How to Lower Commercial Property Insurance in Duval County: The 2026 Market Guide

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 13, 2026

Key Takeaways

- Duval County commercial property rates are softening for the first time in over a decade — admitted carriers are pricing 10 to 18 percent under the 2024 surplus-lines market [1][2].

- 17 new admitted (state-licensed and regulated) commercial property carriers have re-entered Florida since HB 837 tort reform passed in March 2023, and several are actively quoting Jacksonville office, retail, and industrial buildings [1][6].

- If your building''s Insurance to Value (ITV) — the dollar amount you are insured for — was set during the 2023 construction-cost spike, you are likely paying premium on a replacement cost that has fallen 8 to 12 percent in 2026 [3].

- Moving from a surplus-lines policy to an admitted-market policy removes Florida''s 5 percent surplus lines tax (FS 626.932) on top of the lower base premium — a direct lift to Net Operating Income (NOI) [4].

- Pre-2017 buildings in Downtown, San Marco, and Riverside need Ordinance or Law coverage at 25 percent of Coverage A or higher to cover the code-upgrade costs the City of Jacksonville will require after any covered loss [5].

Commercial property insurance in Jacksonville, FL is finally coming off the 2022–2024 crisis peak, and most Duval County building owners can lower their 2026 premium by 10 to 18 percent without changing a single thing about the building itself. The savings come from three places: a refreshed ITV against current Jacksonville construction costs, a switch from the surplus-lines market back to the admitted (state-licensed) market that is now actively writing Duval, and a clean audit of Ordinance or Law, flood, and portfolio-credit gaps that snuck into policies during the crisis years.

If you are the CFO, asset manager, or owner of a commercial building in Downtown, San Marco, Riverside, the Southside / Town Center, or the JAXPORT-adjacent industrial corridor, this guide is the audit framework we run for clients every week in 2026. The downloadable CFO''s Audit Worksheet at the bottom is the 60-second version your team can walk through during a renewal call.

The market shift is real. Florida-domiciled and national admitted carriers have re-entered the state at a pace not seen since before Hurricane Irma, and the Jacksonville commercial book — historically less-targeted than South Florida — is now competitive. The 2026 question for most Duval owners is not "can I get coverage?" — it is "am I leaving 10 to 18 percent of my premium on the table?"

How to lower commercial property insurance in Duval County in 2026

The five red flags below are the audit categories that decide your premium outcome. Each maps to a specific dollar movement on your dec page. Run them in order — the same order our brokerage runs them on every Duval commercial submission.

Download the printable worksheet → CFO''s Insurance Audit Worksheet (PDF). Two pages: the 10-item audit checklist and the surplus-vs-admitted comparison grid with portfolio-credit math.

Red Flag #1 — Your asset is valued at 2023 inflation peaks (ITV bloat)

Insurance to Value, or ITV, is the dollar amount your building is insured for — basically, are you insured for what it actually costs to rebuild today. In 2023 and 2024, Jacksonville construction costs spiked dramatically: lumber, steel, concrete, and skilled labor all moved together as supply chains broke and Florida absorbed post-Ian and post-Idalia rebuilds. Most Duval commercial dec pages set during that window locked in replacement-cost numbers at the peak.

The 2026 reality is that Jacksonville supply chains have stabilized. RSMeans Construction Cost Data (the industry-standard construction-pricing database, published quarterly) is showing Duval averages 8 to 12 percent below the 2023–2024 peak [3]. If your dec page is still priced against the peak, you are paying premium against a replacement cost that no longer exists in the market.

The 60-second ITV math:

`` Target Coverage = (Total Sq Ft × 2026 Construction Index) − Foundational Exclusions ``

A 40,000 sq ft Jacksonville office building at the 2026 Duval average of $265/sq ft works out to a $10.6M target replacement cost. If your dec page reads $12M (priced from 2023 inputs at roughly $300/sq ft), you are paying premium against $1.4M of inflated value — a 13 percent premium overcharge that compounds every year you renew without rechecking.

