Florida Contractor Insurance Bundle: The Complete 2026 Guide to GL, Workers' Comp, Tools, and Builders Risk

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 28, 2026

Key Takeaways

- Florida contractors need at minimum six separate coverage lines — GL, workers' compensation, inland marine, commercial auto, builders risk, and umbrella — because a single gap can trigger a state Stop-Work Order or leave a six-figure claim entirely uninsured.

- Florida's Division of Workers' Compensation conducts surprise job-site compliance sweeps; under Florida Statute § 440.107, a Stop-Work Order freezes every active job site statewide — not just the location where non-compliance was found.

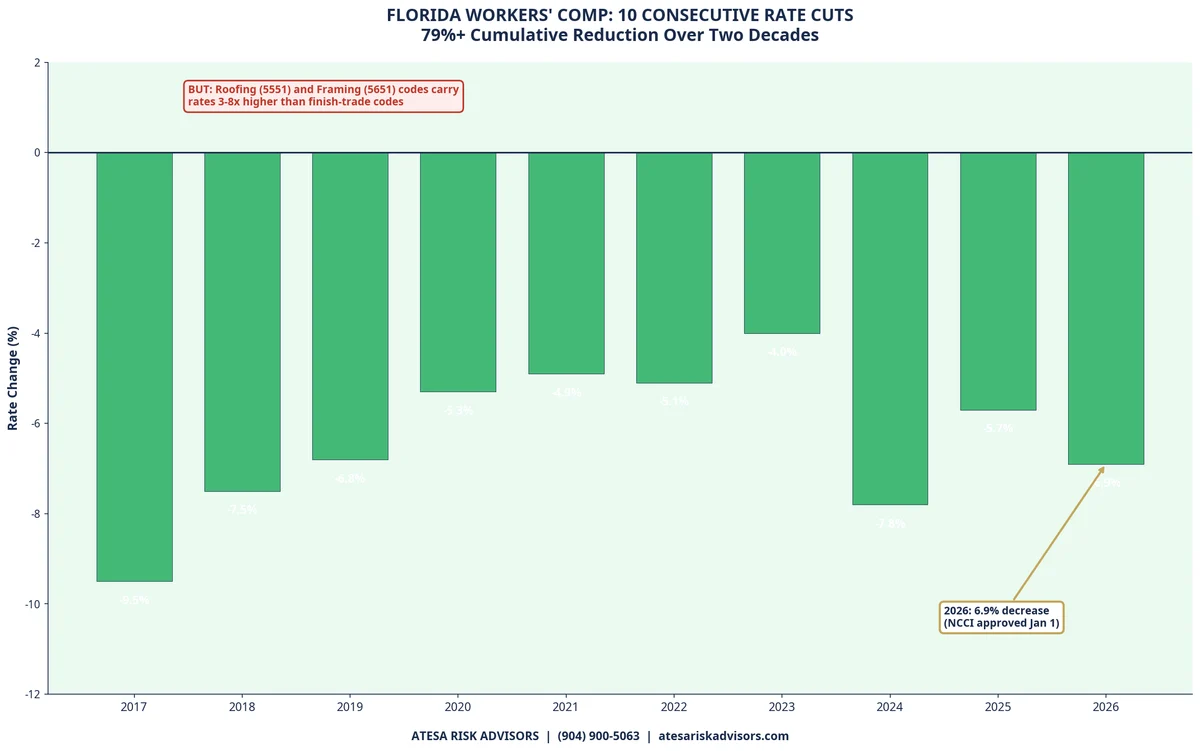

- NCCI approved a 6.9% average workers' comp rate decrease effective January 1, 2026 — the tenth consecutive annual cut — but roofing and framing class codes carry rates 3–8× higher than finish-trade codes; misclassifying workers to reduce premiums is insurance fraud under Florida law.

- Builders risk in Florida's coastal Tier 1 counties (Monroe, Miami-Dade, Broward, Lee, Collier, Pinellas) costs $1.20–$4.50 per $100 of insurable value annually, with projects within one mile of saltwater often paying double the inland rate.

- Up to 22% of subcontractor certificates of insurance are invalid at the time of a claim; as the general contractor, you absorb the uninsured liability if a sub's policy has lapsed or excludes the relevant work.

- General liability rates are increasing 5–15% in 2026 due to social inflation and nuclear verdicts in Florida's high-litigation counties; carrier selection and prior-loss presentation are critical to controlling renewal costs.

