Townhome or Condo? Solving the St. Johns County Insurance Identity Crisis (2026)

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 13, 2026

Key Takeaways

- Most townhomes in Nocatee, Silverleaf, and Shearwater are deeded as fee-simple — you own the structure and the land beneath it — which means you need an HO-3 homeowners policy, not an HO-6 condo policy [1].

- Buying an HO-6 (condo) policy on a fee-simple townhome creates a "wall-in gap" — if a hurricane rips off your roof, the carrier denies the claim because the HOA never insured the exterior [1][3].

- St. Johns County master policies in 2026 commonly carry $50,000 to $100,000 building deductibles. Florida personal policies cap Loss Assessment coverage at $2,000 with no buy-up option — so owners are personally exposed for the gap, often $20,000+ after a single storm [2].

- HB 815 (the 2024 condo-bill follow-up): Florida carriers can no longer drop a townhome for an "older" roof (15+ years) if it passes a 2026 4-point or wind-mitigation inspection [4].

- St. Johns townhomes are pricing 10 to 15 percent under comparable South Florida units in 2026, thanks to newer Class A fire-rated construction and the First Coast wind-loss advantage [5].

The Insurance Identity Crisis in St. Johns County happens when townhome owners buy the wrong policy form: an HO-6 (condo) policy on a fee-simple townhome they actually own outright. If your recorded deed includes the land beneath your unit — which is the case for most homes in Nocatee, Silverleaf, Shearwater, Beacon Lake, and Beachwalk — you need an HO-3 homeowners policy that covers the roof and exterior walls. Putting the wrong form on the wrong deed isn''t just a paperwork issue. It''s the difference between a covered claim and a $100,000 out-of-pocket hit after the next hurricane.

The confusion is understandable. A row of attached townhomes in Coastal Oaks or Riverview looks architecturally identical to a condominium building. Both have shared walls, an HOA, and rules about exterior paint. But the legal structure — what you actually own under Florida law — is completely different, and the policy you need follows the deed, not the architecture.

This guide walks through the audit we run for every new St. Johns townhome owner: how to read your deed, how to find your HOA''s master policy type, how much Loss Assessment coverage you actually need, and the 2026 market reality across the five biggest townhome communities in the county. The 24-hour identity audit worksheet at the bottom is the printable version your spouse can walk through over coffee.

Is your St. Johns townhouse actually a condo?

The architecture and the legal entity are two different things. In St. Johns County master-planned communities, attached townhomes can be deeded as either fee-simple homes or condominiums. The deed — not the floor plan — decides which policy form you need.