Foundational exclusions — slab, footings, below-grade utility runs — generally represent 8 to 12 percent of total replacement cost and are not destroyed in most covered losses. A current 2026 appraisal will subtract these properly.

What to do: Order a 2026 replacement-cost appraisal before any renewal quote. Most Jacksonville commercial appraisers turn one around in 7 to 14 days. The savings on the next renewal typically pay for the appraisal in the first month.

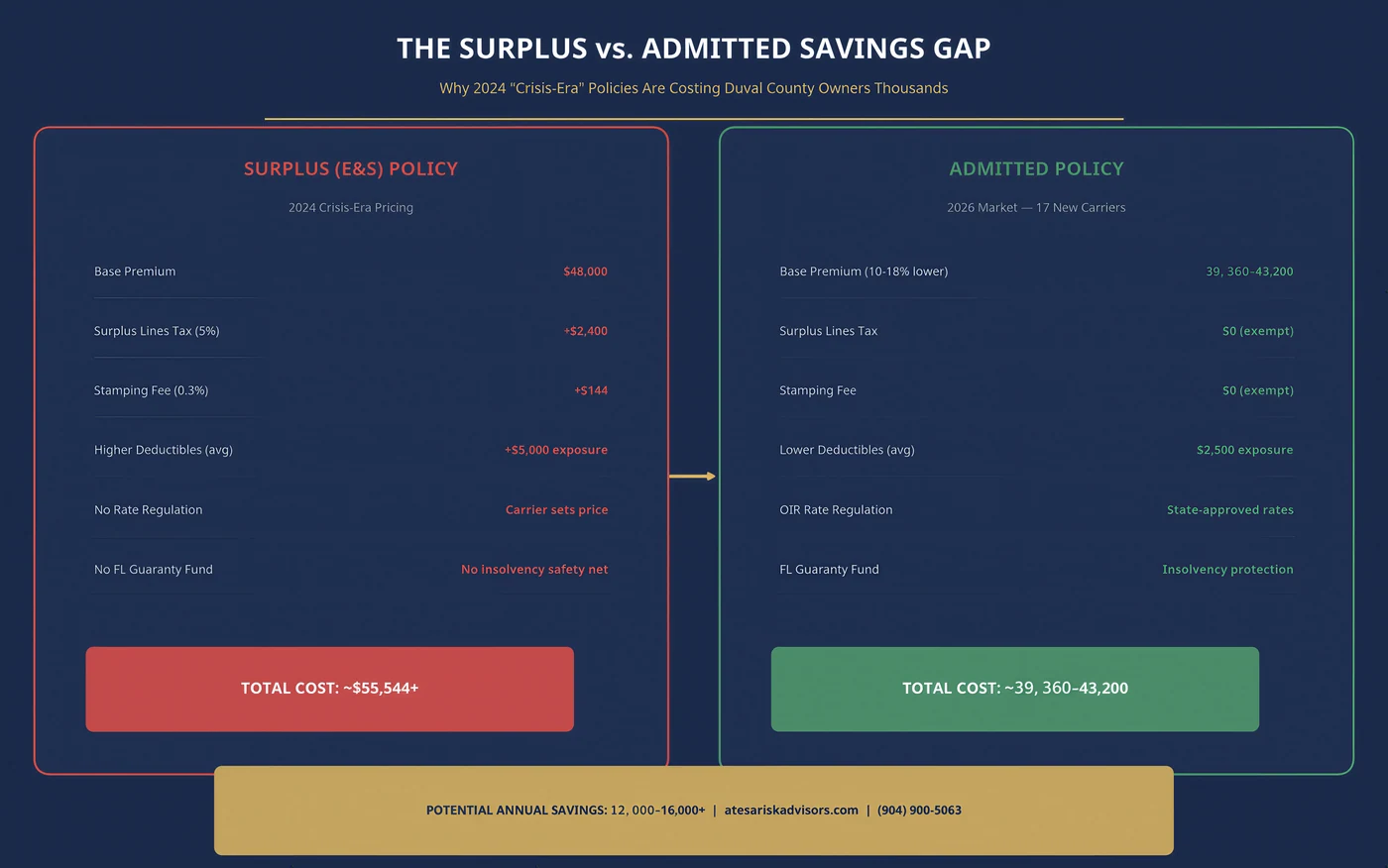

Red Flag #2 — You are still stuck in the surplus-lines market

During the 2022–2024 crisis, many Jacksonville office, retail, and industrial buildings were pushed out of the admitted market and into the E&S — Excess & Surplus, the specialty market for hard-to-place risks — because admitted carriers simply stopped quoting Florida commercial property. Surplus lines policies kept buildings insured but came with two costs: a higher base premium, and the 5 percent Florida Surplus Lines Tax under FS 626.932 [4].

In 2026, this picture has flipped. Seventeen admitted carriers — state-licensed insurers regulated by the Florida Office of Insurance Regulation, whose claims are backstopped by Florida''s guaranty fund — have re-entered the Florida commercial property market since HB 837 passed in March 2023 [1][6]. Several are specifically targeting Duval office, warehouse, and retail accounts in the $1M to $25M TIV range.

Why moving from surplus to admitted matters for your P&L:

- Lower base premium. Admitted carriers are pricing Duval commercial property at $5.60–$6.90 per $1,000 of TIV (inland office) versus surplus-market 2024 rates of $6.80–$8.40 — a 14 to 18 percent reduction.

- No 5 percent surplus lines tax. Florida charges a 5 percent tax on every surplus-lines premium. Admitted policies pay 0 percent. On a $100,000 premium, that''s a $5,000 line item that disappears at the binding desk.

- Florida guaranty fund protection. If an admitted carrier becomes insolvent, the Florida Insurance Guaranty Association covers claims up to statutory limits. Surplus lines carriers are not covered by FIGA.

- Easier loan compliance. Most commercial loan covenants require admitted-market coverage above certain TIV thresholds. If you''ve added debt since the crisis, your lender may be quietly auditing this at the next refinancing.