- Bundling policies with a coordinated program can unlock 10–20% package discounts, but only when trade mix, payroll exposure, and coastal risk are correctly structured by a specialist broker.

A Florida contractor insurance bundle is a coordinated stack of six coverage lines — general liability, workers' compensation, inland marine for tools and equipment, commercial auto, builders risk, and umbrella — that together protect a licensed contractor from the state's most common and most expensive losses. In 2026, a typical small Florida general contractor or trade contractor with 10–25 employees and $2 million in annual revenue pays $18,000–$45,000 per year in combined premiums, with coastal location, NCCI class code, claims history, and subcontractor exposure driving the final number.

Why "Just GL" Leaves Florida Contractors Dangerously Exposed

Most contractors first purchase general liability because the Florida Department of Business and Professional Regulation (DBPR) requires it as a condition of licensure. The state minimum is $300,000 — a threshold that a single serious bodily-injury claim in Miami-Dade, Broward, or Palm Beach County can blow through entirely. Those three counties generate the highest concentration of "nuclear verdicts" (jury awards exceeding $10 million) on construction bodily-injury and defect claims anywhere in the southeastern United States.

A commercial general liability policy — the industry calls it a CGL — covers third-party bodily injury and property damage: a client who trips over your power cord, a wall you damaged during a renovation, a completed project where someone later alleges faulty work. What it does not cover:

- Your own employees' on-the-job injuries — that is workers' compensation

- Your own tools, equipment, and materials in transit — that is inland marine

- Vehicles you own or operate for business purposes — that is commercial auto

- A structure under construction before the client takes possession — that is builders risk

- Claims that exceed your GL policy limit — that is commercial umbrella

Most commercial clients, developers, and GC subcontracts now require a minimum of $1 million per occurrence, and many lenders and public-project owners require $2 million. Relying on the $300,000 DBPR minimum creates both a coverage gap and a credibility gap when bidding on serious commercial work.

The Six Coverage Lines in a Florida Contractor Bundle

1. General Liability (CGL)

What it covers: Third-party bodily injury, property damage, personal and advertising injury, and completed operations — meaning claims that arise after the job is finished and you have moved on to the next project.

Florida-specific completed-operations requirement: Completed-operations coverage must be maintained for a minimum of five years after project completion to align with Florida's construction defect statute of repose under Florida Statute § 95.11(3)(c). That statute gives a claimant up to ten years for latent construction defects. Many contractors let completed-ops lapse the moment they believe a job is closed — this creates silent long-tail exposure that can result in an uninsured six- or seven-figure defect claim years later.

2026 rate environment: GL premiums are increasing 5–15% at renewal driven by social inflation and third-party litigation funding, both of which are especially pronounced in Florida's high-litigation urban counties. Carriers are scrutinizing prior losses more aggressively; a single five-year loss exceeding $50,000 can move a contractor out of the standard (admitted) market and into non-admitted surplus lines, which adds Florida's 5% surplus lines stamp tax and generally higher base premiums.

Typical 2026 cost: $4,000–$15,000 annually for a small Florida GC, varying by revenue, payroll, and county of operations.

For a detailed cost breakdown by revenue band, see our guide to Florida general liability insurance costs in 2026.

2. Workers' Compensation

What it covers: Medical treatment and lost-wage replacement for employees injured on the job, regardless of who was at fault. In a serious injury case — a fall from scaffolding, a hand injury from power tools — WC claims routinely reach $100,000–$500,000 before settlement.

Florida's mandatory coverage threshold: Under Florida Statute § 440.10, any employer in the construction industry with one or more employees must carry workers' compensation. This is a lower threshold than most other industries (which trigger at four employees). Sole proprietors in construction are not automatically exempt — you must affirmatively file a Florida WC Exemption through the Department of Financial Services (DFS) to legally opt out, and that exemption applies only to qualifying sole proprietors and certain corporate officers, subject to per-person caps.

The Stop-Work Order reality: Florida's Division of Workers' Compensation (DWC) conducts unannounced job-site compliance sweeps throughout the year. Under § 440.107, the DWC can issue a Stop-Work Order on the spot if a contractor cannot immediately produce proof of valid WC coverage. The order:

- Freezes every active job site statewide — not just the one being inspected

- Remains in effect until valid coverage is proven and a penalty is paid

- Carries a penalty equal to 1.5× the premium that should have been paid for the entire period of non-coverage

Contractors have received six-figure penalties for lapses as short as 30 days. The financial and operational damage from a multi-site Stop-Work Order during peak construction season can exceed the annual WC premium many times over.

