How to Lower Your Condo HOA Insurance in Duval County: The 2026 Market Guide

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 7, 2026

Key Takeaways

- Citizens (Florida's state-backed insurance carrier of last resort) approved an 8.7% rate cut for Duval County multi-peril condo policies effective 2026 — the first meaningful reduction since the 2022 reform package [1].

- 17 new admitted carriers (private insurers licensed and regulated by the state, with claims backed by Florida's guaranty fund) have entered the Florida property market since SB 2-A in 2022, and many are targeting Jacksonville first because the First Coast has lower hurricane exposure than South Florida [2].

- Well-maintained Duval associations are reporting 12–20% premium reductions in 2026 by completing the Structural Integrity Reserve Study (SIRS) early and challenging stale 2024 replacement-cost numbers [3][4].

- The SIRS deadline is December 31, 2026, under Florida Statute 718.112(2)(g) — boards that finish early are now getting "preferred risk" credits at renewal [4].

- The "Beach vs. River" split inside Duval is real: a Jax Beach high-rise can pay 2x to 3x more per $1,000 of insured value than a comparable San Marco or Riverside building, almost entirely because of wind exposure [5].

Jacksonville condo associations should expect to lower their 2026 master-policy premium by 12–20% if they audit three things: their carrier (Citizens vs. private market), their SIRS report, and their replacement-cost number. Most Duval boards we audit in 2026 are paying 2024 crisis-era rates on a market that has already moved. The savings are no longer hypothetical — Citizens' 8.7% rate cut [1] and 17 new admitted carriers [2] mean a Jacksonville building can usually find a better policy in less than 90 days.

If you serve on a Duval condo board, you've spent the last three years writing checks for a market that priced every Florida building like it was sitting on the beach in Miami. That's finally over — but only for the boards that actively go shopping. Citizens and the new private carriers don't lower your premium automatically; you have to ask, and you have to bring proof.

This guide walks through the five specific moves that are working for Jacksonville, Jax Beach, Atlantic Beach, San Marco, and Riverside associations right now. Every number cited is from a Florida-filed rate document, statute, or the carriers themselves — no industry-blog math.

Beyond Citizens: Why Jacksonville Is the "First Choice" for New Carriers

The 17 new private insurers that entered Florida after the 2022–2023 reforms aren't writing in Miami first. They're writing in Jacksonville first [2], and the reason is geography.

Duval County sits in wind-zone Tier 2 to Tier 3 for most non-coastal areas — the Florida Office of Insurance Regulation (FOIR) treats Jacksonville's hurricane exposure as meaningfully lower than Miami-Dade or Broward. Translation: when a new carrier wants to ease into the Florida market without front-loading hurricane risk, they ask their underwriters to "open Duval first."

That gives Jacksonville associations leverage no other Florida market has right now. Specifically:

- Lower minimum deductibles. Many new admitted carriers are quoting Duval condos at a 2% wind deductible, where Citizens still defaults to 5% on the same building.

- Better Ordinance or Law coverage. This is the part of the policy that pays the extra cost of rebuilding to current Jacksonville building code after a loss — important for any building completed before the 2017 code update. The new carriers commonly include 25–50% Ordinance or Law as standard; older Citizens policies often capped it at 10%.

- No surcharge on multi-peril ("all risk") forms. Citizens has historically priced multi-peril higher to push associations toward simpler wind-only policies. The private market doesn't.

The Move: If your association is still on Citizens, you are likely paying a "Loyalty Tax." Citizens' own glide-path rules mean that once a private admitted carrier offers you a comparable policy within 20% of Citizens' premium, Citizens is required to non-renew you anyway. Most Duval boards never see that letter because their broker hasn't actively shopped the new entrants. A 2026 audit moves you off Citizens onto an admitted carrier with better deductibles and stronger coverage — usually at the same price or slightly less.

We also recommend confirming the new carrier's financial-stability rating (Demotech or AM Best) before binding. Florida's reform was real, but a few of the new entrants are still capitalizing — your broker should show you the current rating in writing.

Using Your SIRS Report as a Negotiating Tool

The SIRS — short for Structural Integrity Reserve Study, basically a 30-year repair budget that the state now requires for older Florida condos — has a hard deadline of December 31, 2026 under Florida Statute 718.112(2)(g) [4]. Most Duval boards we talk to view the inspection as a cost. In 2026, the smart play is to flip it: turn the SIRS into a renewal credit.