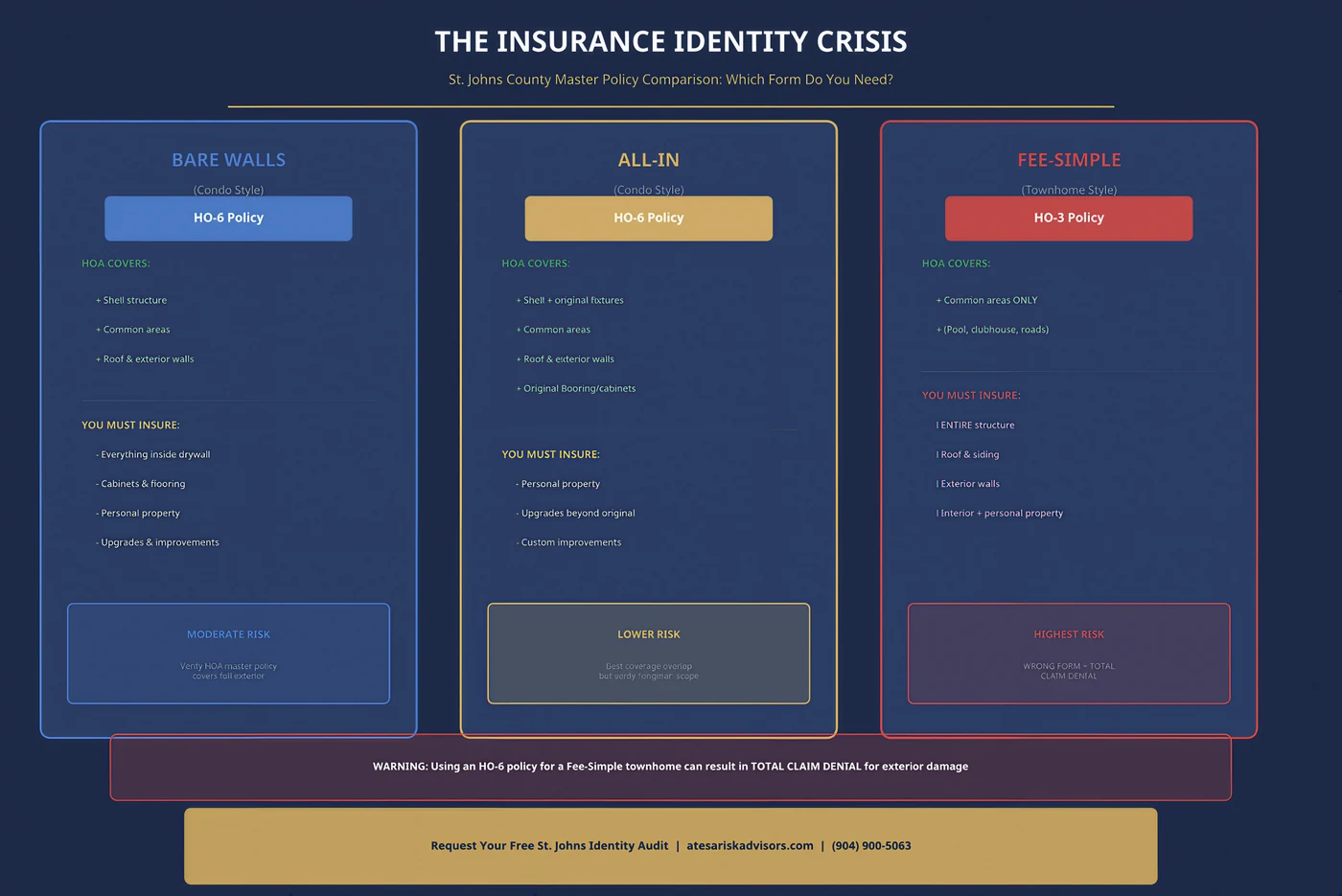

The Condominium (HO-6). You own the air space inside your walls — basically, the cabinets, flooring, contents, and any upgrades. The HOA owns the building structure, the roof, the exterior walls, and the land. Your policy form is HO-6 (a unit-owner''s condo policy that covers everything inside your unit but not the building itself). This is the "walls-in" form most people associate with condo living.

The Fee-Simple Townhome (HO-3). You own the structure and the land it sits on. You are responsible for the roof, the exterior walls, the siding, the foundation, and the parcel underneath. The HOA may handle landscaping or lawn-care of common areas, but the building itself is yours. Your policy form is HO-3 — the standard homeowners policy that covers the whole structure.

The fastest way to tell which one you own is to read the legal description on your recorded deed:

- "Lot X, Block Y, Plat Book Z" → fee-simple. You need HO-3.

- "Unit X of [Community Name], a Condominium" → condominium. You need HO-6.

