enormous. Insurance analysts use the term "nuclear verdict" for a jury award exceeding $10 million. Nationally, the number of nuclear verdicts rose roughly 52% in 2024, awards above $100 million surged more than 80%, and the average nuclear verdict now exceeds $51 million. Critically, more than half of the country's nuclear verdicts come from just four states — and Florida is one of them. [4]

The driver is "social inflation" — the tendency of juries to award ever-larger sums for pain and suffering, fueled by litigation tactics that anchor jurors to seven- and eight-figure numbers. For a Florida family, the takeaway is not abstract. A car crash, a guest injured at your pool, a dog bite, or a teenager's mistake behind the wheel can become a claim that a $300,000 home-liability limit cannot begin to absorb. Tort reform has helped tamp down questionable claims and even lowered some auto rates, but it did not cap the damages a sympathetic plaintiff can win. The exposure is still there; the umbrella is still the answer.

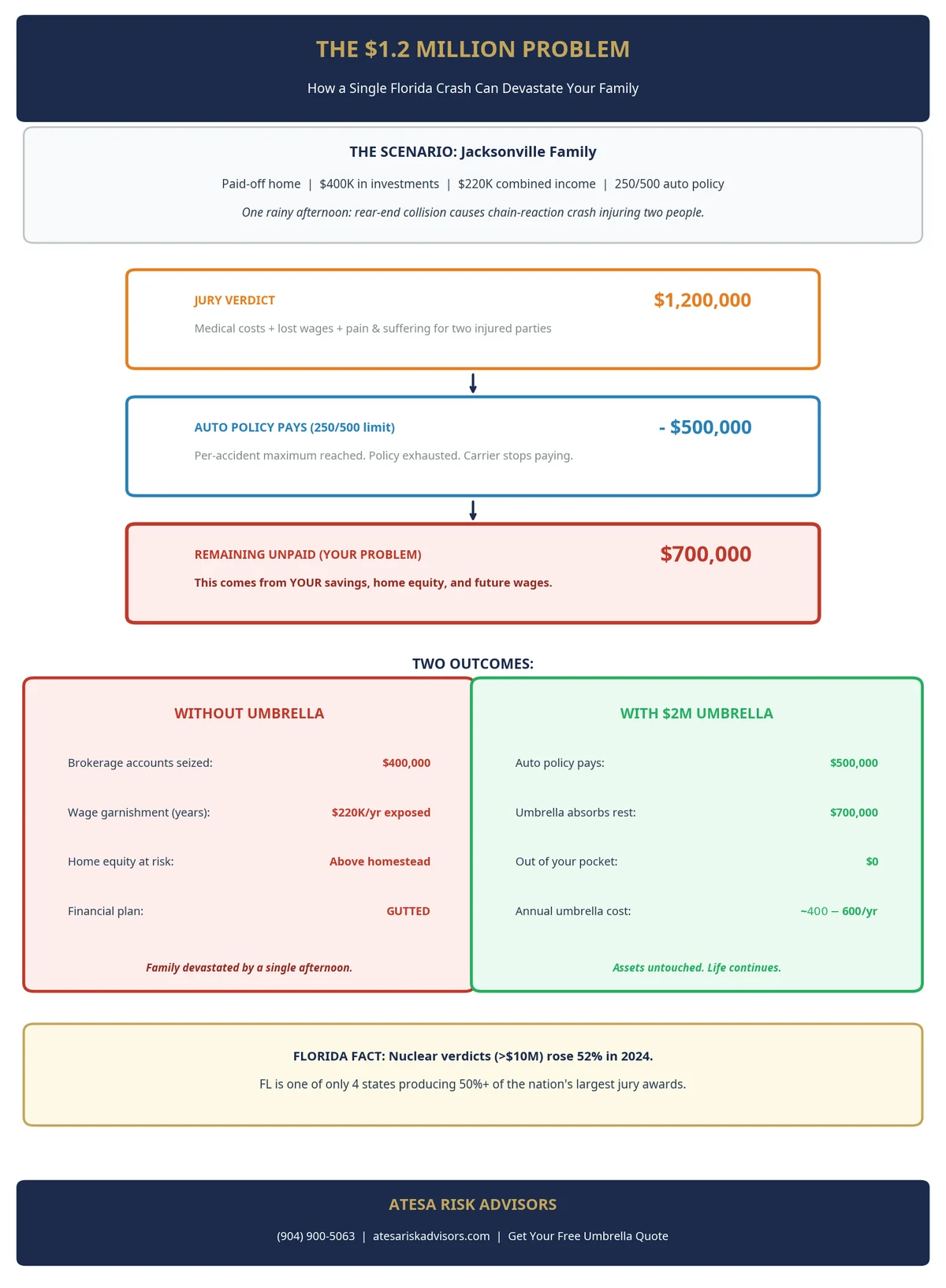

A Florida Example: How $250,000 Becomes a $1.2 Million Problem

Picture a Jacksonville household with a paid-off home, about $400,000 in retirement and brokerage accounts, and two earners pulling a combined $220,000 a year. Their auto policy carries 250/500 bodily injury — better than most. One rainy afternoon on the way home, a driver rear-ends a stopped car, causing a chain-reaction crash that seriously injures two people.

A jury finds our driver at fault and awards $1.2 million in combined medical costs, lost wages, and pain and suffering. The auto policy pays its $500,000 per-accident maximum and stops. That leaves $700,000 unpaid. Without an umbrella, the plaintiffs' attorney goes after the brokerage accounts and secures a wage garnishment that follows both earners for years; the family's financial plan is gutted by a single afternoon.

Now run the same crash with a $2 million umbrella in place. The auto policy pays its $500,000, the umbrella absorbs the remaining $700,000, and the family's assets and paychecks are untouched. The annual cost of that umbrella? A few hundred dollars. That is the entire value proposition in one example — and in Florida's high-verdict legal climate, this scenario is more common than most families realize.

The Coverage That Surprises People: Excess UM/UIM

Here is the feature that separates a thoughtfully placed umbrella from one bought on price: excess uninsured/underinsured motorist (UM/UIM) coverage.

