Florida EV Commercial Fleet Insurance 2026: The Saltwater Battery-Fire Gap Standard Auto Policies Miss

By Ricardo Alonso, Founder, Atesa Risk Advisors · June 25, 2026

Key Takeaways

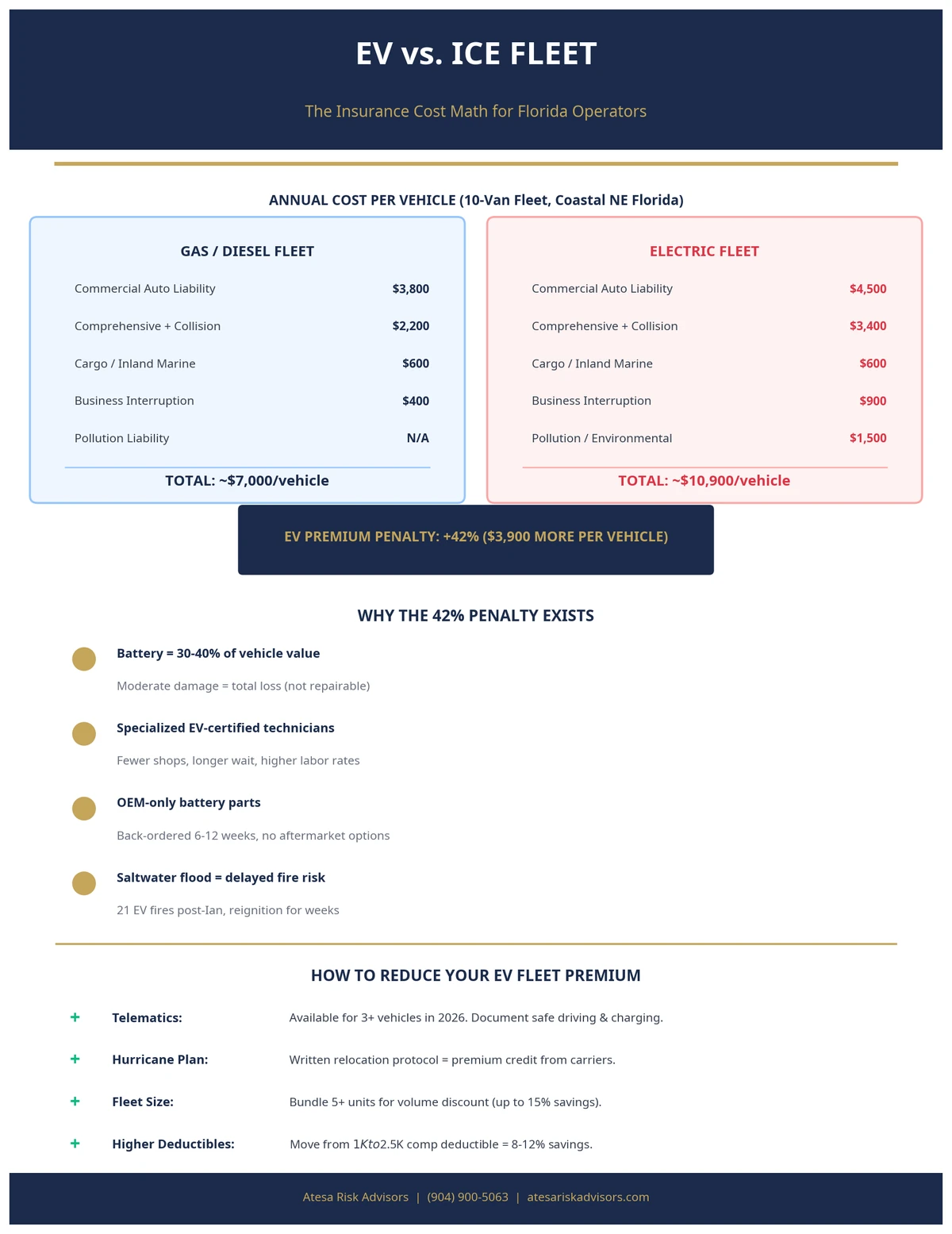

- Electric commercial fleets cost more to insure than gas fleets because the high-voltage battery represents 30–40% of a vehicle's value — so even moderate damage can trigger a total loss, and specialized labor plus back-ordered OEM parts lengthen downtime and inflate claim severity. National data shows EVs run roughly 42% more expensive to insure than comparable gas vehicles.

