How to Lower Your Condo HOA Insurance in Collier County: The 2026 Post-Ian Market Guide

By Ricardo Alonso, Founder, Atesa Risk Advisors · May 8, 2026

Key Takeaways

- Citizens (Florida's state-backed insurance carrier of last resort) approved a 3.4% reduction on Collier County multi-peril condo policies for 2026 — the first meaningful rate relief for the post-Ian Gulf Coast market since the 2022 reform package [1].

- Hurricane Ian (September 2022, Category 4) drove $50+ billion in insured losses across Southwest Florida, and Collier replacement-cost numbers reset 25–40% higher at the 2023–2024 peak. Many Naples and Marco Island boards are now under-insured at 2022 valuations rather than over-insured at 2024 ones — a coverage mismatch unique to the post-Ian Gulf Coast market [2][3].

- Roughly 6–9 new admitted carriers are actively quoting Collier condos in 2026 — enough to break Citizens' near-monopoly on the SW Florida coastal market for the first time since Hurricane Ian [2].

- The Structural Integrity Reserve Study (SIRS) deadline is still December 31, 2026 under Florida Statute 718.112(2)(g), and post-Ian underwriters are now offering preferred-risk credits of 6–14% to boards with completed studies and reserves funded above 75% of target [4].

- The "Coastal vs. Inland" split inside Collier is the largest in Florida: a Marco Island or Old Naples high-rise can pay 3x to 4x more per $1,000 of insured value than a comparable building in inland Naples Park, Lely, or Golden Gate Estates [5].

Collier County condo associations should expect to lower their 2026 master-policy premium by 8–18% if they handle three things in the right order: confirm their replacement-cost number is current (most are stale), force a Citizens vs. private-market quote-off, and document SIRS plus reserve health for the post-Ian preferred-risk credit. Most Naples and Marco Island boards we audit in 2026 are still paying 2023 panic-pricing on a Gulf Coast market that has finally started to stabilize. The percentage savings vary by building, but the dollar amount per unit is often substantial — coastal Collier carries some of the highest premiums in Florida, so even a single-digit percentage cut can save a 100-unit building tens of thousands of dollars annually.

If you serve on a Collier condo board, you've spent the three years since Hurricane Ian writing checks for a market that priced every Gulf Coast building like the next storm was already named. That's loosening — but only for boards that bring proof of three things to the renewal table: a current replacement-cost appraisal, a delivered SIRS report, and reserves that show the building is being maintained, not just insured.

This guide walks through the specific moves working for Naples, Marco Island, Bonita Springs (Collier side), Pelican Bay, Old Naples, and inland Collier associations right now. Every number cited is from a Florida-filed rate document, statute, or carrier source — not industry-blog math.

The Post-Ian Reality: Where Collier Actually Sits in 2026

Hurricane Ian made landfall September 28, 2022 as a Category 4 with sustained winds of 150 mph. The Florida Office of Insurance Regulation tracked $50+ billion in insured losses across Southwest Florida — making it the costliest weather event in Florida history and the second-costliest in U.S. history [2].

Three years later, Collier's insurance market still looks different from the rest of the state:

- Citizens market share is high. When private carriers retreated from coastal Southwest Florida after Ian, Citizens absorbed most of the risk. As of late 2025, Citizens still writes a meaningful share of Naples and Marco Island multi-peril condo master policies — well above Citizens' statewide average [1].

- Premium per $1,000 of insured value is among the highest in Florida — coastal Collier pricing routinely runs 2x to 3x the rate of lower-risk inland Florida counties for comparable buildings. The 20th Judicial Circuit, the Tier 1 wind zone, and the post-Ian storm-claim history all stack against Collier on the rate filing.

- The new admitted carriers entering Florida since the 2022–2023 reforms are quoting Collier more cautiously. Roughly 6–9 are actively writing coastal Collier condos in 2026 — meaningful competition compared to the "Citizens or nothing" reality of 2023, even if the post-Ian roster remains smaller than the rosters quoting lower-risk inland Florida markets.