Underwriters at the new admitted carriers are now offering what they call a "preferred risk credit" for associations that:

- Have already completed the SIRS (not "scheduled" — actually delivered).

- Have a funded reserve plan showing the dollars are being collected per the study's schedule.

- Have board minutes documenting that capital projects identified by the study are either underway or budgeted.

Carriers don't publish this credit on their rate filings, but it commonly shows up as a 5–12% discount on the wind-and-property portion of premium — sometimes more on buildings older than 30 years.

The mental model an underwriter uses looks like this:

`` Premium Discount = Base Rate × (Actual Reserves / Target SIRS Reserves) × Safety Factor ``

In plain English: the closer your reserve account is to what the SIRS says it should be, the bigger the discount you can negotiate. A board that has funded 80% or more of its SIRS target gets the maximum credit; one at 30% may get a smaller discount or none at all. Boards under 30% are now seeing the opposite — surcharges or non-renewals.

If your SIRS isn't done yet, the practical move is to schedule it now and ask for a conditional renewal quote that locks in the credit once the report is delivered. Several Jacksonville carriers will hold the rate for 60–90 days while you finish.

The "Beach vs. River" Wind Mitigation Strategy

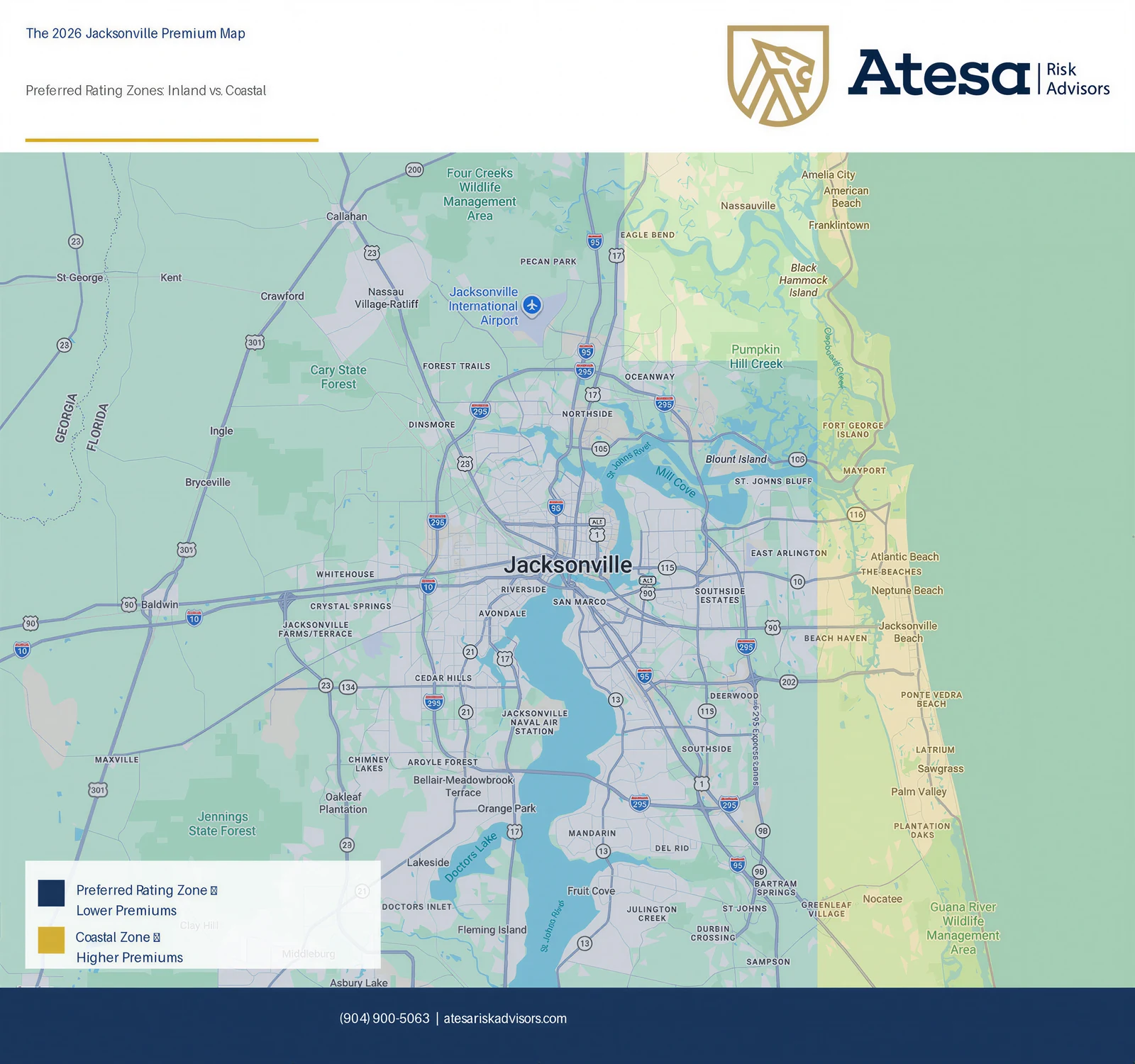

The 2026 Jacksonville Premium Map — preferred rating zones run along the St. Johns River and inland; coastal Duval (Jax Beach, Atlantic Beach, Neptune Beach) carries higher wind premiums.

Inside Duval County the wind picture splits hard between coastal and inland buildings. A condo in San Marco, Riverside, or Avondale along the St. Johns River prices very differently than a comparable building in Jax Beach, Atlantic Beach, or Neptune Beach — sometimes 2x to 3x per $1,000 of insured value [5].

That's why the Wind Mitigation Inspection — Florida's standard form OIR-B1-1802 — is the single highest-leverage document an inland Duval association can produce. The inspection scores how well the roof and walls resist hurricane wind, and the credits it unlocks can be enormous.

Two rules of thumb for Jacksonville:

- Make sure your wind-mit form is less than 12 months old. Most carriers won't honor an OIR-B1-1802 dated more than a year out at renewal. We see Duval boards lose 15–25% in earned credits every year just because the inspection lapsed.