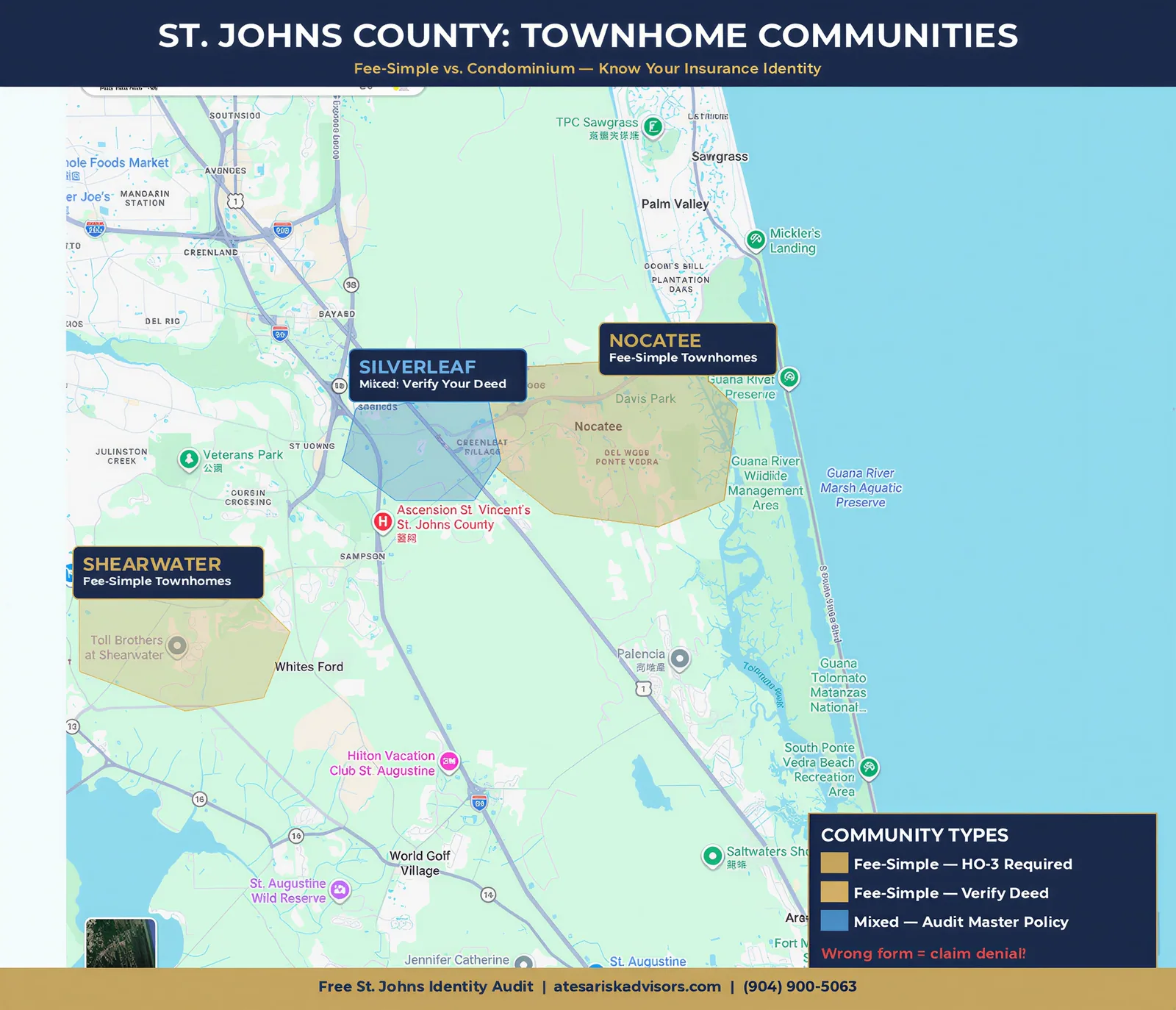

If you bought a townhome in Nocatee (Coastal Oaks, Riverwood, Daniel Park), Silverleaf (Riverview, Heritage Landing), or Shearwater (Trailmark sections), your deed almost certainly reads "Lot X, Block Y" — fee-simple. If you have an HO-6 policy on it, you are misinsured.

The "Wall-In Gap"

Here''s the practical exposure of the mismatch.

Imagine a fee-simple Nocatee townhome with an HO-6 policy on it. A 2026 named storm rolls through and rips half the roof off your unit. You call your carrier to file a claim. Two things happen:

- Your HO-6 carrier denies the claim. The HO-6 form only covers "walls-in" — your cabinets, flooring, contents, and personal liability. The exterior structure (the roof, the trusses, the sheathing) is not on your policy because the HO-6 form assumes an HOA is insuring the building shell above you.