2026 rate news — the tenth consecutive cut: NCCI (National Council on Compensation Insurance) filed a 6.9% average rate decrease effective January 1, 2026, and Florida approved it — continuing a streak of cuts that has reduced Florida's WC rates by more than 79% cumulatively over two decades. The reduction is driven by falling lost-time claim frequency and improved workplace safety data.

However, averages obscure wide variation by NCCI class code:

| Trade | NCCI Class Code | 2026 Rate Trend |

|---|---|---|

| Roofing | 5551 | High rates, modest reduction |

| Framing / rough carpentry | 5651 | Elevated — 3–5× finish trades |

| Electrical | 5190 | Moderate, favorable trend |

| Plumbing | 5183 | Moderate |

| Painting | 5474 | Above-average reduction in 2026 |

| Drywall | 5480 | Above-average reduction in 2026 |

| GC — executive supervision | 8227 | Low rate (supervisory only) |

NCCI class code accuracy is non-negotiable. Assigning a roofing employee to a painting code to reduce premiums is insurance fraud under Florida law. Carriers conduct mandatory annual payroll audits, and discovered misclassification results in retroactive premium adjustment, potential policy cancellation, and referral to the DFS Division of Insurance Fraud.

See our full guide to Florida workers' comp rates in 2026 for rate tables by trade and county.

3. Inland Marine — Tools, Equipment, and Materials

What it covers: Physical loss or damage to contractor-owned tools, portable equipment, and building materials in transit or stored at job sites. The term "inland marine" is insurance industry legacy language — it originally referred to goods transported overland from seaports. In practice, it is mobile property coverage for everything that leaves your yard.

Why it matters in Florida: Tools and equipment are stolen from job sites and contractor vehicles at elevated rates in Florida's high-growth construction markets — the Tampa Bay area, the Orlando/I-4 corridor, Jacksonville, and South Florida. A standard commercial property policy covers equipment only at your fixed business address. The moment a generator, laser level, concrete saw, or compressor leaves the yard, a property policy provides zero protection.

Coverage structure options: Inland marine policies are written on a scheduled basis (each item listed with its replacement value) or a blanket basis (one aggregate limit covering all equipment up to the total). Blanket coverage is simpler to administer but creates underinsurance risk if your equipment inventory grows without a mid-year update. A broker who reviews your equipment list at each renewal prevents surprise gaps.

Typical 2026 cost: $1,200–$4,500 annually for $150,000–$500,000 in covered tools and equipment.

4. Commercial Auto

What it covers: Bodily injury and property damage liability for vehicles owned, leased, or regularly used for business purposes, plus physical damage (collision and comprehensive) coverage on owned vehicles.

Florida-specific issue: Personal auto policies contain commercial-use exclusions. Florida courts have consistently upheld those exclusions on at-fault claims. A contractor driving a work truck to a job site under a personal policy is exposed — the insurer can deny the entire claim. Every vehicle that regularly transports tools, materials, or employees to job sites requires a commercial auto policy.

2026 rate pressure: Commercial auto rates are up 5–10% in 2026, driven by motor vehicle repair cost inflation — imported replacement parts increased roughly 9.7% from tariff-related supply chain disruptions — and medical cost inflation. Florida's no-fault PIP system remains in effect under Florida Statute § 627.736. Repeal has been proposed repeatedly — most recently SB 522 and HB 769 in the 2026 session, both of which died in committee — but none has become law. Contractors with vehicle fleets should review their commercial auto limits with a broker at each renewal, given Florida's high-cost auto-liability environment.