- Florida's defining EV exposure is the saltwater-flood battery fire. After Hurricane Ian (2022), the Florida State Fire Marshal's office linked roughly 21 fires to flood-damaged electric vehicles, and lithium-ion battery fires can ignite days after the water recedes — then reignite repeatedly after firefighters believe they are out.

- A standard commercial auto policy does cover flood and fire damage to an EV through its comprehensive (other-than-collision) coverage, but hurricane and named-storm deductibles, total-loss valuation on a damaged battery, and downtime can still leave large uninsured gaps.

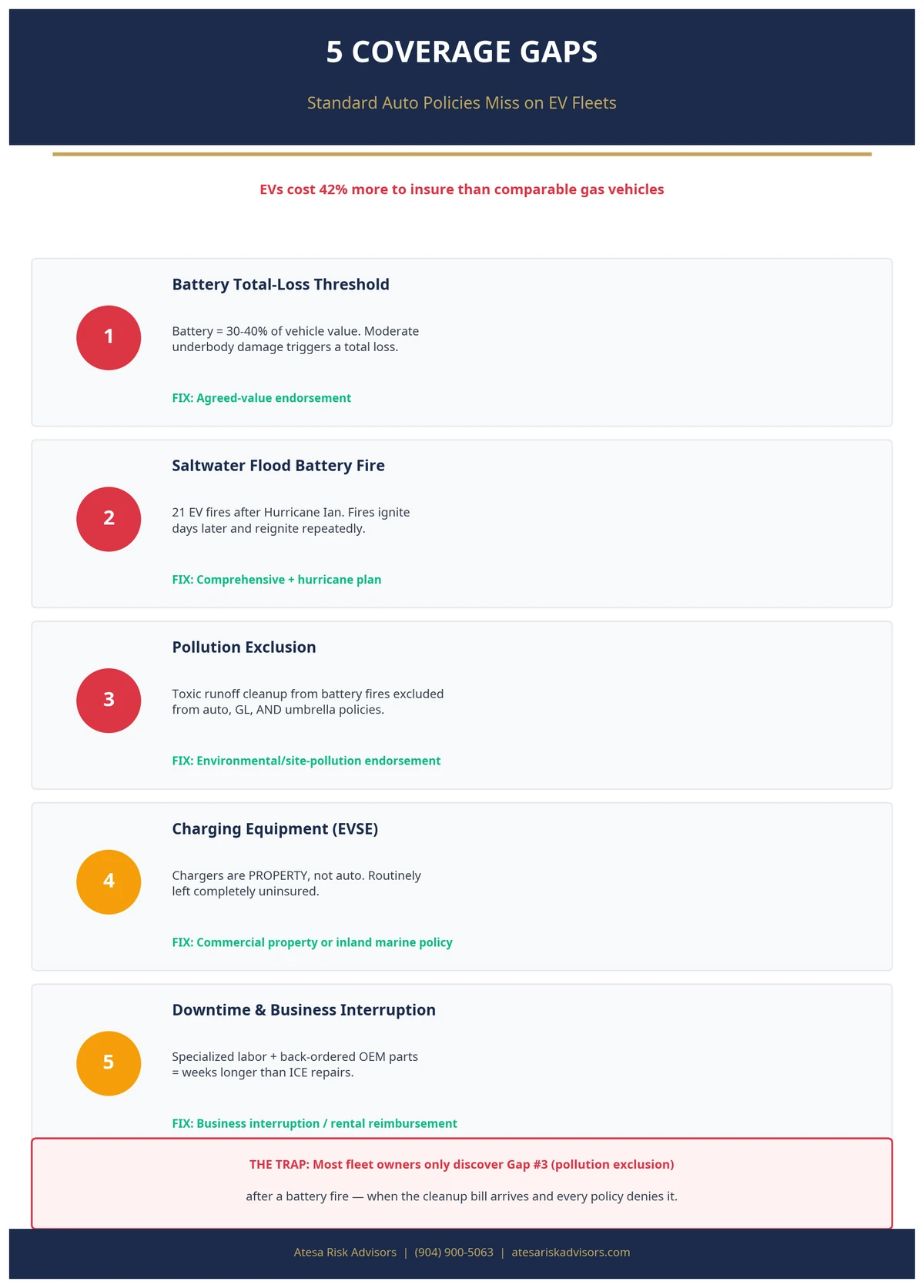

- Charging stations (EVSE) are property, not auto. They belong on a commercial property or inland marine policy — not your fleet auto policy — and are routinely left uninsured entirely.

- The pollution-exclusion gap is the one most owners never see: the toxic runoff and third-party cleanup costs from a battery fire are excluded by most commercial auto, general liability, and umbrella policies. A separate environmental or site-pollution endorsement is the fix.

- Florida Statute § 627.7415 sets minimum liability limits for heavier commercial vehicles, and coastal garaging in Duval, Nassau, and St. Johns counties plus a documented hurricane plan materially affect what an EV fleet pays.

- Telematics-based pricing is now available to fleets as small as three vehicles in 2026 — a real lever for EV operators who can document safe driving and charging practices.

Florida EV commercial fleet insurance is commercial auto coverage structured for the unique loss profile of electric vehicles — high battery-replacement costs, longer repair downtime, and the saltwater-flood fire risk that has caused dozens of Florida EVs to ignite after hurricanes. A standard commercial auto policy will cover an EV, but it rarely addresses charging-equipment property, environmental cleanup after a battery fire, or the higher total-loss threshold a damaged battery triggers. Fleet operators in coastal counties like Duval, Nassau, and St. Johns need a program built around these gaps — not a generic policy pulled off a comparison site.

What Counts as an EV Commercial Fleet?