UM/UIM protects you when the at-fault driver has no insurance or not enough. In Florida — where roughly one in five drivers is uninsured and the state does not even require Bodily Injury liability — this is not a remote risk. If a driver with no coverage puts you in the hospital, your own UM/UIM is the only policy that pays your medical bills, lost income, and pain and suffering. An umbrella can extend that protection by an extra $1 million or more.

The catch is statutory. Under Florida Statute 627.727, UM/UIM coverage must be offered, and you can only reduce or reject it by signing a written waiver. [2] Many buyers reject excess UM on the umbrella without realizing it, chasing a slightly lower premium — and then discover the gap only after a crash with an uninsured driver. A human advisor's job is to make sure that decision is deliberate, in writing, and understood. This is also why generic online umbrella quotes are risky: the cheapest quote is often the one that quietly stripped out the coverage you most need in Florida.

How Much Umbrella Coverage Do You Need?

The rule of thumb is to carry umbrella limits at least equal to your net worth, and ideally to your net worth plus a few years of future income, because a judgment can attach to wages you have not yet earned. You can put real numbers to this in about two minutes with our umbrella coverage calculator, which turns your assets, future income, and risk factors into a recommended limit. But net worth is only the starting point. The better question is: how large is the claim a jury could realistically assign to you? That depends on your exposures, not just your balance sheet.

Use this as a working framework:

- Tally your at-risk assets. Home equity above Florida's homestead exemption, investment and bank accounts, rental properties, and non-qualified investments are all reachable by a judgment.

- Add your future income. A garnishment can follow a high earner for years.

- Weight your exposures. A household with a teen driver, a boat, a pool, a dog, and a short-term rental has a far higher frequency of liability events than a retired couple with one sedan.

For most Florida professionals, $1 million is a floor, not a target. Households with significant assets, a coastal second home, or watercraft commonly carry $3 million to $5 million, and ultra-high-net-worth families layer to $10 million-plus through specialty carriers. The good news, covered next, is that the marginal cost of each additional million is low.