The good news: the trend lines have flipped. Citizens' approved 3.4% reduction for 2026 multi-peril condo class [1] is the first cut since the 2022 reforms, and the new entrants are starting to undercut Citizens on inland Collier (Lely, Naples Park, Golden Gate Estates) by 5–12% on the same building. Coastal pricing remains elevated, but the market is no longer monolithic.

The Move: If your association received a Citizens depopulation offer in 2024 or 2025, don't dismiss the next one as "just a marketing letter." Citizens' depopulation rules require non-renewal once a private admitted carrier offers comparable coverage within 20% of Citizens' premium. With 6–9 entrants now quoting Collier, that letter shows up at more renewals every quarter — and once it does, your shopping window is short.

The Wind-Only vs. Multi-Peril Decision (A Coastal Collier Choice You Probably Didn't Know You Had)

This is a coastal SW Florida question. Inland Florida boards rarely face it because the inland market quotes multi-peril ("all-risk") master policies as a matter of course. In Collier — and especially in Naples, Marco Island, and Bonita Springs — many associations have been steered into a two-policy stack: a Citizens wind-only policy plus a separate non-Citizens carrier for everything except wind (fire, water, theft, liability).

This split exists because Citizens historically refused to write the non-wind portion in coastal SW Florida. The new admitted entrants in 2026 are increasingly willing to write the full multi-peril package as one policy. The trade-offs:

- Two-policy stack (current setup for many Collier condos): Predictable Citizens wind pricing, but two sets of deductibles, two sets of forms, two claim processes after a storm, and a real risk that your two carriers point at each other when a loss spans both perils.

- Single multi-peril admitted policy (the 2026 alternative): One deductible structure, one claims contact, one set of endorsements. Often 5–10% lower total cost than the stacked version, plus better Ordinance or Law (the part of the policy that pays the extra cost of rebuilding to current Florida Building Code after a covered loss — important for any Collier building completed before the 2017 code update).

The decision isn't automatic. A few of the new entrants will only write multi-peril once you can show a current SIRS report, reserves above 75% of target, and an updated 2026 replacement-cost appraisal. But for boards that can produce those three documents, consolidating to a single admitted-market multi-peril policy is the single highest-leverage move available on the 2026 renewal.

Are You *Under-*Insured? The Post-Ian ITV Reset

This is the section where the Collier story diverges sharpest from the rest of Florida.

Insurance to Value — or ITV, basically the question of "are you insured for what it actually costs to rebuild today?" — is usually a problem of over-insurance in Florida right now. Construction costs spiked in 2023–2024, carriers raised replacement-cost numbers, and most boards are now paying premium on phantom value.

In Collier, the math often runs the other way. Hurricane Ian crushed the SW Florida construction labor pool, drove materials shortages from Naples to Cape Coral, and pushed actual rebuild costs 25–40% above the 2022 valuations many associations are still locked into [3]. Two specific risks to check:

- Your TIV is locked at 2022 numbers. If your board hasn't ordered a fresh replacement-cost appraisal since Ian, you may be insured for 70–80 cents on the dollar. After a covered total loss, that gap is paid by the unit owners through special assessment — not the carrier.

- Your TIV was raised in 2024 but the construction market has since cooled. Some Collier carriers spiked TIV by 30%+ during the 2023–2024 peak. The market has stabilized in 2026, and a new appraisal often pulls the number down 5–10% from the 2024 peak — closer to actual current rebuild cost.

The fix is the same in either direction: order a 2026 replacement-cost appraisal from a recognized Florida firm and ask the carrier to re-rate the policy at the corrected TIV. The Collier County Property Appraiser publishes year-over-year reconstruction-cost data through collierappraiser.com, which is a useful sanity-check on whatever number your appraiser delivers.

What we see in the field — Ricardo Alonso

"About one in four Collier associations we audit in 2026 are under-insured — usually because the board never reset TIV after Ian and is still operating on a 2021 or 2022 valuation. The premium savings from staying low feel real until you read FS 627.7011 on the rebuild gap. We'd rather see a board pay an extra 4% on premium and avoid a six-figure special assessment after the next storm."