A commercial fleet is simply two or more vehicles insured under a single business auto policy, titled to a company rather than an individual. A fleet auto policy lets you add and remove vehicles mid-term and apply one set of liability limits and deductibles across every unit, instead of buying separate policies. When some or all of those vehicles are battery-electric — Rivian or Ford E-Transit delivery vans, Tesla rideshare sedans, a Mullen or BrightDrop box truck running last-mile routes out of a Jacksonville distribution hub — you have an EV commercial fleet.

The distinction matters because personal EV insurance and commercial EV insurance are different products. A personal Tesla policy will not respond to a claim if the vehicle is being used to deliver packages, haul tools, or transport paying passengers. In Florida, where last-mile delivery, rideshare, and contractor fleets are electrifying fastest, "I have insurance on my Tesla" is not the same as "my Tesla is insured for the way my business actually uses it." That gap — between how a vehicle is titled, used, and insured — is where uncovered claims live.

Why EVs Cost More to Insure Than Gas Vehicles

The single biggest driver is the battery pack. On most EVs it represents 30–40% of the vehicle's total value, and it is the component most exposed in a collision or flood. Insurers have repeatedly declared EVs a total loss over battery damage alone, because a replacement pack plus the specialized labor to install it can exceed the depreciated value of the vehicle. That pushes the total-loss threshold — the point at which the insurer pays out the vehicle's value instead of repairing it — far lower than fleet owners expect.

Three more cost drivers stack on top:

- Specialized labor. High-voltage systems require certified technicians and dedicated bays. There are fewer of them, so labor rates and wait times are higher.

- OEM parts and downtime. Proprietary components and limited parts supply mean a repair that takes a week on a gas van can take a month on an EV — and the policy keeps paying rental reimbursement the whole time, raising claim severity.

- Repair-network gaps. Outside major metros, the nearest EV-certified shop may be hours away, extending the period your vehicle is off the road and not earning revenue.

National figures put the EV premium gap at roughly 42% versus a comparable gas vehicle, narrowing to about 18% on newer model years as repair networks mature. Layer that on top of Florida — already one of the most expensive auto-insurance states in the country because of storm exposure, litigation, and high repair costs — and an EV fleet operator is stacking a vehicle-type surcharge on an already steep base rate.