What an Umbrella Costs in Florida

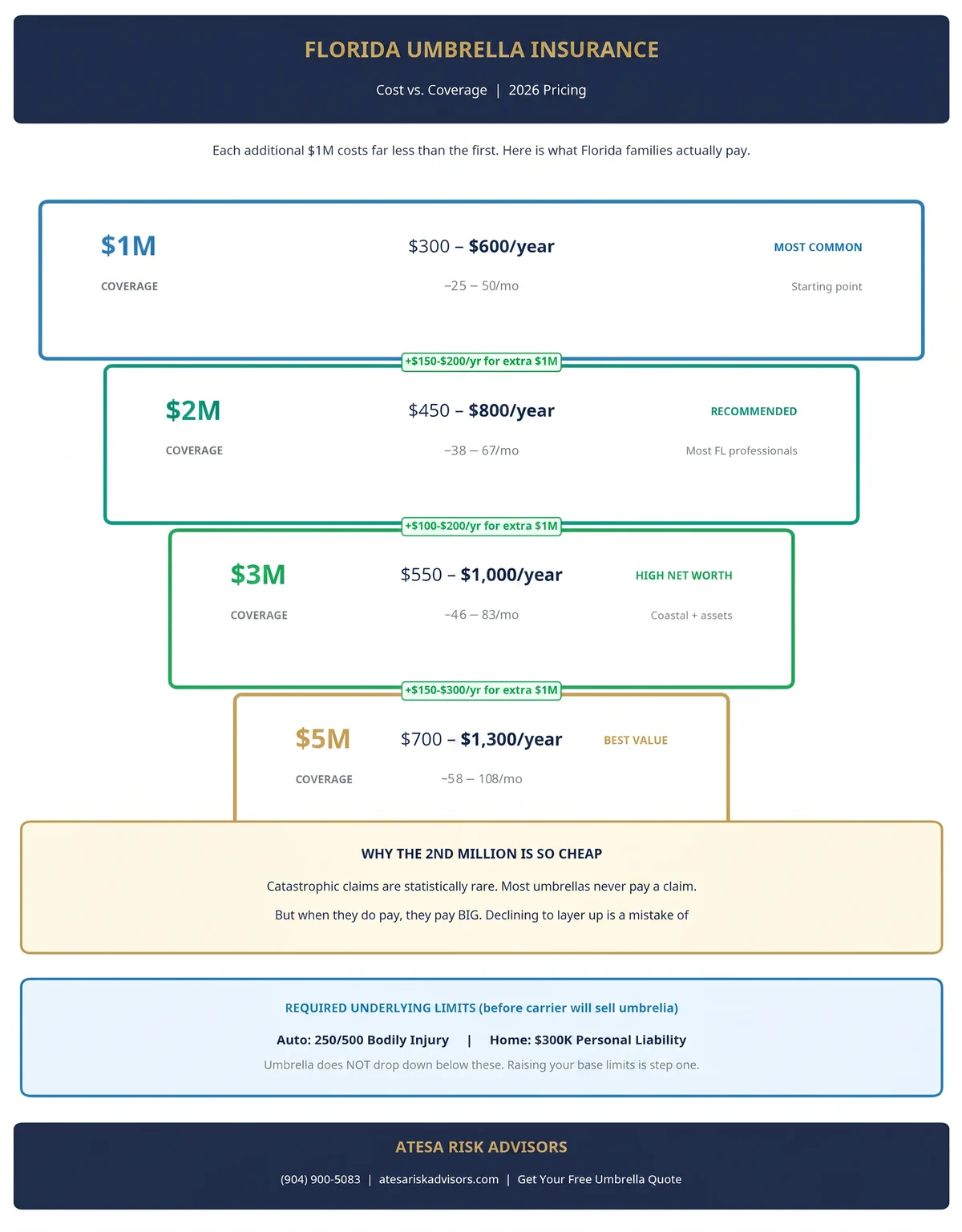

Umbrella insurance is one of the best values in personal insurance — we ran the 2026 cost math to prove it. Nationally, the Insurance Information Institute and major carriers put the first $1 million at roughly $200 to $400 a year, with each additional million adding far less than the first. [5] In Florida, expect the first $1 million to run closer to $300 to $600 because of the litigation climate, with higher figures for households that carry the exposures underwriters worry about.

Why is the second and third million so cheap? Because catastrophic claims are statistically rare — most umbrellas never pay — but when they do pay, they pay big. A family carrying $5 million of coverage often pays only a few hundred dollars more than one carrying $1 million. For high-net-worth households, declining to layer up is usually a mistake of pennies guarding against dollars.

The Underlying-Limits Trap

Before a carrier will sell you an umbrella, it requires you to carry minimum underlying limits on the policies beneath it — typically 250/500 of bodily injury on auto and $300,000 of personal liability on home, sometimes $500,000. [5] We map out the exact underlying limits carriers require, and the gap most Florida drivers have in a companion guide. The umbrella does not "drop down" to fill a gap below those limits; if you carry less than required and a claim lands, you are responsible for the shortfall between your actual limit and the required attachment point. Raising your auto and home liability to meet the umbrella's requirements is part of the placement — and it is one more reason a coordinated advisor beats a piecemeal online purchase.