- Your HOA''s master policy also doesn''t cover it. On a fee-simple community, the HOA doesn''t insure individual homes'' roofs — only common-area buildings (clubhouse, pool buildings) if any exist. There is no master policy above you to fall back on.

Result: full roof replacement at 2026 Florida prices — roughly $25,000 to $60,000 — out of your pocket, plus interior water damage, plus loss of use while the structure is uninhabitable. The same loss covered correctly under an HO-3 would have been a routine claim with the standard hurricane deductible.

Download the 24-Hour Identity Audit worksheet → St. Johns Townhome Identity Audit (PDF). Two-page printable with the 7-step audit checklist, the fee-simple-vs-condo decision tree, the loss-assessment exposure math, and a community-by-community quick-reference table.

Auditing the master policy: who owns the roof in 2026?

If your townhome is a condominium (some Beacon Lake and Beachwalk sections are), the next question is what your HOA''s master policy — the building-level policy the association buys to cover shared structure — actually includes. Florida condo master policies come in three flavors, and the type your association carries decides what you personally have to insure.

You find this information in the HOA''s Declaration of Covenants, Conditions, and Restrictions (CC&Rs) — the recorded document that governs the community. The CC&Rs explicitly state which physical components of the building the HOA insures and which fall on the unit owner. Read the "insurance" section carefully; this is the single most important page in the whole document.

The three master policy types:

| Master Policy Type | What the HOA Covers | What YOU Must Insure | Policy Form Needed |

|---|---|---|---|

| Bare Walls | The building shell — exterior walls, roof, common areas | Everything inside the drywall (cabinets, flooring, fixtures, personal property, upgrades) | HO-6 |

| All-In | Shell + original fixtures (original cabinets, original flooring, original fixtures as delivered) | Personal property, upgrades, anything added or changed since the original spec | HO-6 |

| Fee-Simple (no shared structure) | Common areas only (clubhouse, pool building, common landscaping) | The entire structure — roof, exterior walls, foundation, everything | HO-3 |

A few things to confirm when you read the CC&Rs:

- Which master policy type is required by the bylaws (Bare Walls / All-In / N/A for fee-simple).

- What the master policy deductible is — pull the master dec page from the property manager. $50,000 to $100,000 per-building deductibles are the norm in St. Johns 2026.

- How assessments are split when the HOA collects to pay the deductible — usually pro-rata by unit count in your specific building, sometimes by square-footage.

If the CC&Rs and the master dec page disagree (it happens — bylaws lag market reality), the recorded CC&Rs win. Get a legal opinion before assuming you know which document controls.

The $2,000 Loss Assessment cap: the uninsurable exposure to plan for

This is the most expensive uninsurable exposure on most St. Johns townhome policies in 2026.

Loss Assessment is the coverage on your personal HO-3 or HO-6 policy that pays your share when the HOA assesses owners to pay the master policy deductible after a covered loss. Florida personal policies cap Loss Assessment coverage at $2,000 — and most Florida admitted carriers in 2026 do not offer a buy-up endorsement to raise it. You cannot insure your way out of this gap. You have to plan around it.

Here''s the math. Master policies in St. Johns now commonly carry $50,000, $75,000, or $100,000 hurricane / wind deductibles on the building. When a storm causes a covered loss, the HOA pays the deductible first before the master policy responds. To pay the deductible, the HOA assesses owners — usually by unit count or by square-footage share of the affected building. Your share of that deductible above $2,000 is uninsured. You owe it personally, in cash, on a short timeline.

The exposure formula:

`` Owner Exposure = (Master Policy Deductible / Units in Building Cluster) − $2,000 ``

Worked example — a 4-unit Nocatee building with a $100,000 hurricane deductible:

- $100,000 deductible ÷ 4 units = $25,000 share per unit.

- Minus the $2,000 Loss Assessment coverage cap = $23,000 uninsured personal exposure per unit.

- This is a personal liability, not an insurance problem. The right plan is a savings reserve, not extra insurance.