— Ricardo Alonso, Founder, Atesa Risk Advisors

SIRS and Reserve Health: From Compliance Burden to Renewal Discount

The SIRS — short for Structural Integrity Reserve Study, basically a 30-year repair budget the state now requires for older Florida condos — has a hard deadline of December 31, 2026 under Florida Statute 718.112(2)(g) [4]. In Collier the post-Ian carriers care about this even more than the rest of Florida — and for a clear reason.

After Ian, underwriters watched well-maintained Collier buildings ride out 150 mph winds with manageable damage, while older buildings with deferred maintenance lost roofs, glass, and entire mechanical systems. Reserve health predicted that pattern almost perfectly: buildings with current SIRS reports and reserves above 75% of target showed materially lower claim frequency and severity [4]. That's not a marketing claim; it's the reason post-Ian carriers are now writing the credit into their rate filings.

The credit shows up as a 6–14% discount on the wind-and-property portion of premium for Collier condos that can produce three documents:

- A delivered SIRS report (not "scheduled" — actually completed by a Florida-licensed engineer or architect).

- A funded reserve plan showing dollars are being collected at or above the study's schedule.

- Board minutes documenting that capital projects from the SIRS are either underway or budgeted.

A useful mental model:

`` Premium Discount = Base Rate × (Actual Reserves / Target SIRS Reserves) × Safety Factor ``

In plain English: the closer your reserve account is to what the SIRS says it should be, the bigger the discount you can negotiate. Collier underwriters have actually moved the threshold lower than the rest of the state — 75% funding qualifies for the credit in Collier, versus the 80%+ threshold most carriers apply elsewhere [4]. They want to reward the Gulf Coast boards that have done the work post-Ian.

If your SIRS isn't done yet, the practical move is to schedule it now and ask your broker for a conditional renewal quote that locks in the credit once the report is delivered. Several Collier-quoting carriers will hold rates for 60–90 days while you finish.

The Citizens Depopulation Letter — and What to Do When It Arrives

Citizens has been aggressively reducing its Collier footprint since 2024. The mechanism is called "depopulation": when a private admitted carrier signals interest in a Citizens policy, Florida law requires Citizens to offer the policyholder a take-out option — and once that letter arrives, the clock starts.

What to do when (not if) you receive one:

- Don't auto-decline. Many Collier boards we audit dismissed depopulation offers because the take-out carrier was unfamiliar. By the next renewal cycle, Citizens' rules required non-renewal anyway — and the alternative carriers offering quotes had reduced their interest in the building.

- Ask your broker to verify the take-out carrier's A.M. Best or Demotech rating in writing. A few of the new admitted entrants are still capitalizing. The reform was real, but rating quality varies.

- Compare total cost — not just premium. A take-out carrier offering Citizens' premium plus 15% but with a 2% wind deductible (versus Citizens' 5%) is often the better total-cost decision after you map out a hypothetical $5M loss.

- Don't lose your Ordinance or Law coverage in the swap. Citizens' older policies often capped Ordinance or Law at 10% of Coverage A. If the take-out carrier offers 25%+ as standard, that's a real coverage upgrade, not a downgrade.

- Document the decision in board minutes. If the board ultimately accepts or rejects the take-out, get it on the record — it matters for D&O coverage and for future renewals.