What to do: Ask your broker — in writing — whether your current carrier is admitted or surplus, and request three admitted-market quotes at renewal. The shopping process takes 14 to 21 days from clean submission to bound policy.

Red Flag #3 — Missing Ordinance or Law in historic sub-markets

If you own commercial property in Downtown Jacksonville, San Marco, Riverside, Avondale, or Springfield, this red flag is the most expensive one to miss. The Florida Building Code 8th Edition (2023) — adopted by the City of Jacksonville for all permitted rebuilds — requires meaningful code upgrades for pre-2017 buildings damaged in a covered loss [5].

The trap: a standard commercial property policy only pays to put the building back the way it was before the loss. If a fire destroys 30 percent of a 1960s Riverside office building and the City of Jacksonville requires you to install a $50,000 sprinkler system, $30,000 of ADA-compliant entryways, and $40,000 of impact-rated glazing on the rebuild to meet current code, you are out of pocket for $120,000 — unless you have Ordinance or Law coverage.

Ordinance or Law has three parts (industry calls them Coverage A, B, and C of the endorsement, separate from your main Coverage A on the policy):

- Coverage A — Loss to undamaged portion. Pays to demolish parts of the building that survived the loss but cannot be reused under current code.

- Coverage B — Demolition cost. Pays the cost of demolishing the undamaged portion (separate from the rebuild).

- Coverage C — Increased cost of construction. Pays the extra cost to rebuild to current code (the sprinklers, ADA, impact glass, updated electrical).

The 2026 benchmark for Duval pre-2017 buildings: Ordinance or Law at 25 percent of Coverage A (the main building limit) is the floor. For Downtown, San Marco, and Riverside buildings 40+ years old, 50 percent is the right number. The premium add for going from 10 percent (crisis-era default) to 25 percent is typically 2–4 percent of total premium — pennies against six-figure code-upgrade exposure.

What to do: Pull your dec page. Find the Ordinance or Law line. If it reads 10 percent of Coverage A, request a re-quote with 25 percent and 50 percent options. The math almost always favors the higher limit.