- Audit "Roof-to-Wall" attachment specifically. This is the one line item on the form that moves the most premium. If your form shows "toe-nails" but the building has actually been retrofitted with hurricane straps or clips, the credit difference can be thousands per year per association. A licensed inspector can re-document the upgrade for a few hundred dollars.

For coastal associations (Jax Beach, Atlantic Beach, Ponte Vedra-adjacent), the wind-mit form matters even more — but you also need to confirm that secondary water resistance and opening protection (impact-rated windows or shutters) are documented on the latest form. These two items alone can shift a Jax Beach building from a "Tier 1 high-risk" rate to a "Tier 1 mitigated" rate.

For wind-zone questions specific to your address, the City of Jacksonville Building Inspection Division maintains the local code records and can confirm your building's compliance history.

Red Flag: Is Your Building Over-Insured Based on 2024 Costs?

In 2023 and 2024, Florida construction costs spiked. Carriers responded by raising the replacement-cost number — the dollar amount your policy is built to rebuild — on virtually every Florida condo. Many Duval boards never re-checked that number, so they're still paying 2024 prices on a market that has cooled.

This is the Insurance to Value problem — or ITV, basically the question of "are you insured for what it actually costs to rebuild today, not last year's panic-pricing." Two things have changed in Jacksonville since the 2024 peak:

- Construction labor and materials have stabilized. The big 2023–2024 spike (driven by post-Idalia and post-Ian demand) has flattened out across the First Coast.

- Local appraisers are pricing 2026 rebuilds 5–12% lower per square foot than 2024 quotes for the same building type. The Duval County Property Appraiser publishes year-over-year reconstruction-cost data through duvalpa.com.

Here's what that means in dollars: if your building is insured at $350 per square foot because that was the 2024 number, but a 2026 appraisal pegs the rebuild at $310 per square foot, you are paying premium on $40/sf of insurance you can't actually use. On a 100-unit, 1,200-sf-per-unit building, that's $4.8 million of phantom Total Insured Value — usually translating to $8,000–$15,000/year in unnecessary premium.