Three mitigation strategies that actually work in Florida 2026:

- Build a personal reserve equal to your assessable share. A line item in a money-market or HOA emergency fund is your real "coverage."

- Advocate at the HOA level to negotiate a lower master policy deductible at renewal. Dropping a $100,000 deductible to $50,000 cuts the owner''s share by half.

- Confirm with your broker whether your specific carrier has any Loss Assessment buy-up available. It is rare in 2026 Florida but worth asking — some surplus-lines or out-of-state forms still offer a higher cap.

A note for fee-simple owners: If you are in a true fee-simple community (no master policy on the building above you — Silverleaf, Shearwater Trailmark, most of Nocatee), there is no master deductible to assess against you, so the $2,000 cap is not a meaningful exposure. The audit still matters because some "fee-simple" communities have a partial master policy on common-area buildings (clubhouses, pool houses), and those can still trigger small assessments — usually well under $2,000 per owner.

Why St. Johns townhomes pay 10–15 percent less than South Florida in 2026

If you''re moving to St. Johns from Miami-Dade, Broward, or even Palm Beach, the rate you''re seeing on a Nocatee townhome will feel meaningfully lower. That''s not an accident — it''s the "First Coast Advantage" working in your favor.

Four structural reasons St. Johns townhomes are priced under South Florida comparables in 2026:

1. Newer construction stock. Nocatee, Silverleaf, Shearwater, Beacon Lake, and Beachwalk are mostly post-2010 developments — and the bulk of inventory is post-2018. Newer construction means Class A fire-rated roofs (the highest fire-resistance rating, mandated by the Florida Building Code 8th Edition for new construction in fire-zone-adjacent areas), hurricane straps that meet current wind-load specs, and impact-rated openings on most units. All three trigger automatic insurance discounts.

2. Wind-loss history. North Florida and the First Coast have a meaningfully lower 30-year hurricane-loss-per-policy track record than South Florida. Carriers price this in. Even when premiums went up 80–110% statewide between 2020 and 2024, St. Johns went up less in raw dollars than Miami-Dade or Broward.

3. HB 815 (2024) roof-age protections. This is the under-discussed 2024 law that matters most for older St. Johns townhomes. Before HB 815, carriers could non-renew a Florida home strictly because the roof was over a certain age (often 15 years for shingles, 25 for tile/metal). After HB 815, carriers cannot drop a policy purely on roof age if the roof passes a current 4-point or wind-mitigation inspection. For owners with 15 to 20-year-old roofs in older Nocatee sections, this is the difference between staying with their current carrier and getting forced to Citizens [4].

4. 17 new admitted carriers actively quoting St. Johns townhomes in 2026. Since HB 837 tort reform passed in March 2023, 17 new admitted-market carriers — meaning state-licensed and regulated insurers whose claims are backed by Florida''s guaranty fund — have re-entered Florida personal lines. Several are aggressively quoting newer-construction townhomes in St. Johns specifically because the loss-ratio expectations are favorable [5].

The wind mitigation lever. If your townhome was built post-2002 to the modern Florida Building Code, ask your broker for a current wind-mitigation inspection (the form is called OIR-B1-1802 — the standard Florida wind-mitigation inspection form). A well-documented form on a typical newer Nocatee townhome can knock 25 to 35 percent off the wind portion of your premium.

Community-by-community roof and deductible reality (St. Johns 2026)

Five major St. Johns townhome communities, what their master policies actually look like in 2026, and what Loss Assessment limit each owner should carry.

| Community | Typical Build Era | Master Policy Type | Typical Building Deductible | Owner Assessable Exposure |

|---|---|---|---|---|

| Nocatee (Coastal Oaks, Riverwood, Daniel Park) | 2010–2024 | Mostly fee-simple, some Bare Walls hybrid | $50k–$100k (where master applies) | $15k–$30k |

| Silverleaf (Riverview, Heritage Landing) | 2018–2026 | Fee-simple, individual roofs | N/A — no master on home structure | $0–$5k |

| Shearwater (Trailmark sections) | 2017–2024 | Fee-simple townhome | N/A — no master on home structure | $0–$5k |

| Beacon Lake | 2019–2026 | Master + Limited Common Elements | $50k–$75k | $12k–$20k |

| Beachwalk | 2018–2026 | Mixed master + fee-simple by phase | $50k–$100k | $15k–$30k |

A few practical notes:

- Nocatee is the trickiest because phases differ. Coastal Oaks predominantly fee-simple. Some Riverwood and Daniel Park townhome courts are Bare Walls condominiums. The CC&Rs for your specific phase control — do not rely on what a neighbor told you about theirs.