The Florida Problem: Saltwater Flooding and Battery Fires

This is the exposure that makes Florida EV fleets genuinely different from EV fleets in Ohio or Arizona, and it is the reason this coverage has to be structured, not price-shopped.

When a lithium-ion battery is submerged in saltwater, the salt bridges the battery's positive and negative terminals and creates a short circuit. That short produces heat, corrosion, and electrical arcing, and it can drive the cells into thermal runaway — a self-sustaining chemical reaction that ignites a fire. These fires are uniquely dangerous for three reasons: they can start days or even weeks after the water recedes, they burn extremely hot, and they reignite after being extinguished, sometimes after tens of thousands of gallons of water have been applied.

Florida has the loss record to prove it. After Hurricane Ian (2022), the Florida State Fire Marshal's office associated roughly 21 fires with flood-damaged electric vehicles, and the National Highway Traffic Safety Administration (NHTSA) opened formal study of saltwater EV immersion. Then-Chief Financial Officer and State Fire Marshal Jimmy Patronis issued repeated consumer alerts after Ian and Hurricane Idalia (2023) warning EV owners to move flood-exposed vehicles away from homes and garages because of the reignition risk. After Hurricane Helene (2024), international fire-service tallies counted 11 electric cars and 48 lithium-ion batteries that caught fire following exposure to salty floodwater.

For a fleet, the implications are operational, not just theoretical. If you garage 15 electric delivery vans in a single coastal Jacksonville depot that takes on storm surge, you are not facing one flooded vehicle — you are facing a clustered total loss and a fire exposure to the building itself and to every other vehicle parked beside it. Where you store the fleet, whether you can relocate it before a named storm, and whether you have a written hurricane plan are no longer paperwork questions. They are underwriting questions that determine whether a carrier will write you at all.

Where a Standard Commercial Auto Policy Falls Short

A well-written commercial auto policy is the foundation, and its comprehensive coverage — the "other-than-collision" piece — does respond to flood and fire damage to the vehicles themselves. The problem is what sits around that coverage.

Hurricane and named-storm deductibles

Many Florida commercial auto and fleet programs apply a separate, percentage-based named-storm deductible rather than a flat dollar amount when damage comes from a declared hurricane. On a flooded fleet, that deductible can run into five figures before the carrier pays a dollar. Knowing whether your policy uses a flat comprehensive deductible or a percentage storm deductible is the difference between a manageable claim and a budget event.

Total-loss valuation on the battery

Because battery damage so often totals an EV, the valuation method in your policy matters enormously. Actual cash value, agreed value, and any new-vehicle replacement provision produce very different checks. Fleet owners who financed or leased their EVs also need gap or lease/loan coverage, because a totaled EV can leave a balance owed that the standard payout will not cover.

Charging infrastructure is not auto coverage

Your EVSE — the charging stations, wall connectors, and depot charging hardware — is property, not a vehicle. It does not belong on, and is not covered by, your fleet auto policy. A power surge, lightning strike, vandalism, or flood that destroys a bank of depot chargers is a commercial property or inland marine claim. Fleets that electrify without adding this coverage are leaving tens of thousands of dollars of equipment uninsured. (This is the same inland-marine logic contractors use for tools and equipment — see our Florida contractor insurance bundle guide.)

The pollution-exclusion gap

This gap surprises most fleet owners. When an EV battery burns, it releases toxic gases and leaves contaminated firefighting runoff. If that contamination reaches a neighbor's property, a stormwater drain, or the ground, the cleanup and third-party bodily-injury costs are typically excluded by standard commercial auto, general liability, and umbrella policies under the pollution exclusion. The fix is a dedicated environmental or site-pollution endorsement built for the fleet — coverage an AI quote engine will never suggest because it does not know the exposure exists.

Downtime and business interruption

Because EV repairs run long, the revenue you lose while a van sits at a certified shop can dwarf the repair cost. Downtime or business-interruption coverage structured for a fleet helps bridge that, and it is priced very differently for EVs than for gas vehicles.