The fix is simple: get an updated 2026 replacement-cost appraisal before your renewal and ask the carrier to re-rate the building at the lower TIV. Most carriers will do it without re-underwriting if the appraisal comes from a recognized firm.

What we see in the field — Ricardo Alonso

"About one in three Duval associations we audit in 2026 are over-insured by 8% or more. The board feels safer with a higher number, but you can't collect more than what it costs to rebuild — so the extra premium is just gone. Bring the TIV in line with reality and you keep the same coverage for less money."

— Ricardo Alonso, Founder, Atesa Risk Advisors

2024 Crisis Rates vs. 2026 Market Rates: Duval County

Before-and-after for a typical 80–120 unit Duval condo, master multi-peril policy. The 2024 numbers are pulled from Citizens' filed rates and FOIR market data; the 2026 numbers reflect what well-maintained admitted-market associations are actually binding this year [1][2][3].

| Coverage element | 2024 typical (Duval) | 2026 typical (Duval) | Change |

|---|---|---|---|

| Citizens base rate (multi-peril) | Reference baseline | −8.7% approved cut | Lower [1] |

| Wind deductible (private admitted) | 5% of TIV common | 2–3% of TIV common | Lower out-of-pocket |

| Ordinance or Law coverage | 10% of Coverage A | 25–50% of Coverage A | Stronger coverage |

| Average premium per $1,000 TIV (inland Duval) | ~$5.20–$6.80 | ~$4.40–$5.50 | 12–20% reduction |

| Average premium per $1,000 TIV (coastal Duval) | ~$9.00–$13.00 | ~$8.00–$11.50 | 8–14% reduction |

| New admitted carriers in market | ~3 actively quoting Duval | 17+ actively quoting Duval | Bigger market [2] |

| SIRS preferred-risk credit available | Not yet filed | 5–12% on wind/property | New in 2026 [4] |

Numbers are typical ranges; your association's actual quote depends on building age, claims history, wind-mit score, and reserve health.

The 2026 Duval Condo Insurance Audit Checklist

Walk the next board meeting through these 10 questions. Any "no" answer is a place where money is leaking. Skip the ones that don't apply to your building.

- [ ] Is our current carrier a "new entry" to Florida (admitted post-2022)?

- [ ] Have we requested a Citizens vs. private-market comparison quote in the last 90 days?

- [ ] Does our policy include Ordinance or Law at 25% of Coverage A or higher?

- [ ] Is our wind mitigation inspection (OIR-B1-1802) less than 12 months old?

- [ ] Has the board reviewed roof-to-wall attachment documentation for hidden credits?

- [ ] Is our SIRS report completed (or scheduled to finish before December 31, 2026)?

- [ ] Are reserves funded at 80%+ of the SIRS target — and is that documented in board minutes?

- [ ] Has the Total Insured Value been updated against a 2026 (not 2024) appraisal?

- [ ] Does the policy carry secondary water resistance and opening protection credits where applicable?

- [ ] Is our broker showing us at least three quotes per renewal, including admitted-market alternatives?

Need a printable version for your next board meeting? Grab the Jacksonville Board-Room Cheat Sheet (PDF) — a 2-page Treasurer's prep sheet covering this checklist plus the 2024-vs-2026 rate-comparison table and what to demand from your broker at renewal.

Florida-Specific Considerations

- FS 718.111(12) — defines the master policy that the association is required to carry on the building shell, common areas, and shared amenities.

- FS 718.112(2)(g) — the Structural Integrity Reserve Study (SIRS) requirement, with the December 31, 2026 deadline that's driving the preferred-risk credits described above [4].

- FS 553.899 — the Milestone Inspection requirement (a separate engineering inspection for buildings 25+ years old, or 30+ if more than 3 miles from the coast) [4].

- HB 1021 (2024) — the 2024 update that tightened reserve funding rules and increased board accountability for SIRS compliance.

- Citizens Property Insurance Corporation 2026 rate filings — published rate documents that show the approved 8.7% Duval reduction [1].

- Florida Office of Insurance Regulation (FOIR) Property Insurance Stability Report — annual report tracking the new admitted carriers, market capacity, and county-level rate movement [2].