Red Flag #4 — Relying on NFIP for Riverside and downtown commercial flood

FEMA''s National Flood Insurance Program (NFIP) is the federal flood program that covers most residential properties and many commercial buildings up to $500,000 of building coverage and $500,000 of contents. For most Duval commercial owners, that limit is no longer enough — and NFIP''s commercial rates have surged under FEMA''s Risk Rating 2.0 reform.

The 2026 alternative: the private flood market is now offering meaningfully better terms for Jacksonville commercial property. Key advantages:

- Higher limits. $5M, $10M, or $25M building coverage available — versus NFIP''s $500K commercial cap.

- Lower premium for elevated buildings. If your Riverside or Downtown property is elevated above the St. Johns River flood plain (BFE — Base Flood Elevation, the FEMA-set water height that defines flood zones), private flood typically prices 20 to 40 percent below NFIP for the same coverage.

- Replacement cost on contents. NFIP commercial contents coverage is actual cash value (depreciated). Private flood policies offer replacement cost.

- Business income (Loss of Rents). NFIP commercial flood does not include business income. Private flood commonly does — critical for income-producing real estate.

- Faster claims. Private flood claims close in 30 to 60 days on average. NFIP claims commonly take 90 to 180 days.

One caveat: If your loan covenants specifically require NFIP coverage, you may need to stack a private "excess flood" policy on top of NFIP rather than replacing it. Talk to the broker before unwinding NFIP.

What to do: Get a private flood quote alongside your NFIP renewal quote. The comparison is usually decisive for buildings above the St. Johns River BFE — which includes most Downtown and Riverside commercial inventory.

Red Flag #5 — Not leveraging portfolio credits across multiple Duval assets

If you own more than two commercial properties in Duval (or anywhere on the First Coast), portfolio credits are the 2026 lever most owners are not pulling. Several admitted carriers re-entering Florida in 2026 have filed new portfolio-credit programs that discount premium by 4 to 8 percent when three or more locations are bound under a single master commercial policy.

The math on a typical Duval portfolio:

- Premium pool today: $180,000 across 3 separate office or retail assets on 3 different carriers.

- Move to a single master commercial policy with a portfolio credit (4–8 percent filed in 2026): savings of $7,200 to $14,400 per year.

- Operational side benefit: one renewal date, one set of declarations, one COI (Certificate of Insurance — the proof-of-coverage doc your tenants, lenders, and vendors request) request workflow. Accounting and asset-management teams typically save 30+ hours per year on insurance administration.

Portfolio credits are not "automatic." Your broker has to specifically request the credit, document the locations on a schedule, and place the package with a carrier whose 2026 filings include the credit. Of the 17 admitted carriers re-entering Florida, roughly 9 have a portfolio program filed as of Q2 2026 [1].

What to do: If you own three or more Duval assets, ask your broker to quote a single master policy with portfolio credit. If they cannot identify which 2026 carriers have the credit filed, get a second opinion.