Underwriting Reality: Who Will Even Write an EV Fleet?

Carrier appetite is the quiet variable that decides everything, and it is exactly what a comparison site cannot tell you. Some national carriers fold EV coverage into standard commercial auto at no extra charge — The Hartford, for example, includes a Broad Form endorsement extending coverage to hybrids and EVs on its commercial auto policies. Progressive consistently ranks at the top of Florida's commercial auto market for breadth and price. But appetite for a fleet of EVs garaged in a coastal flood zone is narrower than appetite for a single EV in a personal policy, and it shifts every renewal season.

A specialist broker knows which markets are open to EV fleets this quarter, which ones are quietly non-renewing coastal commercial auto, and how each one treats battery valuation, named-storm deductibles, and garaging. That carrier-by-carrier knowledge — built from placing and renewing real Florida fleets — is what a comparison site cannot show you, and it shifts every renewal.

One bright spot for 2026: telematics-based pricing has expanded to fleets as small as three vehicles. If your EVs already capture driving and charging data, documenting safe operation can unlock premium reductions that used to be reserved for national fleets. A broker who knows which carriers reward that data can turn your telematics into dollars.

How to Structure a Florida EV Fleet Insurance Program

- Inventory the fleet by use, not just by VIN. List every electric vehicle, how it is used (delivery, rideshare, contractor transport, executive travel), where it is garaged, and who drives it. Use determines which form and limits apply.

- Set liability limits to the law and the risk. Florida Statute § 627.7415 sets minimum liability limits for commercial motor vehicles by weight, but minimums rarely protect a business against Florida's litigation environment. Most fleets layer a commercial umbrella above the auto policy.

- Confirm comprehensive terms in writing. Pin down the deductible structure (flat vs. named-storm percentage), the battery/total-loss valuation method, and gap coverage for financed or leased units.

- Insure the chargers separately. Add depot charging equipment to a commercial property or inland marine policy.

- Add the environmental endorsement. Close the pollution-exclusion gap with a site-pollution or environmental policy sized to the fleet and storage location.

- Document a hurricane and relocation plan. A written plan to move vehicles to higher ground before a named storm reduces both your loss risk and, often, your premium.

What Actually Decides Your EV Fleet Program

Three things determine whether an EV fleet program holds up after a storm: which carriers are currently writing EV fleets in coastal Florida, how each one values a damaged battery and applies named-storm deductibles, and whether the charging-equipment and pollution gaps are closed. Those answers shift every renewal and vary carrier by carrier, which is why an EV fleet in Florida is structured rather than price-shopped.

Related Reading

- FMCSA Is Recalculating Your Fleet's Safety Score: The 2026 Overhaul — how the rebuilt scoring system reprices every fleet, electric ones included.

- Why Did My Florida Trucking Insurance Double? The 2026 Math Behind Your Renewal — the commercial-auto cost pressure behind every Florida fleet renewal.

- Does Commercial Property Insurance Cover Hurricanes in Florida? The 2026 Reality Check — where your charging equipment and depot belong.

- Florida Commercial Insurance Rates in 2026: A Complete Guide for Business Owners — how fleet limits and umbrellas are priced.

How Atesa Risk Advisors Can Help

Atesa Risk Advisors is a Jacksonville-based, Florida-licensed (2-20 General Lines) independent brokerage serving Florida businesses statewide. We are a RamseyTrusted provider and shop 40+ A-rated carriers, including the specialty commercial auto and environmental markets that national comparison platforms cannot reach.

Insuring an electric fleet in coastal Florida is a structuring problem, not a price-shopping problem. Working with a broker who knows which carriers will write EV fleets, how each one treats battery valuation and named-storm deductibles, and how to close the charger and pollution gaps can be the difference between a clean program and a six-figure surprise after the next storm.

Want an EV fleet coverage review for your Florida business? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Frequently Asked Questions

Does a regular commercial auto policy cover electric vehicles in Florida?