Your 6-Step Duval Audit Timeline

The whole process, from "pull last year's policy" to "bind a new admitted-market quote," typically runs 60–90 days. Here's the order of operations.

| Step | Action | Typical Time | Why It Matters |

|---|---|---|---|

| 1 | Pull current policy and renewal letter | 1 day | You can't audit what you can't read line-by-line. |

| 2 | Order an updated 2026 replacement-cost appraisal | 7–14 days | Sets the correct Total Insured Value before quoting. |

| 3 | Confirm the wind mitigation form (OIR-B1-1802) is under 12 months old | 1–3 days | A current form unlocks every other credit. |

| 4 | Document SIRS status and reserve funding percentage | 3–7 days | Required for the 5–12% preferred-risk credit at renewal. |

| 5 | Request quotes from at least three admitted-market carriers (plus Citizens for benchmark) | 14–21 days | The 17 new entrants don't all quote every building — broad shopping is the leverage. |

| 6 | Bind the best total-cost policy (premium + deductible + endorsements) | 5–7 days | Lowest premium isn't always lowest total cost — compare deductibles and Ordinance or Law together. |

FAQ for Duval Treasurers and Board Members

Q: How much can my Duval condo association realistically save on 2026 insurance?

A: Most well-maintained Jacksonville associations are seeing 12–20% reductions on their 2026 master-policy premium when they audit three things — the carrier (Citizens vs. private market), the wind mitigation form, and the replacement-cost number. Coastal buildings (Jax Beach, Atlantic Beach) save a smaller percentage but a larger dollar amount because their starting premium is higher.

Q: What is a "preferred risk credit" and how do we qualify?

A: It's a discount that several new admitted carriers are now offering associations that have completed their Structural Integrity Reserve Study (SIRS) and are funding reserves at 80%+ of the study's target. It typically shows up as a 5–12% reduction on the wind-and-property portion of premium. Boards that have only "scheduled" the SIRS don't qualify — the report has to be delivered and the funding has to be documented in board minutes.

Q: We're with Citizens — can we just stay there since they cut rates 8.7%?

A: You can, but Citizens' own rules require non-renewal once a private admitted carrier offers you comparable coverage within 20% of Citizens' premium. With 17 new entrants now actively quoting Duval, that letter is increasingly common — and once it arrives, your renewal options shrink fast. The smarter play is to shop the private market proactively while you still have the choice.

Q: Our SIRS isn't done yet. Is it too late to get the credit?

A: No, but you need to schedule the inspection now. Several Jacksonville carriers will hold a renewal rate for 60–90 days while you finish, and they'll apply the preferred-risk credit retroactively once the report is delivered. The hard cutoff is the December 31, 2026 statutory deadline — boards that miss it face surcharges or non-renewals, not just lost credits.

Q: How is a Jax Beach condo priced differently than a San Marco condo?

A: Wind exposure is the biggest difference. A coastal Jax Beach or Atlantic Beach building can pay 2x to 3x per $1,000 of insured value compared to an inland San Marco or Riverside building of the same age and quality. The mitigation moves are the same — make sure the wind-mit form is current, confirm roof-to-wall attachment credits, and document opening protection — but the dollars at stake are larger on the coast.

Q: Should we drop our Ordinance or Law coverage to save money?

A: Almost never in Duval. Many Jacksonville buildings predate the 2017 Florida Building Code update, which means a covered loss requires rebuilding to current code — and the extra cost (impact glass, updated electrical, ADA upgrades) is exactly what Ordinance or Law pays for. Cutting it is one of the most expensive "savings" a board can choose.

Q: How often should the board shop insurance?

A: Every year, 90 days before renewal. Florida's market is changing fast in 2026, and the carrier offering the best rate today often isn't the one that was best last year. A board that shops every renewal averages 5–8% better pricing over time than one that auto-renews.

Q: What documents should we have ready before requesting quotes?

A: At minimum: the current declarations page, the most recent OIR-B1-1802 wind mitigation form, the SIRS report (or proof it's scheduled), the most recent reserve funding statement, the latest 4-point inspection if the building is over 25 years old, and a 5-year claims history. Brokers can pull most of this for you, but having it in one folder before quoting cuts the timeline by 2–3 weeks.

Q: Our broker says "Citizens is the only option in Duval." Is that still true in 2026?