Who Gets Declined — and Why Placement Is Hard

This is where automated quoting engines fall apart and a human advisor earns their fee. Personal umbrella underwriting is exposure-driven, and the exact features that define an affluent Florida household are the ones standard carriers decline:

- Watercraft. Boats, especially fast or large vessels, and personal watercraft (jet skis) trigger declinations or require the umbrella to schedule the vessel and confirm a primary marine-liability layer. Many standard markets simply will not extend umbrella over a 38-foot center console.

- Young or newly licensed drivers. A teen in the household — a real liability magnet under the new at-fault regime — can knock a family out of a preferred carrier's appetite.

- Pools, trampolines, and dogs. "Attractive nuisances" and certain dog breeds are classic decline or surcharge triggers.

- Rental and short-term-rental units. Owning a second home you rent on Airbnb is a commercial-flavored exposure that a personal umbrella may exclude unless specifically endorsed.

- Multiple homes and high coastal values. A coastal second home placed in the surplus-lines (non-admitted) market, or carried with Citizens, complicates the underlying-limits math an umbrella depends on.

When a standard carrier declines, an experienced advisor moves the risk to specialty and high-net-worth markets — Chubb, PURE, Cincinnati, Berkley One, RLI — that are built for exactly these exposures, and in some cases to the surplus-lines market for the highest limits. A quoting algorithm returns "no eligible carriers." A human gets the family covered. That is the core reason this coverage resists commoditization.

Where Umbrella Fits in the High-Value Coastal Bundle

For an affluent Florida household, the umbrella is the keystone of a larger, deliberately built personal program — not a standalone afterthought. The pieces work together:

- An HO-5 or agreed-value homeowners policy on the primary residence, so the home itself is insured on the broadest, most generous terms rather than a basic actual-cash-value form. (Start with what your Florida homeowners policy actually covers.)

- Scheduled valuables — a "valuable articles" floater that individually lists jewelry, art, watches, fine wine, and firearms with agreed values and worldwide, all-risk coverage, including the "mysterious disappearance" a homeowners policy excludes.

- The umbrella stretching liability protection across the home, the autos, the watercraft, and the rental units in one coordinated limit.

If your primary home is carried with Citizens or was recently taken out by a private carrier, the bundle gets more complex, and coordinating the underlying liability limits across admitted and surplus-lines policies becomes genuinely technical work. NOAA forecasts a below-normal 2026 Atlantic hurricane season, but liability does not take a hurricane off — pool gatherings, dock guests, and boat outings peak in exactly the months a coastal family is most exposed. [6]

How to Buy the Right Umbrella in Florida

- Inventory your at-risk assets and future income. Set a target limit at or above net worth plus a buffer for wages.

- Pull your current auto and home declarations pages. Confirm your bodily-injury and personal-liability limits and identify whether they already meet umbrella underlying requirements (commonly 250/500 auto, $300,000 home).

- Raise underlying limits if needed. Bring auto and home liability up to the attachment point before binding the umbrella.

- List every exposure honestly. Boats, jet skis, teen drivers, pools, dogs, rental units, and second homes — disclosure now prevents a denied claim later.

- Demand excess UM/UIM — or reject it in writing knowingly. In Florida this protects you from the state's many uninsured drivers; do not let it be silently dropped. [2]

- Match the household to the right carrier. Standard for simple risks; high-net-worth or surplus-lines markets for watercraft, multiple homes, and high limits.

- Layer to $3M–$5M and compare the marginal cost. The extra millions are usually inexpensive.

- Review annually and after every life change — a new driver, a new boat, a new rental — so the limit keeps pace with the exposure.

Claims Advocacy: Why a Human Matters When the Lawsuit Lands

Buying the umbrella is the easy half. The hard half is the day a process server hands you a lawsuit. Umbrella claims are, by definition, the large and contested ones — the cases where the plaintiff's attorney is anchoring a jury to a number with a comma in it.