- Silverleaf and Shearwater Trailmark are the cleanest — almost all townhomes are pure fee-simple with no shared master policy on the structure. The Loss Assessment concern is minimal there.

- Beacon Lake uses the "Limited Common Elements" model in some sections — the HOA insures shared roofs across attached units but not the interior. This is a common 2020+ master-planned approach. Pull your CC&Rs to confirm.

- Beachwalk mixes phases. Some sections are master-policy condominium townhomes (the ones with shared roofs by design), others are fee-simple. Phase letter and lot number determine which.

What we see on St. Johns townhome submissions

"I audit at least three Nocatee townhome policies a week, and I''d estimate 30 to 40 percent of new homeowners are walking around with the wrong policy form. Almost always it''s an HO-6 on a fee-simple Coastal Oaks townhome — sold by an out-of-area agent who didn''t pull the deed before quoting. The first time we catch it is at the next renewal, and the homeowner had no idea their roof has been uninsured for two years. The fix is straightforward — bind an HO-3 and document the assessable exposure — but if a storm had hit during those two years, it would have been a six-figure mistake."

— Ricardo Alonso, Founder, Atesa Risk Advisors

Florida-Specific Considerations

A handful of Florida statutes and 2024 legislative changes that decide how this works in St. Johns specifically.

Florida Statute 720 — Florida Homeowners Association Act. Governs fee-simple HOAs. Distinct from FS 718 (Florida Condominium Act). If your community is fee-simple, FS 720 controls — assessments, governance, and what the HOA can and cannot require regarding your insurance [6].

Florida Statute 718.111(11) — condo master policy requirements. Applies only if your community is legally a condominium. Specifies what the master policy must cover for the building (the shell + common elements) versus what the unit owner is responsible for. This is the statute that defines "Bare Walls" vs "All-In" coverage requirements [7].

HB 815 (2024). Florida law protecting homeowners from roof-age non-renewals if a current 4-point inspection passes. Critical for older Nocatee phases with 15 to 20-year-old roofs that would have triggered non-renewal under pre-2024 rules. The carrier must accept a passing inspection over a strict roof-age threshold [4].

HB 837 (March 2023) — tort reform. Modified comparative negligence, repealed one-way attorney fees for property claims, tightened the bad-faith framework. This is the legislative reason 17 new admitted carriers have re-entered Florida personal lines in 2026 [5].

Florida Building Code 8th Edition (2023). Sets Class A fire-rated roof minimums and modern hurricane-strap specifications. Newer St. Johns townhomes built to this code automatically qualify for premium credits on the wind portion of coverage [8].

Your 24-Hour Identity Audit Timeline

| Step | Time | What happens |

|---|---|---|

| 1. Pull your recorded deed | 5 min | "Lot X, Block Y, Plat Book Z" = fee-simple (need HO-3). "Unit X of [Condo Name]" = condominium (need HO-6). |

| 2. Pull the HOA Declaration of Covenants (CC&Rs) | 15 min | Identify master policy type: Bare Walls, All-In, or Fee-Simple. Read the insurance section line by line. |

| 3. Pull the HOA master policy declarations page | 20 min | Confirm hurricane / wind deductible (typically $50k–$100k in St. Johns 2026). |

| 4. Pull your current personal policy declarations | 10 min | Check form (HO-3 vs HO-6) and Loss Assessment limit. |

| 5. Identify mismatches and gaps | 15 min | Wrong form? Documented your assessable exposure (master deductible / units in cluster, minus the $2,000 Loss Assessment cap)? Roof age trigger? |

| 6. Submit to a broker for re-quote | 30 min | Three admitted carriers + Citizens benchmark. Provide deed, CC&Rs, master dec, current personal dec. |

| 7. Bind the correct form and document your assessable exposure | Within 24 hours | New effective date matches or precedes old expiration. Confirm the $2,000 Loss Assessment cap on your policy and document your personal exposure as a reserve item, not an insurance need. |