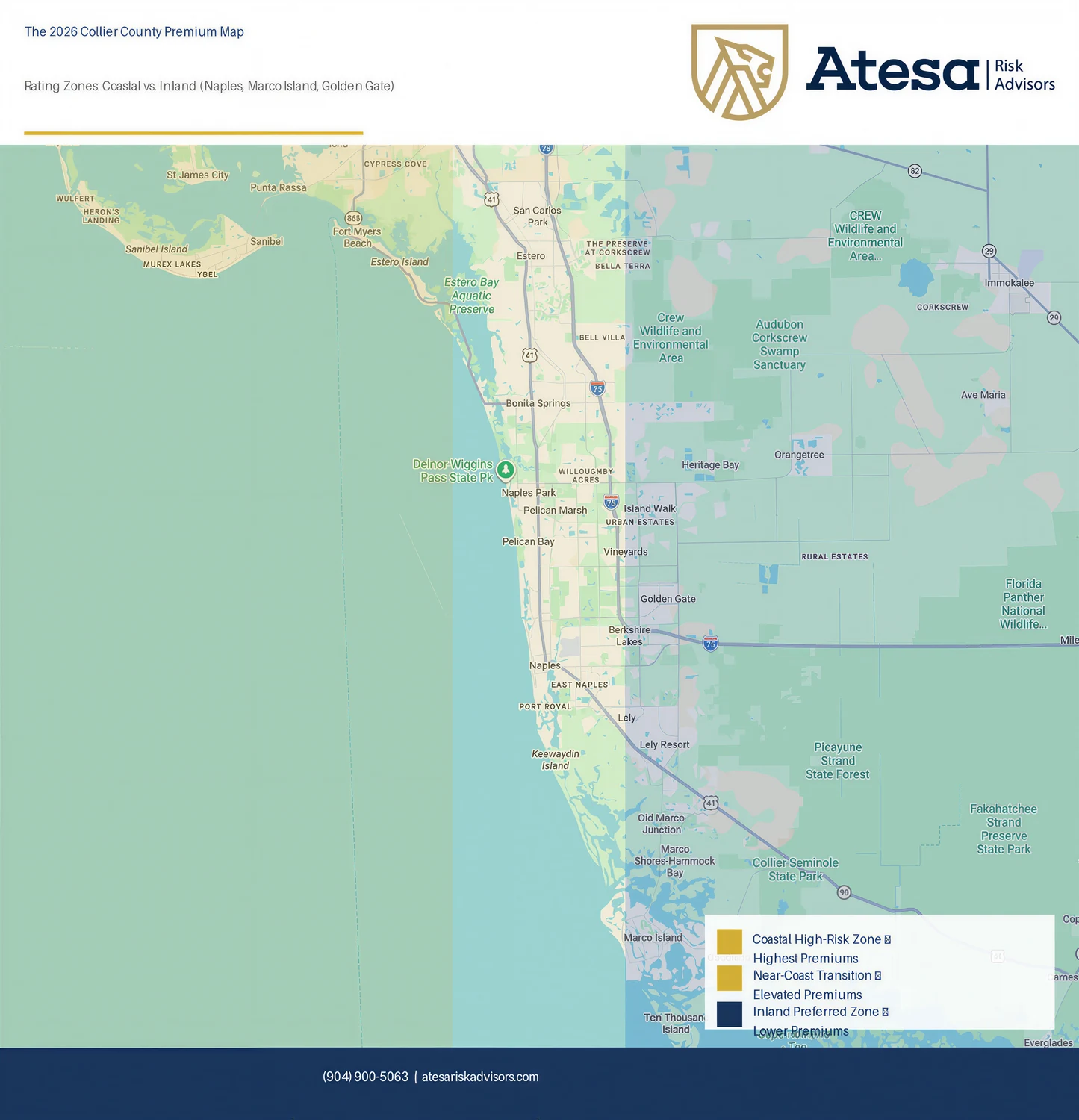

The Naples vs. Marco vs. Bonita Wind Tier Map

The 2026 Collier County Premium Map — coastal high-risk zones (Marco Island, Old Naples, Park Shore, Pelican Bay, North Naples beachfront) carry the highest wind premiums; inland preferred zones (Naples Park east, Lely, Golden Gate Estates, Immokalee) drop into a lower-cost rating tier.

Inside Collier the wind picture splits harder than anywhere else in Florida — and the cost gap between the coast and inland is the widest in the state.

A typical 100-unit master policy on Marco Island Gulf-front runs $22–$32 per $1,000 of insured value in 2026. A comparable building 3 miles inland in Lely or Naples Park runs $10–$14 per $1,000 — a 2x to 3x difference for the same square footage and age [5]. That gap is almost entirely driven by:

- Wind tier classification. Coastal Collier sits in Tier 1 hurricane wind zone with a Florida Building Code design wind speed of 170–180 mph. Inland Collier drops into Tier 2 or Tier 3.