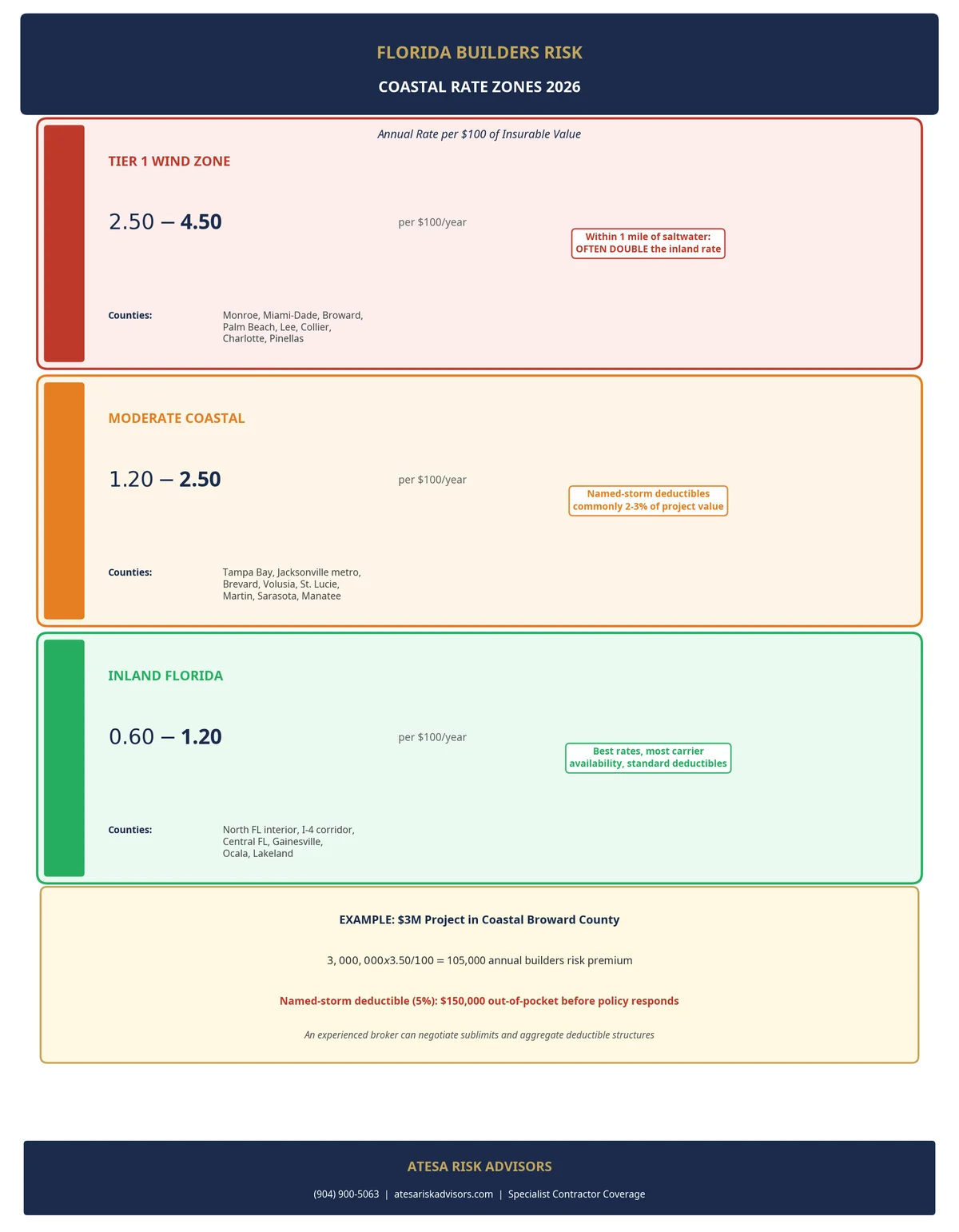

5. Builders Risk

What it covers: Physical damage to a structure under construction — fire, theft, vandalism, windstorm, lightning, and collapse — from the day work begins until the owner takes possession or the project reaches substantial completion. Once the owner occupies the building, builders risk ends and a standard commercial property policy takes over.

Florida coastal premium reality: Rate per $100 of completed insurable value varies significantly by geography:

| Location | Annual Rate per $100 |

|---|---|

| Inland Florida (North FL, I-4 corridor, Central FL) | $0.60–$1.20 |

| Moderate coastal (Tampa Bay, Jax metro, Brevard) | $1.20–$2.50 |

| Tier 1 wind zone (Monroe, Miami-Dade, Broward, Palm Beach, Lee, Collier, Charlotte, Pinellas) | $2.50–$4.50 |

Projects within one mile of saltwater regularly pay double the inland rate and frequently face named-storm deductibles of 2–5% of completed project value. A $3 million project in coastal Broward carries a $60,000–$150,000 out-of-pocket deductible before the policy responds to a hurricane loss. An experienced broker can negotiate named-storm sublimits and aggregate deductible structures that a standard admitted carrier's policy form may not offer — or can access London market capacity where domestic carriers will not go.