In those moments, an independent advisor coordinates the layers: confirming the auto or home carrier defends and pays to its limit first, then triggering the umbrella, and making sure the two insurers do not point fingers while the clock runs. The advisor pushes for a defense before the underlying limit is exhausted, documents the exposure, and keeps the family informed of settlement dynamics that a policyholder navigating alone would never see coming. (For why an independent advocate matters across every line, see what an independent insurance agent does.) Against a Florida jury and a sophisticated plaintiff's bar, that advocacy is not a luxury — it is the difference between a claim that ends at the policy limit and one that reaches your assets.

Related Reading

- Florida Auto Insurance for High Earners: Maxed Limits & an Umbrella — Why high-net-worth families need high bodily-injury limits and an umbrella, plus the $250K liquid-asset rule.

Frequently Asked Questions

Do I really need umbrella insurance if I'm not wealthy? Yes, if you have any assets or future income to protect. Florida's large jury verdicts — and the fact that many drivers carry little or no bodily injury liability — mean a single at-fault crash can produce a judgment far above your auto limits. Wages can be garnished even if your bank account is modest.

How is umbrella insurance different from my homeowners liability? Homeowners liability covers incidents tied mostly to your property and personal activities, up to a fixed limit. An umbrella sits above both your home and auto liability, raises the ceiling by $1 million or more, and covers some claims (like libel and slander) your base policies exclude.

Why is a personal umbrella especially important in Florida? Because Florida does not require Bodily Injury liability, many drivers carry little or none — yet an at-fault driver is personally liable for the injuries they cause. Combined with one of the nation's most active litigation climates and largest jury verdicts, that makes your liability and umbrella limits — not your $10,000 PIP — what actually protect your assets. [1]

What underlying limits do I need before I can buy an umbrella? Most carriers require roughly 250/500 of auto bodily injury and $300,000 (sometimes $500,000) of home personal liability. You may need to raise your base limits first. [5]

What is excess UM/UIM and should I keep it? Excess uninsured/underinsured motorist coverage pays you when an at-fault driver has no insurance or too little. In Florida, where about 1 in 5 drivers is uninsured, most advisors strongly recommend keeping it. It must be rejected in writing under Florida Statute 627.727. [2]

How much umbrella coverage should I carry? At minimum, enough to cover your net worth, and ideally net worth plus several years of income. Households with boats, second homes, or teen drivers often carry $3 million to $5 million.

How much does umbrella insurance cost in Florida? The first $1 million typically runs about $300 to $600 a year in Florida, with each additional million costing far less than the first. [5]

Will an umbrella cover my boat or jet ski? Sometimes, but watercraft must usually be disclosed and may require the umbrella to sit over a primary marine-liability policy. Larger or faster vessels can cause standard carriers to decline, which is when specialty placement matters.

Does umbrella insurance cover my short-term rental or Airbnb? Not automatically. Rental and short-term-rental activity is often excluded from a personal umbrella unless specifically endorsed, because it carries a commercial flavor. The exposure must be disclosed and arranged deliberately.

Why was I declined for an umbrella? Common triggers include teen drivers, large or fast boats, pools or trampolines, certain dog breeds, multiple homes, and rental units. A declination from a standard carrier usually means the risk belongs in a high-net-worth or surplus-lines market, not that you are uninsurable.

Does my umbrella defend me in a lawsuit, or just pay damages? Most umbrellas provide a legal defense for covered claims, often in addition to the policy limit, which is a major benefit when a plaintiff's attorney is pursuing a large award.

Can I buy an umbrella from a different company than my home and auto? You can, but it is harder and riskier. A "stand-alone" umbrella requires careful coordination of underlying limits across carriers. Most buyers are better served keeping the umbrella with — or carefully matched to — the underlying policies, which an advisor manages for you.

Sources

[1] Florida Statutes § 627.736 — Personal Injury Protection (no-fault), current 2026 — PIP remains required; repeal proposals (SB 54, vetoed 2021; SB 522 / HB 769, died in committee 2026) have not become law.

[2] Florida Statutes § 627.727 — Uninsured/Underinsured Motorist Coverage (Online Sunshine)

[3] Florida Statutes § 768.81 — Comparative Fault (Online Sunshine)

[4] Insurance Information Institute (Triple-I) — Background on Social Inflation

[5] Insurance Information Institute (Triple-I) — Understanding Umbrella / Excess Liability Insurance

[6] NOAA — 2026 Atlantic Hurricane Season Outlook

[7] Florida Department of Highway Safety and Motor Vehicles — Insurance Requirements