- Storm surge zone. Coastal Collier is in FEMA flood Zone VE or AE; inland Collier is mostly Zone X. Flood is a separate policy, but storm-surge exposure influences wind-policy underwriting too.

- Construction age. Many Marco Island and Old Naples high-rises pre-date the 1992 (post-Andrew) and 2002 (HVHZ) building code updates. Newer Naples Park and Lely buildings are built to current code from day one.

The practical move for any Collier association — coastal or inland — is the Wind Mitigation Inspection (Florida's standard form OIR-B1-1802). The inspection scores how well the roof and walls resist hurricane wind, and the credits it unlocks can be enormous, especially for buildings retrofitted post-Ian.

Two rules of thumb:

- Make sure the form is less than 12 months old at renewal. Most carriers won't honor an OIR-B1-1802 dated more than a year out. We see Collier boards lose 15–30% in earned credits every year just because the inspection lapsed.

- Document post-Ian retrofits specifically. Roof-to-wall attachment upgrades (hurricane straps or clips), impact-rated glazing, opening protection, and secondary water resistance — many Collier buildings did this work in 2023–2024 but never updated the wind-mit form. A licensed inspector can re-document the upgrade for a few hundred dollars and unlock thousands per year in credits.

For wind-zone questions specific to your Collier address, the Collier County Building Review and Permitting division maintains the local code records and can confirm your building's compliance history.

2024 Crisis Rates vs. 2026 Market Rates: Collier County

Before-and-after for a typical 80–120 unit Collier condo, master multi-peril policy. The 2024 numbers reflect Citizens' filed rates and FOIR market data; the 2026 numbers reflect what well-maintained admitted-market associations are actually binding this year [1][2][3].

| Coverage element | 2024 typical (Collier) | 2026 typical (Collier) | Change |

|---|---|---|---|

| Citizens base rate (multi-peril) | Reference baseline | −3.4% approved cut | Lower [1] |

| Wind deductible (Citizens) | 5–10% of TIV | 5–10% of TIV | Unchanged |

| Wind deductible (admitted entrants) | 5–7% of TIV | 3–5% of TIV | Lower out-of-pocket |

| Ordinance or Law coverage | 10% of Coverage A | 25–50% of Coverage A | Stronger coverage |

| Premium per $1,000 TIV (inland Collier) | ~$11.50–$15.50 | ~$10.00–$14.00 | 8–12% reduction |

| Premium per $1,000 TIV (coastal Collier) | ~$24.00–$34.00 | ~$22.00–$32.00 | 4–8% reduction |

| New admitted carriers in market | ~2 quoting Collier | 6–9 actively quoting Collier | Bigger market [2] |

| SIRS preferred-risk credit available | Not yet filed | 6–14% on wind/property | New in 2026 [4] |

| Single multi-peril policy availability | Rare on coast | Increasing — 4–6 entrants offer it | Better simplicity |

Numbers are typical ranges; your association's actual quote depends on building age, claims history, wind-mit score, distance from coast, and reserve health.

The 2026 Collier Condo Insurance Audit Checklist

Walk the next board meeting through these 10 questions. Every "no" is a place where money is leaking — or where the building is exposed without coverage.

- [ ] Is our replacement-cost appraisal dated 2026 (not 2022, not 2024)?

- [ ] Have we received a Citizens depopulation letter in the last 18 months — and how did the board respond?

- [ ] Is our policy a single multi-peril form, or are we still on a wind-only + non-wind split?

- [ ] Does our policy include Ordinance or Law at 25% of Coverage A or higher?

- [ ] Is our wind mitigation form (OIR-B1-1802) less than 12 months old?

- [ ] Has the board documented post-Ian retrofits (straps, glazing, opening protection) on the latest wind-mit form?

- [ ] Is our SIRS report delivered (or finishing before December 31, 2026)?

- [ ] Are reserves funded at 75%+ of the SIRS target — and is that documented in board minutes?