A: It hasn't been true since 2024 and it's emphatically not true in 2026. Seventeen new admitted carriers are quoting Duval condos, and several of them are quoting better coverage than Citizens at lower deductibles. If your broker isn't showing you private-market alternatives, the audit-first move is finding a broker who actively works the new admitted market.

Related Reading

- SIRS Compliance or Non-Renewal? The 2026 Board Member's Guide to Structural Reserves — deep dive on the SIRS requirement, what underwriters look at, and how to avoid the non-renewal trap.

- Small Building, Big Deadlines: The 2026 Survival Guide for 25-50 Unit Condo Boards — the playbook for smaller Duval associations that don't have a full-time property manager.

- 5 Red Flags Your Association is Overpaying for Insurance in 2026 — the audit signals that show up first when a board starts shopping the new admitted market.

Related Reading

- How to Lower Your Condo HOA Insurance in Collier County: The 2026 Post-Ian Market Guide — the Gulf Coast counterpart for Naples, Marco Island, and inland Collier boards navigating the post-Ian admitted market.

- Got Non-Renewed in Jacksonville? Your 30-Day Replacement Playbook (2026) — Day-by-day worksheet if your Duval commercial policy was just non-renewed.

- How to Lower Commercial Property Insurance in Duval County: The 2026 Market Guide — The CFO audit for Duval office, retail, and industrial buildings — 10-18% rate softening in 2026.

- Townhome or Condo? Solving the St. Johns County Insurance Identity Crisis (2026) — The Nocatee / Silverleaf / Shearwater audit for HO-3 vs HO-6 mismatch — most common 2026 gap for new townhome owners.

How Atesa Risk Advisors Can Help

Atesa Risk Advisors is an independent Jacksonville insurance brokerage. We hold direct appointments with 40+ A-rated admitted Florida carriers — including most of the 17 new entrants writing Duval condos in 2026 — plus Citizens and the Florida-specialty markets that don't sell direct to consumers. For Duval associations that means we don't pick a carrier first and shop the policy second; we shop every quoting carrier on every renewal and bring the best three to your board for the decision.

We're local: our office is in Jacksonville and we handle Duval, St. Johns, Clay, and Nassau county associations directly. See our Jacksonville insurance page for how we serve the First Coast. We work with boards, property managers, and individual unit owners in English, Spanish, and Portuguese, and our typical Duval audit takes 30–45 days from "send us your current policy" to "here are your three best 2026 options."

Want a free 2026 First Coast Market Analysis on your master policy? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Citizens Property Insurance Corporation. 2026 Rate Filings — Multi-Peril Condominium Master Policy, Duval County. citizensfla.com/media-resources (2026 Rate Kit). Accessed 2026.

[2] Florida Office of Insurance Regulation. Property Insurance Stability Report — 2026 Edition. floir.com/home/property-insurance-stability-report.

[3] Florida Office of Insurance Regulation. County-Level Property Insurance Premium Trends, 2024–2026. floir.com.

[4] Florida Statutes 718.112(2)(g) — Structural Integrity Reserve Study, including the December 31, 2026 deadline. leg.state.fl.us/statutes.

[5] Florida Office of Insurance Regulation. Wind Mitigation Credits and Coastal Tier Rating Factors, 2026. floir.com.

[6] HB 1021 (2024) — Florida condominium reform act, board accountability and reserve funding rules. flsenate.gov/Session/Bill/2024/1021.

[7] National Association of Insurance Commissioners (NAIC). Property/Casualty Market Conditions Report — Florida, 2026. naic.org.

External Resources for Duval Condo Boards:

- Citizens Property Insurance Corporation — current rate filings and renewal forms

- Florida Office of Insurance Regulation (FOIR) — market reports and consumer complaints

- Duval County Property Appraiser — building records and replacement-cost data

- City of Jacksonville Building Inspection Division — local code records and Milestone Inspection guidance

- Florida Department of Business and Professional Regulation — Division of Florida Condominiums — state-level board education and complaint process

If your board is ready to act, compare the market for condo & HOA insurance in Jacksonville with an independent broker who shops your master policy across 40+ Florida carriers.

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency based in Jacksonville. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. He has reviewed 200+ Duval County condo and HOA master policies across the post-2022 reform cycle and works directly with First Coast boards on annual audits and renewal strategy.