FAQ for St. Johns townhome owners

Q: How do I tell if my Nocatee townhouse is fee-simple or a condominium?

A: Read the legal description on your recorded deed. "Lot X, Block Y, Plat Book Z" means fee-simple — you own the parcel of land. "Unit X of [Community Name], a Condominium" means condominium — you own the air space inside the walls. You can pull a copy of the deed for free from the St. Johns County Clerk of Court''s online records portal. The legal description is on the first page.

Q: If I have the wrong policy form and my roof gets damaged, will the carrier really deny the claim?

A: Yes. An HO-6 (condo) policy specifically excludes the building''s exterior structure — the form was designed assuming an HOA master policy is sitting above it covering the shell. If you''re fee-simple, no such master exists, so the exterior damage is uninsured by both your policy and the (nonexistent) HOA master. The denial is standard, not negotiable. The fix is to bind the correct HO-3 form before the loss, not after.

Q: How much Loss Assessment coverage should a Silverleaf townhouse owner carry in 2026?

A: Florida personal policies cap Loss Assessment at $2,000 and most carriers do not offer a buy-up, so the question is really about exposure, not coverage. Silverleaf is almost entirely pure fee-simple — there is no master policy on the home structure above you, only on common-area buildings like the amenity center. For Silverleaf owners, this is fine because there is no master-policy deductible exposure of any size. The exception is some Riverview phases with Limited Common Elements arrangements; in that case, calculate your share of the master deductible above $2,000 and treat it as a personal reserve item, not an insurance need.

Q: Can my fee-simple HOA require me to carry an HO-3 policy?

A: Yes. Florida HOAs governed under FS 720 can include insurance-form requirements in their CC&Rs, and most do — typically requiring owners to carry "all-risk dwelling coverage equivalent to ISO HO-3 form." This is your association protecting itself from a downstream lawsuit if your underinsured property becomes a code-violation problem after a loss. Read your CC&Rs to confirm — it''s usually in the "Insurance" or "Owner Responsibilities" section.

Q: What does HB 815 mean for my 15-year-old townhome roof?

A: Pre-HB 815, a Florida carrier could non-renew you simply because the roof was 15+ years old (for asphalt shingles). After HB 815, the carrier cannot non-renew on roof age alone if your roof passes a current 4-point inspection. Get the inspection done before your renewal date if you''re at the 15-year mark; a passing inspection holds your existing policy and rate. A failing inspection means you''ll need to repair or replace before renewing.

Q: Why are St. Johns rates lower than South Florida in 2026?

A: Three reasons. First, newer construction stock — most St. Johns townhomes are post-2010, built to modern wind and fire codes that South Florida''s older inventory doesn''t match. Second, the 30-year wind-loss history per policy is lower on the First Coast. Third, since HB 837 passed in 2023, 17 new admitted carriers have re-entered Florida personal lines, and several are actively competing on newer-construction North Florida risks because the loss ratios are favorable. The net effect is 10 to 15 percent lower premium on a comparable townhome.

Q: If I move from an HO-6 to an HO-3 mid-policy, does my mortgage company need to approve it?

A: They need to be notified, not technically approve. Most mortgages require "evidence of insurance" — proof you have a policy that meets the loan''s minimum coverage and the carrier rating. Moving from HO-6 to HO-3 on a fee-simple home actually increases coverage (you''re now insuring the structure, not just the contents), so the lender''s evidence-of-insurance requirement is more, not less, satisfied. Send a Certificate of Insurance from the new policy to the loan-servicing department within 5 business days of binding.