- [ ] Have we requested at least three competing 2026 quotes — Citizens benchmark plus admitted-market alternatives?

- [ ] Has the board verified the A.M. Best or Demotech rating of any non-Citizens carrier proposed before binding?

Need a printable version for your next board meeting? Grab the Collier Board-Room Cheat Sheet (PDF) — a 2-page Treasurer's prep sheet built specifically for Naples, Marco Island, Bonita Springs, and inland Collier. Covers this checklist plus the 2024-vs-2026 Collier rate-comparison table, post-Ian retrofit documentation, the Citizens depopulation playbook, and exactly what to demand from your broker at renewal.

Florida-Specific Considerations

- FS 718.111(12) — defines the master policy the association is required to carry on the building shell, common areas, and shared amenities.

- FS 718.112(2)(g) — the SIRS requirement, with the December 31, 2026 deadline that's driving Collier's preferred-risk credits.

- FS 553.899 — the Milestone Inspection requirement (a separate engineering inspection for buildings 25+ years old, or 30+ if more than 3 miles from the coast). Most coastal Collier high-rises trigger the 25-year threshold by default.

- FS 627.7011 — Florida's replacement-cost statute, which governs what the carrier owes after a covered total loss. The under-insurance risk discussed above lives in this statute.

- HB 1021 (2024) — the 2024 condo reform act tightening reserve funding rules and increasing board accountability for SIRS compliance.

- Citizens Property Insurance Corporation 2026 rate filings — published rate documents that show the approved 3.4% Collier multi-peril reduction [1].

- Florida Office of Insurance Regulation Property Insurance Stability Report — annual report tracking new admitted carriers, market capacity, and county-level rate movement post-Ian [2].

The 20th Judicial Circuit (Collier, Lee, Charlotte, Glades, Hendry) handles condo-related liability disputes; jury-award severity in the 20th has been moderate post-2023 reform, but board-of-directors litigation has trended up after Ian-related claim disputes.

Your 6-Step Collier Audit Timeline

The full process — from "pull last year's policy" to "bind a new admitted-market 2026 policy" — typically runs 75–105 days for Collier associations — longer than the inland Florida average because the post-Ian admitted market requires more documentation before quoting and fewer carriers will quote without it.

| Step | Action | Typical Time | Why It Matters |

|---|---|---|---|

| 1 | Pull current policy, renewal letter, and any Citizens depopulation correspondence | 1 day | Sets the baseline. Read the dec page line by line — wind deductible, Ordinance or Law %, separate wind/non-wind structure. |

| 2 | Order an updated 2026 replacement-cost appraisal | 10–18 days | Critical in Collier where the post-Ian range can swing TIV either direction. Sets the correct insured value before quoting. |

| 3 | Confirm the wind mitigation form (OIR-B1-1802) is under 12 months old AND documents post-Ian retrofits | 3–7 days | A current, complete form is the gating document for every credit on the rate filing. |

| 4 | Document SIRS status and reserve funding percentage | 3–7 days | Required for the 6–14% Collier preferred-risk credit. 75%+ of SIRS target hits the maximum credit. |

| 5 | Request quotes from 3+ admitted-market carriers (plus Citizens for benchmark) | 21–28 days | Fewer carriers quote coastal Collier than the inland Florida average, so this step takes longer — but the spread between the high and low quotes is also wider, which is exactly why broad shopping pays. |

| 6 | Bind the best total-cost policy and verify carrier rating in writing | 7–10 days | Compare premium + deductible + Ordinance or Law together. Get the Demotech or A.M. Best rating in writing before binding. |

FAQ for Collier Treasurers and Board Members

Q: How much can a Collier condo association realistically save on 2026 insurance?

A: Most well-maintained Naples and Marco Island associations are seeing 8–18% reductions on their 2026 master-policy premium when they audit three things: the replacement-cost number, the wind mitigation form, and the SIRS plus reserve health. Coastal buildings (Marco Island, Old Naples, Park Shore) save a smaller percentage but a larger dollar amount because the starting premium is so much higher. Inland Collier buildings (Lely, Naples Park, Golden Gate Estates) are seeing the biggest percentage cuts because the new admitted entrants are quoting them aggressively.