Yes — a standard commercial auto policy covers EVs, and its comprehensive coverage responds to flood and fire damage. The gaps are around the policy: charging equipment, environmental cleanup after a battery fire, named-storm deductibles, and battery total-loss valuation. Those need to be addressed deliberately.

Why is insurance for an electric fleet more expensive?

The battery represents 30–40% of an EV's value and is easily totaled, specialized repairs take longer and cost more, and downtime drives up claim severity. Nationally, EVs run about 42% more to insure than comparable gas vehicles, narrowing to roughly 18% on newer models.

Are EV battery fires really a Florida insurance issue?

Yes. Saltwater flooding can short-circuit a lithium-ion battery and cause fires that start days later and reignite after being put out. Florida fire officials linked roughly 21 fires to flood-damaged EVs after Hurricane Ian, and more followed Idalia and Helene. It is the defining EV exposure in coastal Florida.

Will my policy pay if a flooded EV catches fire weeks after the storm?

Damage to the vehicle itself is generally covered under comprehensive, even with delayed ignition, subject to your deductible. What is usually not covered is third-party pollution cleanup and bodily injury from the fire's toxic runoff — that requires a separate environmental endorsement.

Does my fleet policy cover my charging stations?

No. Charging stations (EVSE) are property, not vehicles, so they are not covered by your auto policy. They belong on a commercial property or inland marine policy. Many fleets electrify and unknowingly leave their charging hardware uninsured.

What is the pollution exclusion and why does it matter for EVs?

The pollution exclusion is standard language in commercial auto, general liability, and umbrella policies that removes coverage for contamination and cleanup. Because a battery fire creates toxic runoff, that exclusion can leave the cleanup and third-party claims entirely uninsured unless you add an environmental policy.

What minimum coverage does Florida require for commercial vehicles?

Florida Statute § 627.7415 sets minimum liability limits for commercial motor vehicles based on weight, on top of standard financial-responsibility rules. Minimums rarely protect a business adequately, so most fleets carry higher limits plus a commercial umbrella.

How does where I park my EV fleet affect my premium?

Garaging location is a major rating factor. A fleet stored in a coastal flood zone in Duval, Nassau, or St. Johns County faces clustered flood and fire exposure, which raises premium and can limit which carriers will quote. A written plan to relocate vehicles before a named storm can help.

Can a small EV fleet get telematics discounts?

Yes. As of 2026, behavior-based and telematics pricing is available to fleets as small as three vehicles. EVs that already capture driving and charging data can use it to document safe operation and earn premium reductions, if the carrier is one that rewards that data.

Do I need separate coverage for rideshare or delivery use?

Almost always. A personal EV policy excludes business use, and even a commercial policy must be rated for the specific use — delivery, rideshare, or passenger transport. Misrepresenting how a vehicle is used can void coverage at claim time.

How long does an EV take to repair compared to a gas vehicle?

Often several times longer, because of specialized labor and limited OEM parts supply. That extended downtime is why business-interruption or downtime coverage is priced differently for EVs and why claim severity runs higher.

Should EV fleet owners worry about the total-loss threshold?

Yes. Because the battery is so valuable, even moderate damage can total an EV. Confirm your valuation method (actual cash value, agreed value, or new-vehicle replacement) and add gap coverage if the vehicles are financed or leased.

Sources

[1] NHTSA — Reports on Saltwater Immersion of Electric Vehicle Batteries

[3] The Conversation — Saltwater Flooding Is a Serious Fire Threat for EVs and Other Lithium-Ion Devices

[5] Insurify — Electric Vehicle Insurance Cost Report (EV Premium Penalty)

[6] The Hartford — Electric Vehicle and Commercial Auto Insurance

[7] Florida Statutes § 627.7415 — Commercial Motor Vehicles; Additional Liability Insurance Coverage

[8] Florida Office of Insurance Regulation (OIR)

[9] Idaho National Laboratory — Understanding Impacts of Flood Damage on Vehicle Batteries

[10] Propel Insurance — EV Fires: An Environmental Liability Risk Many Businesses Don't See Coming

*Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. He helps Florida fleet operators structure commercial auto programs so an electric fleet — and the next hurricane — does not become an uninsured financial event.