Q: Does the HOA''s flood insurance apply to my unit, or do I need my own private flood?

A: Depends on your community structure. If you''re in a true fee-simple townhome (Silverleaf, Shearwater, most of Nocatee), the HOA almost never carries flood coverage on the home — it''s your responsibility. If you''re in a condo-structured townhome (some Beachwalk and Beacon Lake phases), the HOA''s master policy may include building-level NFIP flood up to the federal cap, but contents and interior finishes are still yours. Pull a flood quote regardless — St. Johns flood risk varies dramatically by elevation and proximity to drainage features. Private flood typically prices below NFIP for newer construction.

Related Reading

- Does the HOA Cover Exterior Walls and Roofs? The Townhome Maintenance Boundary Decoded — The companion deep-dive on the maintenance-boundary side of the same question.

- How to Lower Your Condo HOA Insurance in Duval County: The 2026 Market Guide — If your community is actually a condominium, the Duval-specific market guide applies — and St. Johns associations face similar dynamics.

- Small Building, Big Deadlines: The 2026 Survival Guide for 25-50 Unit Condo Boards — Boutique condo board guide if your townhome community is on the small-condo side of the line.

How Atesa Risk Advisors Can Help

Print the worksheet first → Download the St. Johns Townhome Identity Audit Worksheet. Two pages: the 7-step audit checklist plus the community-by-community master policy table with the Loss Assessment exposure math.

Atesa is a Florida independent insurance brokerage that runs identity audits on St. Johns townhome policies every week — we know the master policy quirks of every major Nocatee, Silverleaf, Shearwater, Beacon Lake, and Beachwalk phase, and we have access to the 17 new admitted carriers actively quoting newer-construction townhomes in 2026.

If you just bought a townhome in St. Johns and you''re not 100 percent sure whether your current policy form matches your deed, the audit takes a single phone call. Worst case, your current policy is correct and we save you a renewal cycle. Best case, we catch a wall-in gap before the next storm and rebuild the policy on the correct form with an admitted-market carrier, plus document the assessable exposure your HOA structure creates.

Just bought a townhome in St. Johns and not sure your policy is right? Get your free identity audit and quote consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Florida Office of Insurance Regulation, Homeowners and Condo Form Comparison Reference (HO-3 vs HO-6 form definitions and Florida-specific endorsements) — floir.com

[2] Citizens Property Insurance Corporation, 2026 Condo and Townhome Underwriting Manual — master policy deductible benchmarks for St. Johns / First Coast — citizensfla.com

[3] Insurance Information Institute (III), Homeowners and Condo Insurance Form Overview — iii.org

[4] Florida House Bill 815 (2024) — Property Insurance, roof-age non-renewal protections — flsenate.gov/Session/Bill/2024/815

[5] Florida House Bill 837 (2023) — Civil Remedies / tort reform — flsenate.gov/Session/Bill/2023/837

[6] Florida Statute Chapter 720 — Florida Homeowners Association Act — leg.state.fl.us/statutes/720

[7] Florida Statute 718.111(11) — Condominium master-policy insurance requirements — leg.state.fl.us/statutes/718.111

[8] Florida Building Code 8th Edition (2023) — Class A fire-rated roof and wind-mitigation specifications — floridabuilding.org

External Resources for St. Johns County townhome owners:

- St. Johns County Clerk of Court — Online Records — Pull your recorded deed and confirm legal description (fee-simple vs condominium)

- Florida Office of Insurance Regulation Company Search — Verify carrier admitted status and financial-stability ratings

- Florida Department of Financial Services — Division of Consumer Services — Complaints and carrier license verification. Hotline: 1-877-693-5236

- Nocatee Community Association — Nocatee CC&Rs and HOA master-policy reference

- Citizens Property Insurance Corporation — Florida insurer of last resort benchmark for St. Johns townhomes

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. Ricardo has audited and rebuilt townhome insurance programs for Nocatee, Silverleaf, Shearwater, Beacon Lake, and Beachwalk homeowners since the post-Ian carrier exits began in 2022.