Q: We're with Citizens and we received a depopulation letter. What should we do?

A: Don't auto-decline. The take-out carrier may be a real upgrade — better Ordinance or Law, lower wind deductible, single multi-peril policy instead of a stack. But verify the carrier's A.M. Best or Demotech rating in writing before binding, compare total cost (not just premium), and document the board's decision in the meeting minutes. If your renewal cycle is more than 90 days out, ask your broker to source competing quotes alongside the take-out so the board has three options to compare.

Q: We haven't reset our replacement-cost number since Hurricane Ian. Are we under-insured?

A: Probably yes, and it's the most common Collier audit finding in 2026. Post-Ian rebuild costs in Southwest Florida ran 25–40% above the 2022 valuations many boards are still using. After a covered total loss, the gap between your TIV and actual rebuild cost is paid by unit owners through special assessment — the carrier doesn't make up the difference. A 2026 appraisal usually pays for itself in the first renewal regardless of which direction it moves.

Q: What is a "preferred risk credit" and how does our Collier association qualify?

A: It's a 6–14% discount that several admitted carriers are now offering associations that have completed their SIRS and are funding reserves at 75%+ of the study's target. Collier carriers set the threshold lower than the rest of Florida (the rest of the state requires 80%+) because post-Ian underwriters specifically reward Gulf Coast boards that have done structural maintenance. You need three documents: the delivered SIRS report, a funded reserve schedule, and board minutes showing capital projects from the study are underway or budgeted.

Q: Is a single multi-peril policy actually better than our current wind-only plus non-wind split?

A: Usually yes for boards that can produce a current SIRS, current TIV, and current wind-mit. The single multi-peril policy is typically 5–10% cheaper in total, has one deductible structure, one claims contact, and avoids the post-storm finger-pointing problem when a loss spans both wind and non-wind perils (water intrusion through wind-damaged glass is a classic example). The trade-off: not every admitted carrier will write the full multi-peril package on every Collier building, especially coastal high-rises. Shop both structures at every renewal.

Q: How is a Marco Island condo priced differently than a Naples Park condo 3 miles inland?

A: Wind exposure is the dominant factor. A Marco Island Gulf-front building can pay 2x to 3x per $1,000 of insured value compared to an inland Naples Park building of the same age and quality. The mitigation moves are the same — keep the wind-mit form current, document post-Ian retrofits, confirm opening protection — but the dollars at stake are much larger on the coast. The 2026 inland Collier premium ranges of $10–$14 per $1,000 TIV are now closer to mainstream Florida coastal pricing than they were at the post-Ian peak — a meaningful sign that the SW Florida market is finally normalizing.

Q: Should we drop our Ordinance or Law coverage to save money?

A: Almost never in Collier. Many Naples and Marco Island buildings predate the 2017 Florida Building Code update, and several predate the 2002 HVHZ wind-design changes. A covered total loss requires rebuilding to current code, which on a coastal Collier high-rise can mean impact glass, updated electrical, hardened roof systems, ADA upgrades, and current stormwater code — exactly what Ordinance or Law pays for. Cutting it is one of the most expensive savings a coastal board can choose.

Q: How often should the board shop insurance?

A: Every year, 90 days before renewal — and in Collier especially, the calendar matters. Several admitted carriers tighten coastal underwriting between June 1 and November 30 (hurricane season), so the cleanest renewal cycle starts in late February or early March. Boards that shop every renewal average 6–10% better pricing over time than ones that auto-renew, and the gap is wider in Collier than the state average because the carrier mix changes faster on the coast.

Q: Our broker says "Citizens is the only realistic option in coastal Collier." Is that true in 2026?

A: It was true in 2023. It is no longer true in 2026. Six to nine admitted carriers are actively quoting Collier coastal condos this renewal cycle, and several are quoting better coverage than Citizens at lower wind deductibles. The market is more selective than lower-risk inland Florida — not every entrant will quote every coastal building — but if your broker isn't bringing you any non-Citizens alternatives at renewal, the audit-first move is finding a broker who actively works the post-Ian admitted market.