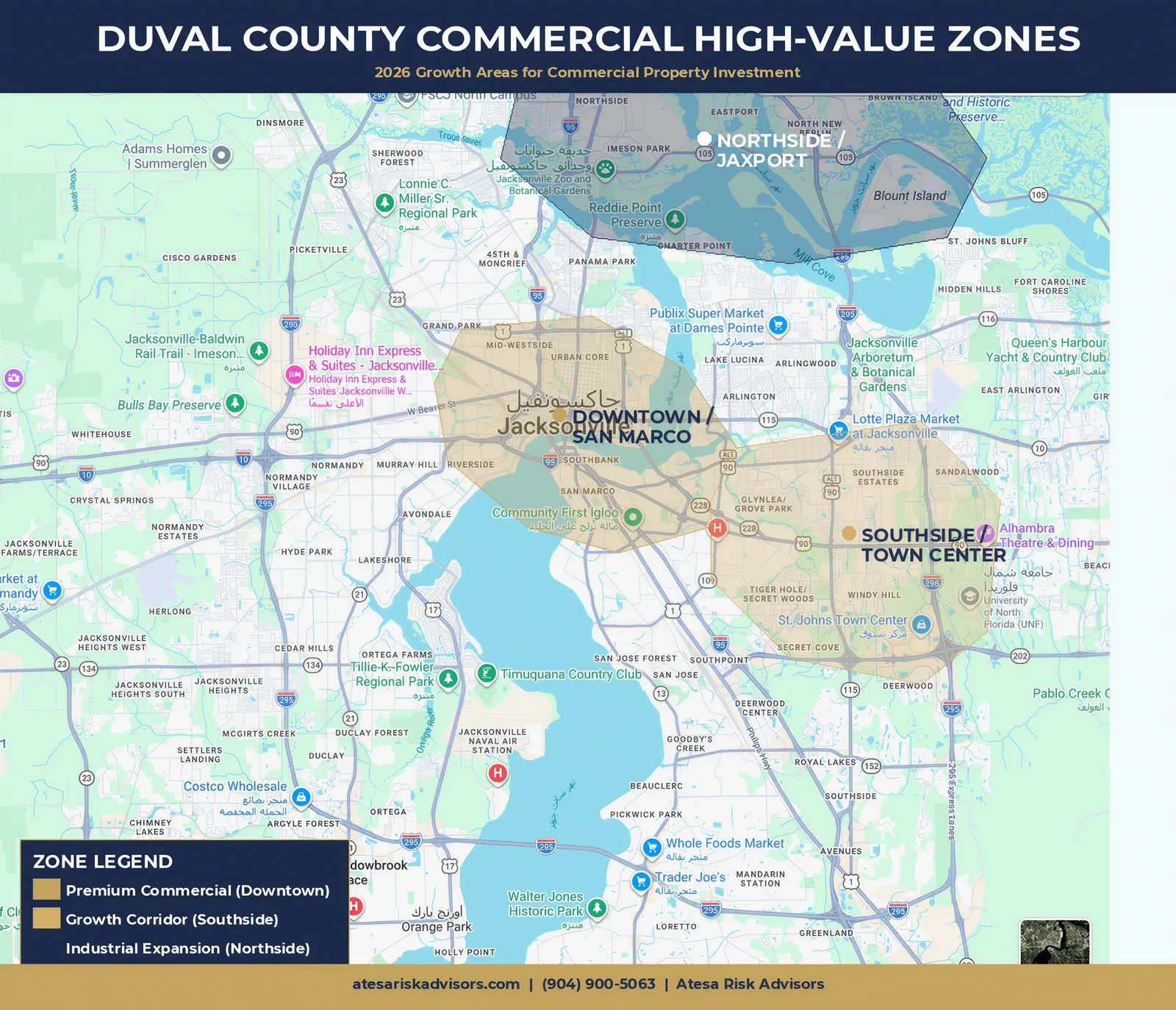

Duval sub-market focus: where 2026 capacity is concentrated

Not every Jacksonville sub-market is equally easy to place in 2026. Carrier appetite varies by zone, building age, occupancy, and flood exposure.

Strongest carrier appetite (most quotes per submission in Q2 2026):

- Southside / Town Center. Newer Class A and B office, mixed-use, and retail. Admitted carriers favor post-2017 construction and updated wind-mitigation features.

- JAXPORT / Northside industrial corridor. Warehouse, distribution, and light-manufacturing in the post-2010 industrial parks near the port. Strong appetite, especially when sprinkler-protected.

- Mandarin and Beaches retail / mixed-use. Updated Class B retail centers with FEMA-current flood elevation certificates.

Selective appetite (fewer quotes, but pricing competitive when accepted):

- Downtown Jacksonville office. Pre-1980s historic stock requires Ordinance or Law, current 4-point inspections, and clean loss runs. Pricing is competitive for well-maintained buildings.

- Riverside / Avondale / San Marco. Older retail and mixed-use with St. Johns flood exposure. Private flood market is the lever here.