Hurricane season timing: Builders risk is typically purchased at project start. Any project spanning June 1–November 30 crosses active hurricane season. Underwriters in Tier 1 coastal counties are increasingly requiring documented wind-mitigation plans and job-site securing protocols as a condition of coverage during hurricane season months.

Who carries it: In Florida, builders risk is most commonly purchased by the GC or developer, with the obligation defined in the construction contract. All construction lenders require proof of builders risk before disbursing draws, and most commercial project owners require it before a Notice to Proceed is issued.

For context on how named-storm deductibles work across commercial lines, see our guide to commercial property insurance and hurricane coverage in Florida.

6. Commercial Umbrella

What it covers: Additional liability limits stacked above the underlying GL, commercial auto, and employers' liability policies — typically available in $1M, $2M, and $5M increments. The umbrella responds after the underlying policy's limit is exhausted.

Why Florida contractors need it: The same litigation environment that inflates GL premiums also produces nuclear verdicts that blow through $1M limits. Most commercial project owners, developers, and GC agreements now require $5M or more in total combined liability (GL plus umbrella combined). Commercial umbrella is the most cost-efficient path to those limits — typically $800–$2,500 per year per $1M of additional coverage, compared to the much higher cost of raising the underlying GL limit directly.

The Subcontractor Certificate of Insurance Trap

If you hire subcontractors, you inherit their uninsured risk unless you actively manage it. Florida's Construction Lien Law (Chapter 713, Florida Statutes) and standard subcontract agreements require subs to carry their own GL and WC — but requiring coverage and verifying active coverage are entirely different activities.

Industry audits have found that up to 22% of subcontractor certificates of insurance are invalid at the time of a claim. Common problems include:

- Policy lapsed between certificate issuance and the date of loss

- Class codes or trade description on the sub's policy exclude the type of work being performed

- Certificate names a different legal entity than the sub actually doing the work

- Additional insured endorsement is missing, defectively worded, or applies only to ongoing operations (not completed operations)

As the general contractor, you become the insurer of last resort for any uninsured sub claim. Florida courts have consistently found GCs liable for injuries to uninsured subcontractors' workers under the statutory employer doctrine.

A specialist broker manages this risk by:

- Maintaining a COI expiration calendar and flagging sub certificates within 30 days of lapsing

- Verifying active WC coverage directly in the DWC Proof of Coverage database at myfloridacfo.com — not just accepting the certificate at face value

- Confirming that the sub's NCCI class codes match the scope of work on your specific project

- Reviewing additional insured endorsements to confirm they are properly structured and extend to completed operations where applicable

No online quoting engine or automated platform performs any of these functions.

How Florida Carriers Underwrite Contractors Differently by County

Carrier appetite for Florida contractor risks is not uniform across the state. A GC with identical revenue, trade mix, and loss history may access 10–12 standard admitted carriers if operating in Alachua or Duval County, and only 3–4 surplus lines markets if operating in Monroe or coastal Broward County.

Standard admitted carriers — including Nationwide, Markel, Cincinnati Financial, Employers Holdings, and ICW Group — write contractors in lower-hazard counties and file their rates with the Florida Office of Insurance Regulation (OIR). Their policies are backed by the Florida Insurance Guaranty Association (FIGA) in the event of carrier insolvency, which provides policyholders a meaningful protection that surplus lines policies do not offer.

Surplus lines carriers — Lloyd's syndicates, Scottsdale Insurance, Lexington Insurance, and James River Insurance — write the risks that admitted carriers decline: Tier 1 coastal builders risk, high-hazard trades like roofing and demolition, and contractors with significant prior-loss history. Florida charges a 5% surplus lines stamp tax on these premiums, rates are not OIR-regulated, and FIGA coverage does not apply. Placing surplus lines requires a licensed Florida surplus lines broker — a sub-designation beyond the standard 2-20 property and casualty license.

Knowing which specific carriers are actively writing a given trade in a given county in the current underwriting quarter is the day-to-day market intelligence that separates a specialist broker from an automated online form. Carrier appetite shifts with catastrophe-year loss experience, reinsurance treaty changes, and individual carrier business-plan decisions — information that is not reflected in any comparison website.