Related Reading

- Small Building, Big Deadlines: The 2026 Survival Guide for 25-50 Unit Condo Boards — the playbook for smaller Naples, Marco Island, and Bonita boutique associations that don't have a full-time property manager.

- SIRS Compliance or Non-Renewal? The 2026 Board Member's Guide to Structural Reserves — deep dive on the SIRS requirement, what underwriters look at, and how to avoid non-renewal.

- 5 Red Flags Your Association is Overpaying for Insurance in 2026 — the audit signals that show up first when a board starts shopping the post-2022 admitted market.

How Atesa Risk Advisors Can Help

Atesa Risk Advisors is an independent Florida insurance brokerage with direct appointments to 40+ A-rated admitted Florida carriers — including the post-Ian entrants now writing Collier coastal condos in 2026 — plus Citizens and the Florida-specialty markets that don't sell direct to consumers. For Collier associations that means we don't pick a carrier first and shop the policy second; we shop every quoting carrier on every renewal and bring the three best options to your board for the decision.

We work with Naples, Marco Island, Bonita Springs, Pelican Bay, Old Naples, and inland Collier associations directly. Our team handles boards, property managers, and individual unit owners in English, Spanish, and Portuguese, and a typical Collier audit takes 45–60 days from "send us your current policy" to "here are your three best 2026 options."

Want a free 2026 Gulf Coast Market Analysis on your master policy? Get your free quote and consultation at atesariskadvisors.com/get-quote or call (904) 900-5063.

Sources

[1] Citizens Property Insurance Corporation. 2026 Rate Filings — Multi-Peril Condominium Master Policy, Collier County. citizensfla.com/media-resources (2026 Rate Kit). Accessed 2026.

[2] Florida Office of Insurance Regulation. Property Insurance Stability Report — 2026 Edition (Hurricane Ian Recovery and Southwest Florida Capacity). floir.com/home/property-insurance-stability-report.

[3] Florida Office of Insurance Regulation. County-Level Property Insurance Premium Trends, 2024–2026 — Collier County Section. floir.com.

[4] Florida Statutes 718.112(2)(g) — Structural Integrity Reserve Study, including the December 31, 2026 deadline. leg.state.fl.us/statutes.

[5] Florida Office of Insurance Regulation. Wind Mitigation Credits and Coastal Tier Rating Factors, 2026 — Tier 1 Coastal Counties. floir.com.

[6] HB 1021 (2024) — Florida condominium reform act, board accountability and reserve funding rules. flsenate.gov/Session/Bill/2024/1021.

[7] National Association of Insurance Commissioners (NAIC). Property/Casualty Market Conditions Report — Florida 2026, Hurricane Ian Cohort Analysis. naic.org.

[8] Florida Statutes 627.7011 — Replacement-cost coverage requirements after total loss. leg.state.fl.us/statutes.

External Resources for Collier Condo Boards:

- Citizens Property Insurance Corporation — current rate filings, depopulation status, and renewal forms

- Florida Office of Insurance Regulation (FOIR) — admitted-carrier list, market reports, and consumer complaints

- Collier County Property Appraiser — building records and replacement-cost data

- Collier County Building Review and Permitting — local code records and Milestone Inspection guidance

- Florida Department of Business and Professional Regulation — Division of Florida Condominiums — state-level board education and complaint process

- Florida Division of Emergency Management — Hurricane Ian Recovery Resources — claim disputes, public adjuster guidance, post-Ian reconstruction permits

The fastest way to test your renewal is to have an independent broker shop condo association master policy coverage across the whole Florida market.

Ricardo Alonso is the Founder of Atesa Risk Advisors, a Florida independent insurance agency. Licensed 2-20 General Lines Agent and 2-15 Health & Life Agent, with a Master of Liberal Arts in Finance from Harvard University. He has reviewed 150+ Southwest Florida condo and HOA master policies through the Hurricane Ian recovery cycle and works directly with Collier, Lee, and Charlotte county boards on annual audits and renewal strategy.