Specialty market (E&S or hybrid placements typically required):

- Coastal Mayport / Atlantic Beach commercial. Wind PML (Probable Maximum Loss) drives the decision; well-mitigated buildings still place admitted with higher deductibles.

- Buildings with open claims or named-storm losses in the last 24 months. Almost always a specialty placement until the claim closes.

Decision matrix: surplus-era policy vs 2026 admitted-market quote

This table is the side-by-side most CFOs need to see to understand the spread. Numbers are typical Duval commercial property ranges; your file may price tighter or wider depending on building age, occupancy, and loss history.

| Cost element | 2024 surplus policy | 2026 admitted policy | Change |

|---|---|---|---|

| Premium per $1,000 TIV (inland office) | $6.80–$8.40 | $5.60–$6.90 | −14% to −18% |

| Premium per $1,000 TIV (coastal Jax Beach) | $11.50–$14.20 | $9.60–$11.50 | −12% to −16% |

| Wind deductible (Duval inland) | 5% of TIV | 2–3% of TIV | Lower retained loss |

| Ordinance or Law (% of Coverage A) | 10% (or excluded) | 25–50% available | Stronger form |

| Florida Surplus Lines Tax | 5% of premium (FS 626.932) | 0% (admitted = no tax) | Direct NOI lift |

| NFIP vs Private Flood (commercial) | NFIP $500K cap | Private $5M+ available | Broader limits |

| Loss of Rents sub-limit | 12 months typical | 18–24 months available | Stronger BI |

| Portfolio credit (3+ Duval assets) | Rarely filed | 4–8% filed in 2026 | New savings |

| Florida Guaranty Fund backing | Not covered | Covered (FIGA) | Insolvency protection |

What we''re seeing on Duval submissions in 2026

"Nine out of ten Duval commercial files I audit in 2026 are still priced like it''s late 2023. The owner remembers the renewal letter that doubled their premium two years ago, and they assumed the market never came back. It did. The same building we placed at $7.40 per thousand in 2024 surplus is binding at $5.90 per thousand admitted in 2026 — and the dec page is genuinely better. The work is showing up at the renewal call, not waiting for the renewal letter."

— Ricardo Alonso, Founder, Atesa Risk Advisors

Florida-Specific Considerations

Florida Statute 627.0629 — rate filings. All commercial property rate changes by an admitted carrier must be filed with the Florida Office of Insurance Regulation. You can verify any carrier''s most recent rate filing through the OIR rate-filing database. This is why the 2026 rate softening is auditable — the filings are public [4].

Florida Statute 626.913–932 — Surplus Lines Law. This is the statutory framework for the 5 percent surplus lines tax and the rules governing E&S placement. The single biggest 2026 line-item win for most Duval commercial owners is moving out of surplus and stopping that 5 percent tax [4].

Florida Statute 627.351(6) — Citizens depopulation. Citizens Property Insurance Corporation''s commercial-non-residential account is shrinking by statute. If any admitted private carrier offers your account at a rate within 20 percent of Citizens'', Citizens is required to non-renew you. For most 2026 Duval commercial owners, this is not the binding constraint — the admitted market is now offering pricing 10–18 percent below Citizens anyway [1].

Florida Building Code 8th Edition (2023). Adopted by the City of Jacksonville for all permitted commercial work. Triggers the Ordinance or Law exposure that makes the Red Flag #3 audit so financially important for any pre-2017 building [5].

HB 837 (March 2023) — tort reform. Modified comparative negligence, repealed one-way attorney fees for property claims, and tightened the bad-faith framework. This is the legislative reason the 17 new admitted carriers have re-entered Florida commercial property in 2026 [6].