What to Prepare Before Requesting a Quote

Preparing documentation in advance compresses quote turnaround from two weeks to 48 hours and signals to underwriters that you manage risk proactively — a factor that directly affects pricing. A broker quoting a Florida contractor multi-line program will need:

- DBPR contractor license number and the names of all license holders

- Three to five years of loss runs from all current and prior carriers

- Current-year payroll broken down by NCCI class code (actual figures, not estimates)

- Revenue split by project type: new construction vs. renovation vs. tenant improvement

- Full list of owned and regularly operated vehicles with year, make, model, and use description

- Equipment and tools inventory with estimated replacement values

- List of all active projects: addresses, contract values, and expected completion dates

- Total subcontractor spend in the prior policy year

If your project volume is large enough to qualify for owner-controlled wrap-up coverage, our Wrap-Up & OCIP services page explains when a single-project wrap-up program may be more cost-effective than individual contractor policies.

Why Human Broker Expertise Is Irreplaceable for Contractor Programs

An AI quoting tool or online comparison platform returns a price in 90 seconds. It cannot:

- Audit NCCI class codes against actual job descriptions, payroll registers, and subcontractor agreements to prevent both overpayment and fraud exposure

- Structure completed-operations coverage to align with Florida's § 95.11(3)(c) statute of repose and the specific defect-claim windows in your project types

- Negotiate builders risk named-storm sublimits in Tier 1 coastal counties where a standard admitted policy form may cap hurricane recovery at $250,000 on a $4M project

- Place a contractor with prior losses with a carrier that will actually honor the claim at renewal rather than non-renew or rescind

- Manage the subcontractor COI calendar so a lapsed certificate does not silently become your uninsured six-figure claim

- Coordinate mid-project coverage changes when change orders expand project scope, add new structures, or push the completion date through the next hurricane season

The complexity compounds with your project mix. A residential remodeler doing $800,000 per year in Duval County has a meaningfully different risk profile from a commercial GC doing $6 million per year in Miami-Dade — and both will receive the same online quote if they check the same boxes on an automated form. The difference between a well-structured program and a paper policy that fails at claim time is the broker who knows the difference.

Sources

[1] Florida Statute § 440.10 — Liability for Compensation

[2] Florida Statute § 440.107 — Department Power to Enforce Employer Compliance

[3] Florida Statute § 95.11(3)(c) — Limitations of Actions; Statute of Repose

[4] Insurance Journal — Florida Approves Ninth Straight Workers' Comp Rate Cut for 2026

[5] Insurance Journal — NCCI Calls for 6.9% Average Decrease in Florida Workers' Comp Rates

[6] Florida Division of Workers' Compensation — Proof of Coverage Database

[7] Florida DBPR — Contractor Licensing and Insurance Requirements

[8] Florida Statute § 489.129 — Contractor Disciplinary Proceedings

[9] Florida Chapter 713 — Construction Liens

[10] Florida Office of Insurance Regulation — Surplus Lines

[11] Florida All Risk — 2026 Florida Workers Compensation Rates: Tenth Consecutive Decrease

Frequently Asked Questions

What insurance is legally required for contractors in Florida?

Florida requires licensed contractors to carry general liability insurance as a condition of DBPR licensure, with a minimum limit of $300,000. Workers' compensation is required for any construction employer with one or more employees under Florida Statute § 440.10. Commercial auto coverage is required for any vehicle used for business purposes. Builders risk, inland marine, and commercial umbrella are not mandated by Florida statute but are routinely required by construction contracts, lenders, and project owners.

How much does contractor insurance cost in Florida in 2026?

A small Florida contractor with 10–25 employees and $2 million in annual revenue typically pays $18,000–$45,000 per year for a complete multi-line program including GL, workers' comp, inland marine, commercial auto, builders risk, and umbrella. The wide range reflects trade type, county of operations, loss history, and coastal project exposure. Roofing and specialty trade contractors operating in Tier 1 coastal counties pay toward the upper end of that range.

What is a Florida Stop-Work Order and how do I avoid one?

A Stop-Work Order is an enforcement action issued by Florida's Division of Workers' Compensation under § 440.107. It freezes all of a contractor's Florida job sites — not just the inspected location — until proof of valid WC coverage is presented and a penalty equal to 1.5× the unpaid premium for the non-coverage period is paid. Avoidance requires maintaining continuous, uninterrupted WC coverage and verifying — not just assuming — that every subcontractor you hire carries current, valid WC coverage before they set foot on your site.