Your 7-Step Duval Commercial Property Audit Timeline

| Step | Days | What happens |

|---|---|---|

| 1. Pull the current dec page and 5-year loss runs | Day 1 | Confirm TIV, carrier type (admitted vs surplus), Ordinance or Law %, wind deductible %, sub-limits |

| 2. Order a 2026 replacement-cost appraisal | Days 2–14 | Florida licensed commercial appraiser; cite RSMeans Jacksonville construction-cost data |

| 3. Sign one Agent of Record (AOR) letter exclusively with one broker | Day 8 | Multi-broker shopping triggers carrier blocks; one broker, two-week exclusive |

| 4. Submit to 3+ admitted carriers, private flood, and a Citizens benchmark | Days 9–21 | Include scheduled portfolio if 3+ Duval assets |

| 5. Compare total cost — premium + deductible + Ordinance or Law + flood + tax | Days 22–28 | Lowest premium is not always lowest total cost |

| 6. Verify lender / loan covenant compliance for the chosen quote | Days 29–32 | Admitted-market requirement, AM Best / Demotech rating, additional-insured wording |

| 7. Bind, issue COIs, update the Schedule of Insurance to the lender / property manager | Days 33–45 | New effective date matches or precedes prior expiration; no coverage gap |

FAQ for Duval commercial property owners

Q: How often should I recheck my building''s ITV in 2026?

A: At every renewal, at minimum. In a market where construction costs are still settling (2026 is the first year of stabilization after a 2-year spike), the right cadence is a fresh appraisal every 18 to 24 months and a desktop ITV check at every renewal. Buildings that haven''t been re-appraised since 2022 or 2023 are almost certainly overinsured.

Q: I''m currently in the E&S surplus market. How fast can I move to an admitted carrier?

A: Most clean Duval commercial submissions can move from surplus to admitted in 30 to 60 days once a complete package (dec page, 5-year loss runs, recent appraisal, current 4-point inspection if applicable) is in front of the broker. The constraint is rarely carrier appetite in 2026 — it''s the time to gather documentation. Buildings with open claims or named-storm losses in the last 24 months may need to stay in the specialty market until the claims close.

Q: What''s the right Ordinance or Law sub-limit for a 1970s Downtown Jacksonville office building?

A: 50 percent of Coverage A is the right number for pre-1980 historic Downtown stock. Pre-2017 buildings (the Florida Building Code threshold) should carry 25 percent at minimum. The 10 percent default that crisis-era policies often used will not cover the code-upgrade costs the City of Jacksonville will require on any meaningful rebuild — sprinklers, ADA-compliant entryways, impact-rated glazing on storefronts, updated electrical.

Q: Should I drop NFIP commercial flood coverage if private flood offers better terms?

A: Usually — but check your loan covenants first. Many commercial loans were written with explicit NFIP requirements before private flood became widely available. If the loan requires NFIP, the right play is to keep a minimum NFIP policy and stack private "excess flood" on top for the higher limits and broader form. If the loan is silent on NFIP specifically, you can usually replace NFIP entirely with private flood.

Q: Does the EMR (Workers Compensation Experience Modifier) affect my commercial property premium?

A: Not directly — EMR is a Workers Comp variable. But if you''re shopping a BOP (Business Owners Policy that bundles property + general liability + business income) or a commercial package that includes Workers Comp, an out-of-date or inflated EMR can drag the whole package''s pricing. Audit your EMR every mod-year (typically annually); a single incorrect classification or unreported claim can leave a high mod in place years after the actual loss closes.

Q: What''s the hurricane / wind deductible benchmark for a Duval inland building vs a coastal one?

A: Inland Duval (Downtown, Southside, San Marco, Riverside, Mandarin) — target 2 to 3 percent of TIV in the 2026 admitted market. Coastal Duval (Jacksonville Beach, Atlantic Beach, Mayport, Ponte Vedra) — 3 to 5 percent is typical. Buildings with wind-mitigated construction (impact-rated openings, secondary water resistance, modern roof-to-wall attachment documented on an OIR-B1-1802 inspection form) can sometimes price tighter, especially in the admitted market.

Q: If I own four Duval commercial properties, what''s the portfolio credit math worth in 2026?

A: On a $200,000 to $300,000 combined annual premium pool, portfolio credits filed in 2026 typically save $8,000 to $24,000 per year (4 to 8 percent). The bigger benefit is operational: one master policy with one renewal date, one schedule of locations, and one COI workflow. Accounting and property-management teams typically reclaim 30+ hours per year on insurance administration after consolidation.

Q: Will my lender accept a 2026 admitted-market carrier they haven''t seen before?

A: Almost always yes, as long as the carrier carries an AM Best or Demotech financial-stability rating that meets the loan covenant threshold (typically AM Best A− or better). Several of the 17 new admitted carriers entering Florida in 2026 are subsidiaries of nationally-rated parents. Provide the lender with the AM Best rating in writing before the binding decision; this clears 95 percent of lender objections.

Related Reading

- How to Lower Your Condo HOA Insurance in Duval County: The 2026 Market Guide — The Duval-specific market overview for condo associations, with parallel ITV and master-policy audit logic.

- Got Non-Renewed in Jacksonville? Your 30-Day Replacement Playbook (2026) — The companion piece if your current commercial carrier has just non-renewed you.

- 5 Insurance Mistakes Florida Business Owners Make — The annual-review checklist that catches the audit gaps before they cost six figures.

- The June 1st Countdown: Is Your Jacksonville Business Sitting on a $250,000 Liability? — Deductible buyback wrap to convert a six-figure Named Storm deductible into a $5k-$10k flat retention before the May 25 binding-window deadline.

How Atesa Risk Advisors Can Help

Print the worksheet first → Download the CFO''s Insurance Audit Worksheet. Two pages: the 10-item audit checklist plus the surplus-vs-admitted comparison grid with portfolio-credit math.

Atesa is a Florida independent insurance brokerage that runs commercial property audits for Duval County asset managers, CFOs, REITs, and owner-operators every week. We work the admitted, surplus, and Citizens markets in parallel — and we run the same 10-item audit you''ll find on the worksheet on every submission, before any quote is requested.

If your 2026 renewal is in the next 90 days, the highest-leverage move is to get the audit done before the renewal letter lands. A 2026 replacement-cost appraisal, a refreshed wind-mit form, and a market plan from a broker who knows which of the 17 new admitted carriers will quote your sub-market is the difference between a flat renewal and a 10 to 18 percent premium reduction.

Owning Duval commercial property in 2026? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Florida Office of Insurance Regulation, Property Insurance Stability Report 2025 and 2026 commercial rate filings — floir.com

[2] Florida OIR Quarterly Commercial Market Report (Q2 2026) — Duval / First Coast aggregate carrier and rate data

[3] RSMeans Construction Cost Data 2026 — Jacksonville, FL Building Construction Cost Index (Gordian / RSMeans, the industry-standard construction-cost reference)

[4] Florida Statute 626.913–932 — Surplus Lines Law and 5% surplus lines tax — leg.state.fl.us/statutes/626.913; FS 627.0629 — Florida commercial property rate filings — leg.state.fl.us/statutes/627.0629

[5] Florida Building Code 8th Edition (2023) — adopted by the City of Jacksonville for permitted commercial work — floridabuilding.org

[6] Florida House Bill 837 (2023) — Civil Remedies / tort reform — flsenate.gov/Session/Bill/2023/837

[7] Citizens Property Insurance Corporation — Commercial-Non-Residential Account Reports and 2026 depopulation filings — citizensfla.com

[8] FEMA National Flood Insurance Program (NFIP) — Risk Rating 2.0 commercial methodology — fema.gov/flood-insurance

External Resources for Duval commercial property owners:

- Florida Office of Insurance Regulation Company Search — Verify carrier admitted status and financial-stability ratings before binding

- JAX Chamber of Commerce — Jacksonville business community resources and commercial real-estate market intelligence

- Duval County Clerk of Courts — Public records for property deeds, liens, and tax data

- City of Jacksonville Building Inspection Division — Florida Building Code permit and inspection records

- Citizens Commercial Programs — Benchmark Citizens rates and depopulation requirements

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. Ricardo has placed and audited commercial property insurance for Jacksonville-area office, retail, warehouse, and mixed-use owners through both the 2022–2024 hard market and the 2026 admitted-carrier re-entry.