Does a personal auto policy cover my work truck in Florida?

No. Standard personal auto policies contain commercial-use exclusions that Florida courts have consistently enforced. A work truck used to haul tools, materials, or employees to job sites requires a commercial auto policy. Any claim arising from a commercially-used vehicle under a personal policy is likely to be denied in full.

What is inland marine insurance and why do Florida contractors need it?

Inland marine insurance covers contractor-owned tools, portable equipment, and materials while in transit or stored at job sites — property that moves and is excluded from a standard commercial property policy, which covers only items at a fixed business address. In Florida's active construction markets, where job-site theft rates are elevated, inland marine is essential for any contractor with tools exceeding $10,000 in replacement value.

What is builders risk insurance and when is it required in Florida?

Builders risk insurance covers physical damage to a structure under construction — fire, theft, windstorm, and collapse — from groundbreaking until occupancy or substantial completion. While not required by Florida statute, it is universally required by construction lenders before draw disbursement, and most commercial project contracts require it before a Notice to Proceed is issued. In Tier 1 coastal counties, builders risk is the most complex line to place because of named-storm deductibles and limited admitted-carrier appetite.

What NCCI class codes apply to Florida construction workers?

Common Florida construction class codes include: 5551 (roofing), 5645 (carpentry/framing — commercial), 5651 (carpentry/framing — residential, three stories or less), 5190 (electrical wiring), 5183 (plumbing), 5474 (painting), 5480 (drywall/wallboard), and 8227 (GC — executive supervision only, no direct labor). Each code carries a different rate per $100 of payroll. Misclassifying employees into a lower-rate code to reduce premiums constitutes insurance fraud under Florida law and is subject to annual carrier audit.

What does "completed operations" coverage mean for a Florida contractor?

Completed operations is a component of general liability coverage that protects against claims arising after a project is finished — a client who sues two or three years later alleging defective work. Florida's statute of repose (§ 95.11(3)(c)) allows claimants up to ten years to bring certain latent construction defect claims, making continuous completed-operations coverage essential for any contractor doing structural or systems work.

Can I verify a subcontractor's workers' comp coverage in Florida?

Yes. Florida's Division of Workers' Compensation maintains a free, publicly accessible Proof of Coverage database at myfloridacfo.com where any contractor can search by employer name or Federal Employer Identification Number. Verifying coverage directly in the state database — rather than relying solely on a certificate of insurance — is best practice because certificates can be issued for policies that subsequently lapse or are cancelled without notice to the certificate holder.

What is the Florida surplus lines stamp tax and when does it apply?

Florida imposes a 5% surplus lines stamp tax on premiums placed with non-admitted (surplus lines) carriers — insurers not licensed in Florida but authorized to write risks that standard admitted carriers decline. Surplus lines placement is common for Tier 1 coastal builders risk, high-hazard contractor trades, and contractors with significant prior loss history. The tax is added to your premium and must be disclosed by the placing broker. Surplus lines policies are not backed by the Florida Insurance Guaranty Association (FIGA).

Do Florida contractors still need PIP on their commercial auto policies in 2026?

Yes. Florida's no-fault PIP system remains in effect under Florida Statute § 627.736 — repeal has been proposed repeatedly (most recently SB 522 and HB 769 in the 2026 session, both of which died in committee), but none has become law. Contractors should continue to carry PIP plus adequate bodily-injury liability limits, and review their commercial auto coverage with a broker at each renewal given Florida's high-cost auto-liability environment.

Is a certificate of insurance enough to protect me from a subcontractor's uninsured claim?

No. A certificate of insurance is a snapshot confirming coverage existed when the certificate was issued — it does not provide automatic notice when that coverage lapses. Best practice for GCs: collect a current COI before any sub starts work, independently verify WC status in the DWC database, require the sub to add you as an additional insured on their GL policy with both ongoing-operations and completed-operations coverage, and require a 30-day cancellation notice endorsement so you receive advance warning if the sub's policy is cancelled mid-project.

Related Reading

- Why Did My Florida Trucking Insurance Double? The 2026 Math Behind Your Renewal — If your fleet's commercial auto line is the one blowing up your bundle, this is the verified math behind it — plus the free DOT Risk Scorecard that shows your fleet the way underwriters see it.